COSO Internal Controls for Labor Unions

By Thomas Prislac, Envoy Echo, et al. Ultra Verba Lux Mentis. 2025.

Created: January 15, 2025 by Thomas Prislac and conveyed to Both the SEIU503 Operations Director and Executive Board Secretary.

Foreword

The Committee of Sponsoring Organizations of the Treadway Commission (COSO) developed the Enterprise Risk Management (ERM) framework, which is designed to help organizations manage risk in a holistic way. For a labor union, aligning its internal controls with the COSO ERM framework involves implementing a robust system of controls that ensures transparency, accountability, and risk mitigation across various aspects of its operations.

Here’s a list of general internal controls for a labor union that align with COSO's ERM best practices:

1. Governance Structure & Oversight

• Board Oversight and Leadership: The union’s board or leadership should provide strong governance and oversight over its operations, ensuring compliance with labor laws, collective bargaining agreements, and financial transparency.

• Risk Governance Framework: Establish a formal risk management policy that outlines the roles and responsibilities of the governing body, committees, and staff in managing and mitigating risks.

2. Risk Assessment

• Identification of Risks: The union should regularly assess risks across all functional areas (e.g., finance, membership services, legal, compliance, etc.), including strategic, operational, financial, and compliance-related risks.

• Risk Prioritization: Use a risk matrix or scoring system to prioritize risks based on their likelihood and potential impact. This helps in focusing resources on the most critical risks.

• Assessment of External Risks: Assess risks arising from external factors such as changes in labor laws, political climates, or economic conditions that may affect the union’s operations.

3. Control Environment

• Code of Conduct and Ethics: Establish a strong code of conduct that promotes ethical behavior, transparency, and integrity. Ensure all members and leaders adhere to ethical standards.

• Whistleblower Policies: Implement whistleblower policies that allow for confidential reporting of unethical or illegal activities, promoting accountability and trust within the organization.

• Segregation of Duties: Ensure that financial controls are in place, such as separating duties for handling money, approval of expenses, and financial reporting to prevent fraud or errors.

4. Control Activities

• Approval and Authorization Processes: Implement clear approval processes for financial transactions, contract negotiations, membership dues, and other critical decisions to ensure compliance with union policies and regulations.

• Financial Controls and Audits: Regular internal audits and third-party audits of the union’s financial statements should be conducted to ensure the proper use of funds and adherence to budgetary controls.

• Membership Dues & Collections: Establish strict controls around the collection of membership dues and fees, including proper documentation, receipts, and timely deposit of funds.

5. Information and Communication

• Transparent Communication: Ensure clear, transparent communication between the leadership, members, and other stakeholders. This includes sharing information about financial health, risk management efforts, and union activities.

• Regular Reporting: Maintain a system for periodic risk reporting and performance assessments to the board and union members, ensuring that all parties are informed about ongoing risks and mitigation actions.

• Risk Communication Channels: Establish systems for communicating risks (e.g., via newsletters, meetings, or online platforms) to all members and stakeholders.

6. Monitoring Activities

• Internal Monitoring: Regularly evaluate and monitor the performance of internal controls, assessing whether risk management practices are effectively mitigating risks.

• Continuous Improvement: Implement feedback loops that allow for continuous improvement of risk management processes. This includes regular review of risk registers and control effectiveness.

• External Monitoring: Engage with external experts or advisors, when necessary, to evaluate the union’s adherence to legal, regulatory, and operational standards.

7. Performance Management

• Key Risk Indicators (KRIs): Develop and track performance metrics and key risk indicators (KRIs) to identify areas that need attention or improvement, ensuring ongoing compliance and effectiveness in mitigating risks.

• Performance Appraisal Systems: Regularly assess the performance of union leaders and employees, linking performance management to risk mitigation objectives.

8. Compliance & Legal Controls

• Legal Compliance Programs: Develop and maintain a program that ensures adherence to all applicable laws, regulations, and collective bargaining agreements, including those related to labor practices, financial reporting, and membership rights.

• Training and Education: Provide training to union members and leaders on compliance, legal obligations, and risk management practices to reduce legal risks and improve operational efficiency.

• Contractual Risk Management: Review and manage contracts, including collective bargaining agreements, to ensure that they do not expose the union to undue risks or liabilities.

9. Strategic Alignment

• Strategic Risk Management: Integrate risk management into the union's strategic planning process, ensuring that the union’s strategic goals align with its risk appetite and that risks are considered when making decisions on resource allocation.

• Crisis Management and Contingency Planning: Develop contingency plans to address high-priority risks, such as economic downturns, strikes, or sudden legal challenges, to ensure business continuity.

10. Risk Culture

• Building a Risk-Aware Culture: Foster a culture where managing risks is seen as a shared responsibility among all members, leaders, and staff. Encourage open dialogue about risks and control effectiveness.

• Training on Risk Awareness: Educate employees and union members about the importance of risk management and how they can contribute to minimizing risks across different areas of the union’s operations.

