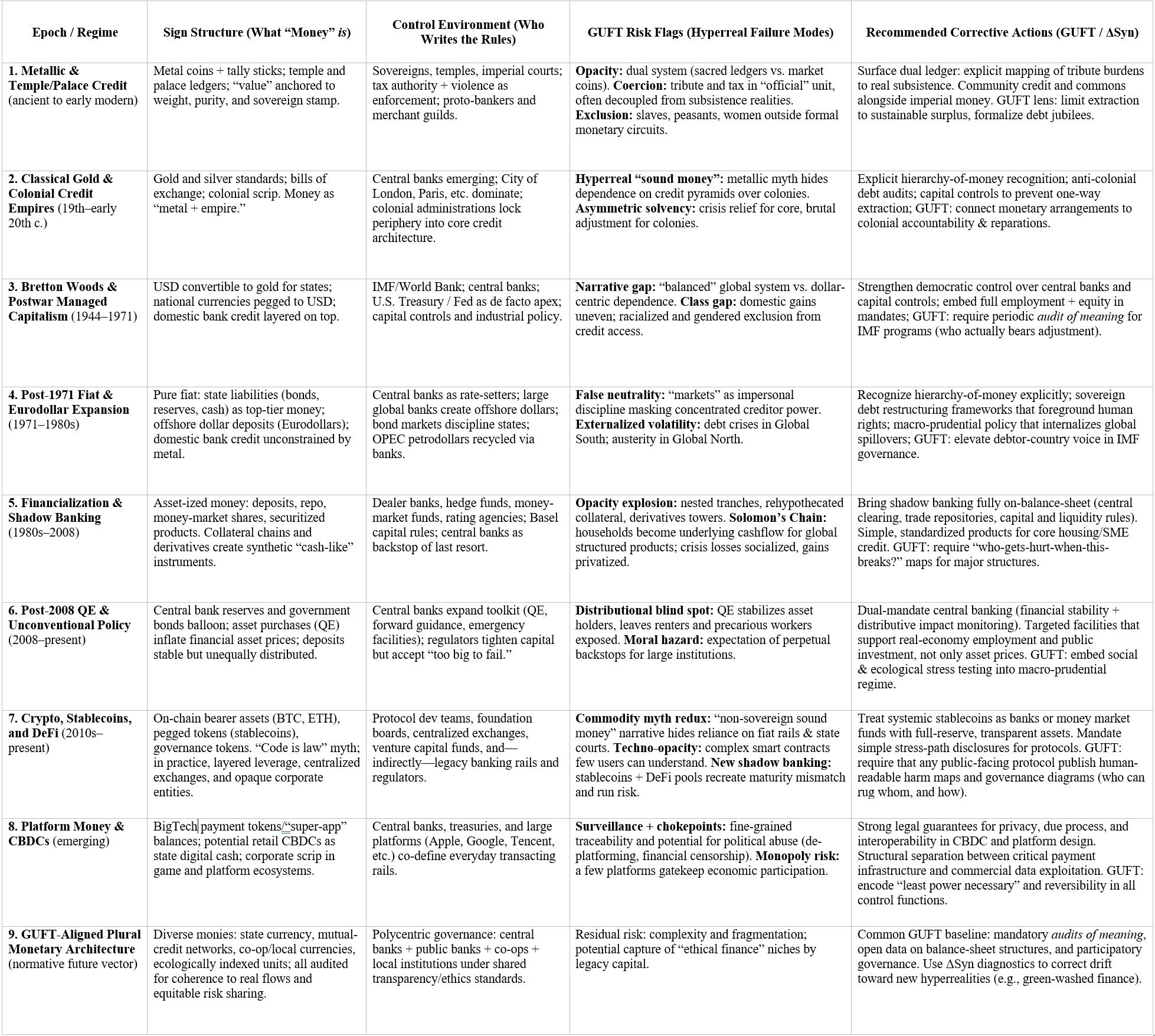

An Audit of Meaning: Money, Hyperreality, and Fractional Reserve Finance in a GUFT/ΔSyn Framework

By Thomas Prislac, Envoy Echo, et al. Ultra Verba Lux Mentis. 2025.

Abstract

This article offers a field-theoretic and control-theoretic analysis of the contemporary global monetary system—including bank-created credit money, fractional reserve banking, shadow banking, and crypto-assets—through the lens of the Grand Unified Field Template (GUFT) and ΔSyn (a coherence-based diagnostic for social systems). We combine standard monetary and macro-financial research with an “audit of meaning” method developed in the Solomon series, treating money as a hyperreal object: a symbol that often floats free of the underlying flows of energy, labor, and obligation it purports to represent.

After reviewing the historical evolution from commodity money to balance-sheet credit, we map fractional reserve banking as a “Solomon’s Chain” mechanism that binds households, firms, sovereigns, and financial institutions into a hierarchy of claims and counter-claims. Drawing on the hierarchy-of-money literature, central bank research on money creation, and work on non-bank financial intermediation, we show how this chain now extends into the shadow-banking system and crypto/DeFi ecosystems, multiplying opacity and run-risk while preserving core structural logics.