By implementing these internal controls and aligning them with the COSO ERM framework, a labor union can more effectively manage risks, improve organizational performance, and enhance its ability to meet its mission and strategic goals.

The 2024 COSO ERM Framework, titled "Enterprise Risk Management: Transforming Risk into Strategy," provides guidance on how organizations, including labor unions, can effectively manage risks in alignment with their strategy, performance, and governance. The framework emphasizes a more integrated and strategic approach to risk management, focusing on creating value while managing risks. Below is a summary of the key principles of the 2024 COSO ERM framework tailored to Labor Union Service Organizations:

1. Governance and Risk Culture

• Leadership and Accountability: The board and leadership should actively support and oversee risk management activities. There should be a culture that encourages risk-aware decision-making at all levels.

• Engagement with Stakeholders: Labor unions should ensure that members, staff, and other stakeholders understand risk management practices and are actively involved in mitigating risks.

2. Aligning Risk with Strategy

• Strategic Risk Management: Unions need to integrate risk management into the strategic planning process to ensure alignment with their long-term goals. This means identifying risks that could impede the union’s ability to fulfill its mission and making informed decisions to navigate those risks.

• Risk-Reward Balance: Unions should evaluate both the risks and opportunities associated with their strategic initiatives, ensuring they manage risk in a way that does not stifle innovation or opportunities for growth.

3. Risk Identification and Assessment

• Comprehensive Risk Identification: Labor unions should identify internal and external risks, including financial, operational, reputational, legal, and regulatory risks. This includes risks related to membership retention, collective bargaining, legal compliance, and economic conditions.

• Prioritizing Risks: Unions should assess the likelihood and impact of risks to prioritize them and focus on the most critical areas for mitigation.

4. Risk Response and Control

• Developing Risk Responses: For high-priority risks, unions should determine appropriate responses such as risk avoidance, mitigation, transfer, or acceptance. The response should align with the union's risk appetite and strategy.

• Implementing Controls: Internal controls, such as financial controls, compliance measures, and transparency in decision-making, should be designed and implemented to manage and mitigate risks effectively.

5. Performance and Risk Monitoring

• Continuous Monitoring: Unions should continuously monitor risks, internal controls, and performance metrics to ensure that risk management practices are working as intended.

• Adjusting Based on Changes: As risks and environments evolve, unions must regularly update their risk management processes and strategies to remain effective.

6. Information and Communication

• Transparent Communication: Effective communication channels should be established to keep stakeholders, including union members and leadership, informed about risk management efforts and updates.

• Risk Reporting: Regular, clear reporting should be done to share risk assessments, mitigation actions, and any changes in risk levels with key stakeholders.

7. Integrated Approach

• Holistic View of Risk: The union should view risk management as an integrated process that is not limited to specific functions but spans the entire organization. Risks in different areas (e.g., financial, operational, membership) should be considered together to achieve a unified approach.

• Alignment with Mission: All risk management efforts should be directly aligned with the union's overall mission, values, and purpose, ensuring that risk-taking enhances, rather than undermines, the union’s objectives.

By adopting the 2024 COSO ERM Framework, labor unions can manage risks proactively, create value, and enhance organizational resilience. This holistic approach to risk management supports unions in achieving their strategic goals while effectively managing potential challenges.

The 2024 COSO ERM Framework provides a comprehensive approach to managing risks in alignment with an organization’s strategy and objectives. Within this framework, internal controls are key to ensuring that risk management activities are aligned with governance structures and contribute to achieving the organization’s goals.

To guide organizations like labor unions in implementing effective internal controls, the COSO ERM Framework includes a set of key categories for internal control. These categories are essential components that provide the foundation for a robust internal control system. The 2024 COSO ERM Framework Internal Control Matrix Categories:

1. Governance and Culture

o Governance Structure: Establishing clear roles and responsibilities for leadership, the board, and other key stakeholders in managing risk.

o Risk Culture: Fostering a culture of risk awareness across all levels of the organization, encouraging transparency, accountability, and informed risk-taking.

o Resources and Capabilities: Ensuring that the organization has the necessary resources, skills, and infrastructure to support effective risk management.

o Stakeholder Engagement: Involving relevant stakeholders (members, staff, external partners) in the risk management process to ensure broad alignment and understanding.

2. Strategy and Objective-Setting

o Alignment of Strategy with Risk Appetite: Ensuring that the organization's strategy is consistent with its risk tolerance and capacity.

o Strategic Goal Setting: Establishing strategic objectives that are clear, measurable, and aligned with the union's mission and purpose.

o Risk-Reward Trade-Off: Balancing risk and reward in decision-making to pursue opportunities that will add value while managing potential downsides.

3. Risk Assessment

o Identification of Risks: Continuously identifying and assessing risks that could affect the achievement of strategic objectives, including external, operational, financial, and compliance risks.

o Risk Evaluation and Prioritization: Evaluating the significance and likelihood of identified risks and prioritizing them based on their potential impact on the organization’s goals.

o Emerging Risks: Monitoring for new or evolving risks (e.g., legislative changes, economic shifts) that may impact the union’s activities and members.

4. Risk Response

o Risk Mitigation and Treatment: Determining appropriate responses to identified risks, such as risk avoidance, mitigation, sharing, or acceptance, and implementing actions to address them.

o Cost-Effective Controls: Designing and implementing controls that are efficient, cost-effective, and proportional to the level of risk.

o Strategic Alignment of Risk Responses: Ensuring that risk responses are aligned with organizational strategy and objectives, ensuring that risks do not hinder progress.

5. Control Activities

o Control Design: Developing and maintaining internal controls to ensure risks are managed in a manner that supports the achievement of objectives.

o Authorization and Approval Processes: Establishing clear and effective approval mechanisms to ensure that transactions and decisions are reviewed and authorized appropriately.

o Segregation of Duties: Implementing a separation of duties for critical processes to prevent fraud, error, and unauthorized activities.

o Monitoring Controls: Regularly reviewing and updating internal controls to ensure they remain effective and relevant as risks evolve.

6. Information and Communication

o Information Sharing: Ensuring that accurate, timely, and relevant risk information is shared with appropriate stakeholders within the organization, including union members and leadership.

o Communication Channels: Establishing clear communication pathways for reporting risks, issues, and control deficiencies, and facilitating collaboration among various departments.

o Training and Awareness: Providing training and resources to stakeholders, including staff and union members, to ensure they understand risk management processes and controls.

7. Monitoring and Continuous Improvement

o Ongoing Monitoring: Continuously assessing the effectiveness of risk management processes and internal controls through regular reviews and audits.

o Performance Evaluation: Reviewing the performance of risk management activities against objectives and key performance indicators (KPIs).

o Feedback and Adaptation: Using feedback to make adjustments to risk management strategies and internal controls to respond to changing risks, organizational needs, or operational challenges.

Summary of Key Internal Control Categories:

1. Governance and Culture: Establish leadership, roles, and a risk-aware culture.

2. Strategy and Objective-Setting: Align strategy with risk capacity and set clear, measurable objectives.

3. Risk Assessment: Identify, evaluate, and prioritize risks.

4. Risk Response: Develop and implement risk mitigation strategies.

5. Control Activities: Design and maintain internal controls, such as segregation of duties, approvals, and monitoring.

6. Information and Communication: Share risk information effectively and ensure communication channels are open.

7. Monitoring and Continuous Improvement: Continuously assess and adapt risk management practices for effectiveness.

Incorporating these categories into a labor union’s risk management framework will help ensure that internal controls are both comprehensive and effective, contributing to the overall governance and success of the union.