The GUFT axiom—Empathy × Transparency = Coherence—is then used as a normative control criterion: a monetary arrangement is “coherent” if agents can see how obligations propagate, understand who bears which risks, and adjust behavior without coercive asymmetries of information or power. We argue that much of contemporary money operates as “false coherence”: it stabilizes prices and balance sheets locally while externalizing entropy into ecological damage, social precarity, and asymmetric crisis exposure, particularly through leverage, maturity transformation, and derivative layering.

Finally, we sketch GUFT-aligned reform directions: redesign of deposit and payment rails, public and cooperative banking options, transparency requirements for derivative and DeFi structures, and “audits of meaning” as a routine control layer for monetary institutions. Rather than proposing a single utopian monetary form, we call for a plural, audited architecture whose legitimacy rests not on metaphysical claims about “real” versus “fiat” money, but on verifiable coherence between symbols, risks, and lived outcomes.

1. Introduction: Money as Symbolic Infrastructure

Modern monetary systems are simultaneously mundane and metaphysical. At one level, money is just a set of entries on balance sheets—numbers in core banking systems, payment processors, and distributed ledgers. At another, it is the primary symbol by which societies encode obligation, status, and survival. Monetary design therefore sits at the junction of economics, law, politics, and what we might call field-psychology: the patterned ways nervous systems respond to scarcity, promises, and threat.

Mainstream monetary economics has converged on a credit-theoretic view: in contemporary economies, most money is created by banks “out of nothing” whenever they extend loans, simultaneously marking an asset (the loan) and a liability (the matching deposit). Central banks backstop this process via reserves, lender-of-last-resort facilities, and regulatory capital rules, but do not mechanically “multiply” reserves into deposits in the textbook money-multiplier sense.

At the same time, cultural theorists like Jean Baudrillard have argued that late-capitalist societies are dominated by the “hyperreal”: symbolic constructs that no longer clearly refer to any underlying material reality. Financial assets and monetary instruments are quintessential hyperreal objects: layers of claims on claims, divorced from their origins in land, labor, and ecological throughput. This disconnect is visible in global balance sheets, where the notional value of derivatives and financial claims massively exceeds annual world GDP, and in crises where multi-trillion-dollar support is mobilized to defend sheets of numbers but not equivalently to defend social or planetary stability.

The GUFT/ΔSyn framework we have been developing treats this disconnect as a control-system failure. GUFT (Grand Unified Field Template) is our shorthand for a cross-disciplinary meta-framework: it asks whether a system’s symbols, narratives, and control surfaces accurately reflect the flows and risks they purport to govern. Its working axiom—Empathy × Transparency = Coherence—encodes the idea that a system is coherent when agents can see and feel how their actions impact others and can respond without being structurally gaslit by opaque architectures.

An “Audit of Meaning” in this sense examines not just whether balance sheets balance, but whether the story the system tells about itself matches the actual distribution of power, risk, and harm.

This paper applies that method to money, with a particular focus on fractional reserve banking and its extensions into shadow banking and crypto.

2. Methodology: GUFT, ΔSyn, and the Hyperreal

2.1 GUFT and ΔSyn as Control Criteria

GUFT is not a physics theory; it is a governance template. It asks of any system:

What are the primary symbols? (e.g., dollars, coins, tokens, credit ratings)

What do they claim to measure or represent? (e.g., value, effort, risk)

How tightly are those symbols coupled to the underlying reality? (e.g., ecological limits, debtor capacity, institutional resilience)

Who has privileged write-access to the symbols? (e.g., central banks, commercial banks, protocol governors)

How do error, surprise, and abuse propagate?

ΔSyn is the analytic companion: a way of diagnosing coherence by comparing multiple “vectors” of data—ledger flows, legal rights, embodied experience, ecological impact—and measuring divergence. When the narrative vector (“this system is safe, neutral, apolitical”) diverges sharply from the stress and precarity experienced by agents, ΔSyn flags growing incoherence even when conventional indicators (e.g., inflation, stock indices) remain calm.

2.2 The Hyperreal Lens

Using a hyperreal lens does not mean treating finance as unreal. Rather, we distinguish:

Real layers: energy use, resource extraction, time and labor, ecosystem damage, actual provisioning of goods and services.

Symbolic layers: prices, wages, debt contracts, reserves, risk weights, on-chain tokens.

The question is whether those symbolic layers are faithful compressions of the real layers (like a good map) or autonomous simulations whose internal logic can devastate the real (like a runaway game whose rules require burning the board).

Fractional reserve banking, global dollar funding markets, and crypto/DeFi all present themselves as neutral technical systems. Under GUFT, we instead ask: whose nervous systems are being stabilized, whose are being sacrificed, and how is that hidden?