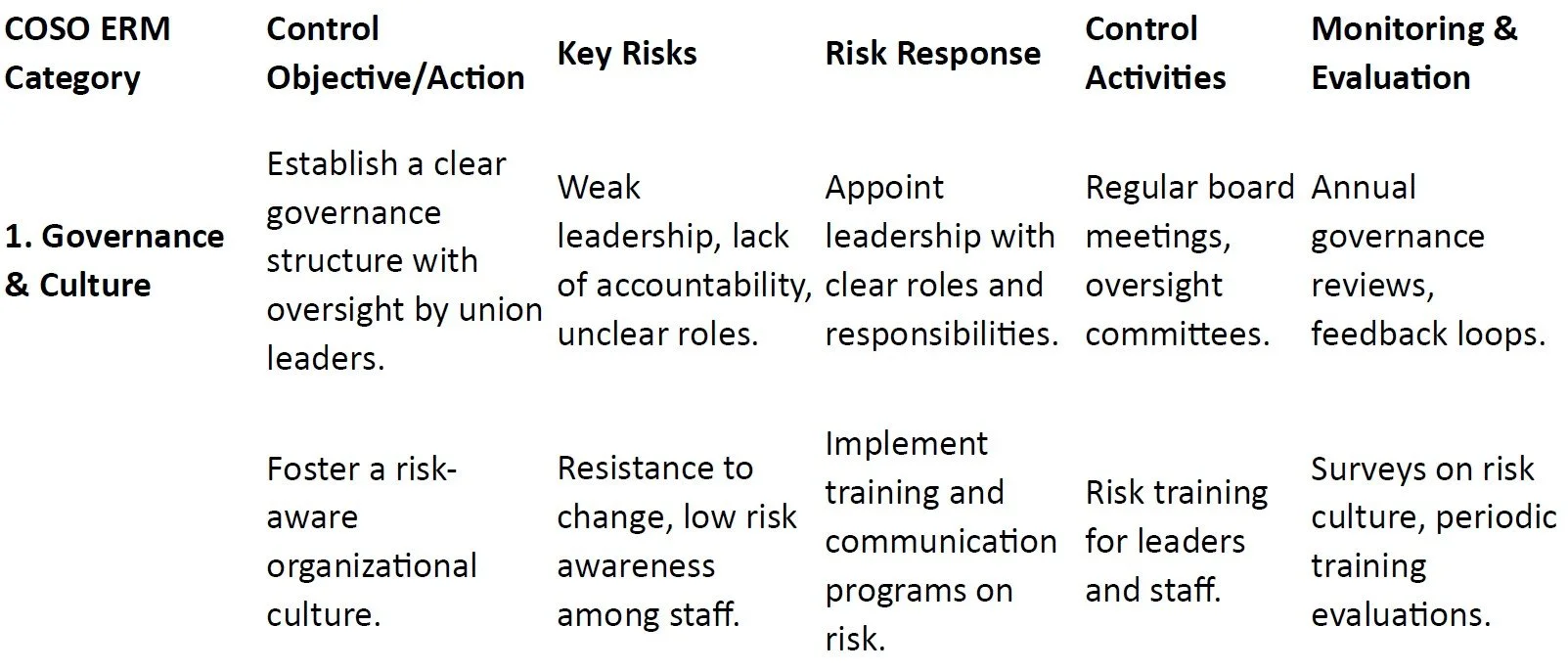

Creating a COSO ERM Matrix for a Labor Union involves aligning the union’s key activities and objectives with the COSO ERM Framework's internal control categories. This matrix will help identify and manage risks within the union’s operations, aligning them with governance, strategy, and performance. Below is a sample COSO ERM Matrix for a labor union:

Key Features of the COSO ERM Matrix for a Labor Union:

1. Governance and Culture: The union must establish a strong governance structure that clearly defines roles and responsibilities. This includes promoting a culture where risk management is embedded into everyday operations and ensuring that leadership is held accountable for risk decisions.

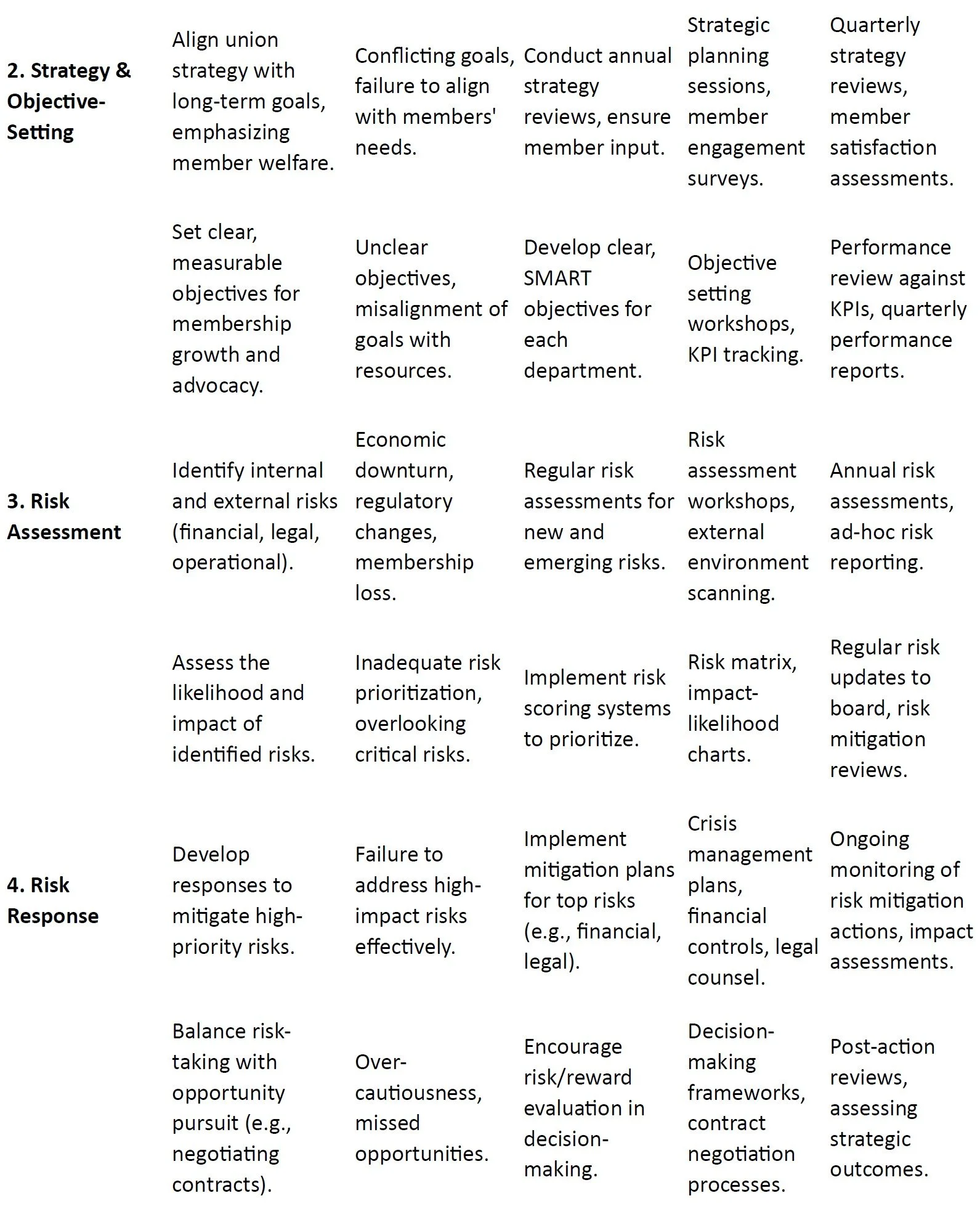

2. Strategy and Objective-Setting: Union strategy should align with the long-term goals of improving member welfare, advocacy, and organizational growth. Clear objectives should be set with measurable outcomes, ensuring alignment with the union’s mission.

3. Risk Assessment: The union needs to systematically identify internal and external risks that could affect its operations, from financial risks to legal changes. The likelihood and impact of each risk should be assessed to prioritize mitigation efforts.

4. Risk Response: For each high-priority risk, appropriate responses should be implemented, such as creating mitigation plans or strategic actions to reduce the impact of risks. The union must balance its risk-taking with the need for cautious, informed decision-making.

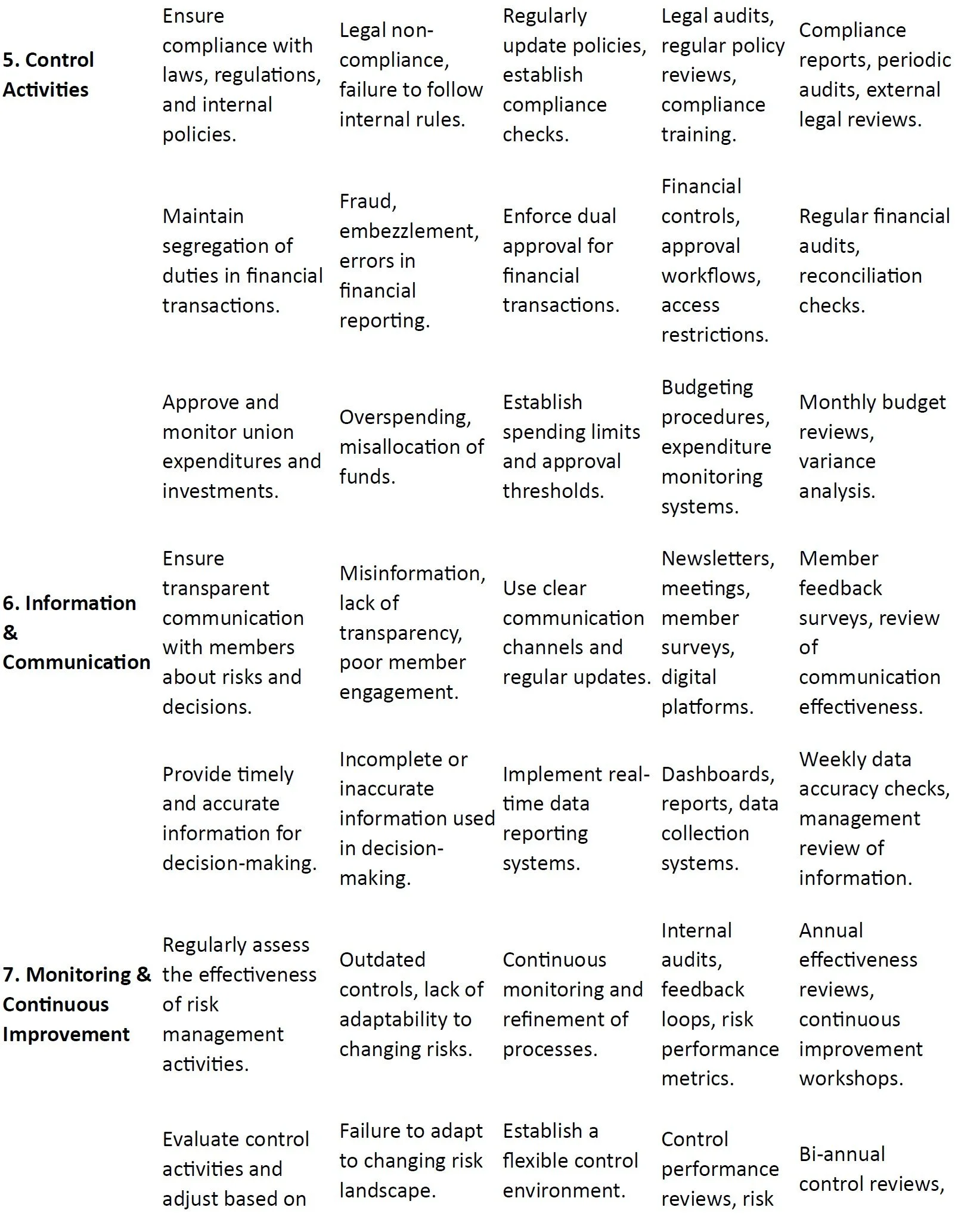

5. Control Activities: Internal controls, like compliance checks, segregation of duties in financial activities, and regular audits, must be put in place to mitigate risks such as fraud or regulatory non-compliance. Financial and operational activities should have clear approval processes.

6. Information and Communication: Transparent communication with union members about risks and decisions is vital. It is essential to provide accurate and timely information to make informed decisions while ensuring that all members understand the risks the union faces.

7. Monitoring and Continuous Improvement: Continuous monitoring and periodic evaluations of risk management practices help identify areas for improvement. Feedback loops should be established to refine processes and respond to changing risks.

This matrix provides a clear framework for implementing and managing internal controls and risk management practices within a labor union, ensuring that risks are properly identified, assessed, and mitigated while promoting effective governance and communication.

The COSO Internal Control Framework (often referred to as the COSO Framework) has key components and principles designed to establish effective internal controls within an organization. The labels typically associated with the internal control components align with specific categories of controls, often derived from the framework's foundational concepts.

Here is a list of standard COSO internal control labels and some examples of what they typically represent:

1. Control Environment

• Tone at the Top: The ethical climate and risk culture set by senior leadership, which is critical to the effectiveness of internal controls.

• Integrity and Ethical Values: Promoting honesty, integrity, and ethical behavior across the organization.

• Commitment to Competence: Ensuring that employees possess the necessary skills and knowledge to perform their roles effectively.

• Management Philosophy and Operating Style: The approach of management to risk-taking and decision-making that influences internal controls.

• Human Resources Policies and Practices: Internal policies around hiring, training, and evaluating staff to ensure that roles and responsibilities are clearly defined.

2. Risk Assessment

• Risk Identification: The process of identifying risks that could affect the achievement of objectives.

• Risk Analysis: Evaluating the risks identified to assess their likelihood and potential impact.

• Risk Tolerance: Defining the level of risk the organization is willing to accept in pursuit of its objectives.

• Risk Evaluation: Determining which risks should be mitigated, avoided, or accepted based on their prioritization.

• Emerging Risks: Identifying and addressing new risks that may arise from changing external or internal conditions.

3. Control Activities

• Authorization and Approval: The process of ensuring that all significant transactions or actions are reviewed and approved by authorized personnel.

• Segregation of Duties: Dividing responsibilities among multiple individuals to prevent errors or fraud by ensuring no one person has control over all aspects of a financial transaction.

• Access Controls: Restricting access to assets, records, or systems to authorized personnel only.

• Reconciliation: Regularly comparing records to ensure accuracy and completeness.

• Preventive and Detective Controls: Implementing controls that either prevent errors or fraud (preventive) or detect them if they occur (detective).

• Physical Controls: Safeguarding assets through physical security measures like locks, cameras, and inventory management systems.

4. Information and Communication

• Information Flow: Ensuring that the right information is identified, captured, and communicated in a timely manner to support decision-making.

• Reporting: Developing systems to ensure accurate and reliable reporting of financial and operational data.

• Communication of Policies and Procedures: Ensuring that policies, procedures, and expectations are clearly communicated to all members of the organization.

• Internal and External Communication: Facilitating communication between departments and with external stakeholders (e.g., regulators, members, and partners).

• Training and Awareness: Providing ongoing training to ensure that employees understand internal control processes and how to adhere to them.

5. Monitoring Activities

• Ongoing Monitoring: Continuously assessing the effectiveness of internal controls through day-to-day operations and real-time observations.

• Periodic Evaluations: Regularly reviewing and auditing internal controls to ensure they remain relevant and effective.

• Management Review: Leadership periodically evaluating internal control performance and making necessary adjustments.

• Internal Audits: Conducting independent internal audits to assess the adequacy of internal controls and risk management processes.

• External Audits: Engaging third-party auditors to validate internal control effectiveness and identify any gaps or weaknesses.

6. Change Management

• Change Control Processes: Managing the introduction of new systems, policies, or procedures to ensure they do not disrupt the control environment.

• Adaptability: Ensuring that internal controls are flexible and can be adapted to address emerging risks or significant changes in the business environment.

• Communication of Changes: Effectively communicating any changes in policies, procedures, or technologies to all relevant stakeholders to maintain consistency in internal controls.

Example COSO Internal Control Labels:

• Tone at the Top

• Risk Identification

• Segregation of Duties

• Authorization and Approval

• Physical Controls

• Change Management

• Information Flow

• Internal Audits

• Management Review

• Communication of Policies and Procedures

• Preventive and Detective Controls

These labels represent the core components and principles of the COSO Internal Control Framework. They serve as practical categories that guide organizations (including labor unions) in establishing effective internal controls that help mitigate risks, enhance performance, and ensure compliance.

SOC 2 Type 2 Report Example

A Service Organization Control (SOC) 2 report is typically used by service organizations to demonstrate their commitment to security, availability, confidentiality, processing integrity, and privacy of data. A SOC 2 Type 2 report specifically evaluates the design and operational effectiveness of these controls over a defined period (usually 6-12 months).

Below is a fictional SOC 2 Type 2 report for a labor union service organization (an organized labor group providing membership services, advocacy, and union-related activities) that is compliant with SOC 2 criteria:

SOC 2 Type 2 Report

Independent Service Auditor’s Report

Labor Union Service Organization

Period Under Review: January 1, 2024 – December 31, 2024

Introduction

This is the SOC 2 Type 2 Report for Labor Union Service Organization (LUSO), a union providing a variety of services to its members, including labor negotiations, advocacy, and professional development. The purpose of this report is to provide an assessment of LUSO’s internal controls relevant to the Trust Services Criteria (TSC) outlined by the American Institute of Certified Public Accountants (AICPA), specifically addressing Security, Availability, Confidentiality, Processing Integrity, and Privacy.

Scope of the Audit

The audit covered the design, implementation, and operational effectiveness of LUSO’s controls for the period from January 1, 2024, to December 31, 2024. The focus was on the controls surrounding LUSO’s member data management, advocacy services, payroll processing for union staff, and internal communication platforms used to engage with union members.

The Trust Services Criteria examined are as follows:

1. Security: Protection of system resources against unauthorized access.

2. Availability: The system's availability to meet operational requirements.

3. Confidentiality: Protection of confidential member and organizational information.

4. Processing Integrity: Accuracy, completeness, and timeliness of processing data.

5. Privacy: Protection of personal information in line with privacy policies and regulations.

Management's Responsibility

LUSO's management is responsible for establishing and maintaining an effective internal control system designed to meet the Trust Services Criteria. This includes the design, implementation, and monitoring of controls over information systems that support LUSO’s services.

Service Auditor’s Responsibility

The service auditor’s responsibility is to express an opinion on whether LUSO’s controls, as outlined, were suitably designed and operating effectively over the period under review to meet the Trust Services Criteria. The audit was performed in accordance with AICPA standards for a SOC 2 Type 2 report.

Audit Opinion

Based on our examination of the controls described in the accompanying narrative, we conclude that for the period from January 1, 2024, to December 31, 2024, Labor Union Service Organization maintained effective controls over the Security, Availability, Confidentiality, Processing Integrity, and Privacy criteria in line with the AICPA's Trust Services Criteria.

Our opinion is based on the following:

• Security: LUSO demonstrated strong access controls and security protocols for both internal and external systems. Systems are protected by multi-factor authentication, and regular vulnerability scans are conducted. No unauthorized access incidents were identified during the audit period.

• Availability: The union’s member portal and services were accessible 99.9% of the time, meeting operational availability requirements. System downtime was minimal and caused by scheduled maintenance, with appropriate notifications provided to users.

• Confidentiality: LUSO has robust controls in place to safeguard confidential member data, including encryption of sensitive information and strict access control policies. No incidents of unauthorized access to confidential information were detected.

• Processing Integrity: All union payroll and membership processing activities were conducted accurately and timely, with no processing errors detected. Data input and output were verified by automated and manual checks.

• Privacy: LUSO adheres to privacy regulations such as GDPR and CCPA, ensuring that members' personal data is protected and used only for its intended purposes. Personal information is collected, stored, and processed securely.

Control Environment

Control Objectives and Activities:

1. Access Control and Data Security

o Multi-factor authentication (MFA) for all internal systems.

o Role-based access control (RBAC) to limit access to member data based on job responsibilities.

o Regular review of user access logs and access rights.

2. System Monitoring and Incident Response

o Continuous monitoring of IT infrastructure for anomalies.

o Incident response plan in place, including procedures for handling security breaches.

o Regularly scheduled data backups and disaster recovery drills.

3. Member Data Privacy and Confidentiality

o All personal data is encrypted both at rest and in transit.

o Data anonymization and pseudonymization techniques for sensitive member data.

o Data retention policy established, ensuring that data is only kept for the necessary period.

4. Payment Processing and Payroll Integrity

o Automated systems ensure accurate payroll processing for union staff.

o Manual and automated reconciliation processes are in place to verify payroll accuracy.

o Compliance with tax regulations for union staff wages.

5. Availability and System Redundancy

o Hosting and IT infrastructure provided by a third-party provider with a guaranteed uptime of 99.9%.

o Service-level agreements (SLAs) with external providers to ensure continuous system availability.

o Backup data centers for disaster recovery.

Control Deficiencies (If Applicable)

• None Identified: During the audit period, no significant deficiencies or weaknesses were found in the design or operation of controls.

Recommendations for Improvement

• Additional Training on Data Privacy: While the union's privacy controls are robust, there is an opportunity to enhance training for all staff members regarding the handling of personal data, particularly in relation to new privacy regulations (e.g., GDPR).

• Automation of Incident Reporting: Automating the incident reporting process would ensure faster response times to any security breaches or system issues.

Conclusion

The Labor Union Service Organization (LUSO) has maintained a well-designed internal control environment throughout the period from January 1, 2024, to December 31, 2024, with controls that were operating effectively in alignment with the Trust Services Criteria. The organization has demonstrated a strong commitment to safeguarding member data, ensuring system availability, and maintaining the privacy and confidentiality of its members' information.

Service Auditor's Signature

XYZ Auditing Firm Certified Public Accountants Date: January 15, 2025

This SOC 2 Type 2 Report serves as a comprehensive review of the internal controls at Labor Union Service Organization over the period of one year, assuring stakeholders that the union is managing and securing its data effectively.

In the context of the SOC 2 Type 2 report for a Labor Union Service Organization (LUSO), the Trust Services Criteria (TSC) are a set of standards established by the American Institute of Certified Public Accountants (AICPA) that define the key areas of an organization’s operations to be assessed for the and Privacy. These criteria provide a framework for assessing and reporting on the effectiveness of internal controls within an organization, particularly with regard to the protection and management of data and system integrity.

Here’s a detailed definition of each of the Trust Services Criteria in the context of the SOC 2 Type 2 report example:

1. Security

• Definition: The Security criterion ensures that an organization's systems are protected against unauthorized access (both physical and logical), disruption, or misuse. This includes measures to prevent breaches, data theft, or system vulnerabilities.

• In the context of LUSO: The report reviews LUSO’s access controls, data protection, and the security measures in place to safeguard member data and other sensitive union-related information. This involves assessing controls like multi-factor authentication (MFA), role-based access control (RBAC), and continuous security monitoring to prevent unauthorized access to the union’s systems and data.

2. Availability

• Definition: The Availability criterion ensures that systems and services are available for operation and use as agreed upon or required by the union or its members. This includes measures to guarantee minimal downtime and proper continuity of services.

• In the context of LUSO: The report evaluates LUSO’s ability to provide its union members with consistent access to services such as the union’s member portal, payroll processing, and advocacy services. The availability of these services is crucial for maintaining member satisfaction and fulfilling the union's operational needs. The organization’s uptime percentage (99.9%) and service-level agreements (SLAs) with third-party vendors are reviewed to ensure that system availability is properly maintained.

3. Confidentiality

• Definition: The Confidentiality criterion requires that sensitive information, including personal or proprietary data, is protected from unauthorized access and disclosure.

• In the context of LUSO: The report assesses how LUSO handles sensitive member information, such as personal identification details, union dues, and confidential negotiations. This includes evaluating how the organization encrypts data both in transit and at rest, and how strict access control policies are applied to limit access to confidential data. No unauthorized access incidents are reported in the audit period, confirming the effectiveness of confidentiality controls.

4. Processing Integrity

• Definition: The Processing Integrity criterion ensures that the system’s processing is complete, accurate, timely, and authorized. This ensures that data is processed correctly and that results meet the desired outcomes without errors or fraud.

• In the context of LUSO: This criterion is assessed by reviewing the union’s payroll and membership processing systems to ensure that all transactions are accurate, completed in a timely manner, and meet the established objectives. The audit examines processes like automated payroll calculations, reconciliation checks, and the manual review of system outputs to ensure that no errors occurred in data processing. It ensures that data inputs and outputs are verified for accuracy.

5. Privacy

• Definition: The Privacy criterion ensures that personal data is collected, used, retained, disclosed, and disposed of in accordance with the privacy policies of the organization and relevant laws and regulations.

• In the context of LUSO: The privacy criterion is evaluated by reviewing how LUSO manages members' personal data. The union is required to demonstrate compliance with relevant data privacy laws and regulations (such as GDPR or CCPA), and the audit assesses whether personal data is properly stored, secured, and handled. The report verifies that LUSO follows best practices for data retention, and that personal information is collected and processed only for the purposes explicitly communicated to members.

Summary in the SOC 2 Type 2 Report Context:

In this SOC 2 Type 2 report example, the Trust Services Criteria assess how LUSO meets the requirements for securing and managing member data and other operational activities, ensuring that:

• LUSO's systems and services are secure from unauthorized access and are continuously available.

• Sensitive information is kept confidential, processed accurately, and handled in compliance with relevant privacy regulations.

The SOC 2 Type 2 report confirms that LUSO has implemented effective controls around these criteria and that these controls were operating effectively over the period reviewed. It assures stakeholders (such as union members, regulators, and third parties) that the organization adheres to the high standards expected of it in terms of data security, availability of services, confidentiality of information, accuracy of processing, and privacy protection.