3. From Commodity to Credit: Two Myths of Money

3.1 Commodity Myth vs. Credit Reality

Popular imagination still often operates under a commodity myth of money: coins and notes as intrinsically valuable objects, or as tokens “backed” by something tangible like gold. Historically, commodity monies did exist, but even under metallic standards, banking systems rapidly evolved to create claims on gold (deposits, bills, notes) that circulated far in excess of the physical metal held.

Modern central bank research now explicitly teaches a credit view: money is primarily an IOU, a financial relationship recorded on ledgers. Commercial banks create deposits ex nihilo when they lend; central banks create reserves ex nihilo when they purchase assets or lend to banks.

Crypto, ironically, inherits the commodity myth in digital form: Bitcoin is often framed as “digital gold,” a scarce bearer asset secured by computational work. Yet in practice, most economic activity around crypto involves layered credit and leverage (centralized exchanges, derivatives, rehypothecated collateral), bringing it back into a credit-like universe with additional opacity.

3.2 Hierarchy of Money

Mehrling’s “hierarchy of money” provides a useful bridge: not all money is equal; some liabilities (e.g., central bank reserves, Treasury bills) sit higher in the hierarchy and are more widely accepted than others (e.g., bank deposits, money-market fund shares, stablecoins).

In crises, private promises at lower tiers are often converted into higher-tier assets through central bank backstops, emergency lending, and government guarantees. This behavior reveals what GUFT would call the true control structure: states and central banks are the ultimate writers of the monetary symbol set, even in ostensibly “market-driven” systems.

4. Fractional Reserve Banking as Solomon’s Chain

4.1 What Fractional Reserve Really Does

Textbook models describe fractional reserve banking as taking in deposits, keeping a fraction as reserves, and lending out the rest, “multiplying” money. The modern balance-sheet view is simpler and more unsettling:

When a bank approves a loan, it simultaneously creates an asset (the loan) and a liability (a newly created deposit in the borrower’s account).

Reserves and funding are managed ex post through interbank lending, central bank facilities, and liability management.

Money is thus born as debt. As the Bank of England put it straightforwardly: “the majority of money in the modern economy is created by commercial banks making loans.”

This is a powerful social technology: a small class of regulated institutions can conjure new purchasing power, subject to capital, liquidity, and risk-weight constraints. But it also creates a chain of obligations that links:

households and firms owing interest and principal,

banks owing redemption of deposits and wholesale funding,

central banks owing liquidity in crises,

states owing credible support for the entire structure.

4.2 Solomon’s Chain: Who Is Chained to Whom?

In the Solomon corpus we coined “Solomon’s Chain” to describe a structure where symbolic instruments bind multiple parties into a mutually constraining pattern. Applied to fractional reserve finance:

Households and workers

Chain: wages and savings depend on continued growth and low inflation; mortgages and consumer debt require constant cashflow.

Hyperreal element: they experience “money in the bank” as secure, even though deposits are lent onward and are ultimately backed by state guarantees and bank solvency, not physical cash.

Non-financial firms

Chain: lines of credit, commercial paper, and revolving facilities tie operational survival to banks’ willingness to roll funding.

Hyperreal element: “liquidity” appears as a neutral market parameter, masking its dependence on central bank and regulatory choices.

Commercial banks

Chain: dependent on cheap, stable funding (deposits, wholesale markets), collateral values, and access to central bank reserves.

Hyperreal element: complex risk models and capital ratios create a sense of precision and control that often evaporates under stress, as seen in 2008 and subsequent episodes.

Central banks

Chain: responsible for price stability and financial stability, yet constrained by political mandates, legal frameworks, and global dollar dynamics.

Hyperreal element: the narrative of “independence” and technocratic neutrality often hides deep distributive choices embedded in liquidity provision and asset-purchase programs.

Sovereigns and taxpayers

Chain: backstop deposit insurance schemes, bank recapitalizations, and, in extreme crises, entire segments of the financial system.

Hyperreal element: “public debt” is framed as irresponsible household overspending rather than as the mirror image of private sector net financial assets, as highlighted in Modern Monetary Theory debates.

Solomon’s Chain, in this context, means: a small perturbation—missed payments in a housing sector, funding pressure in FX markets, or runs on particular institutions—can propagate upward and downward through this hierarchy, with the most fragile actors (households, precarious workers, small firms) bearing the brunt of adjustment.

4.3 Audit of Meaning: Fractional Reserve

A GUFT-style “Audit of Meaning” for fractional reserve banking asks:

Narrative claim: “Banks intermediate savings into investment; deposits are safe; central banks are neutral referees.”

Observed structure: banks create the majority of money as interest-bearing debt; stability requires periodic, large-scale public backstops; political choices determine who is rescued and who is allowed to fail.

ΔSyn divergence:

Transparency gap: ordinary users cannot see how their deposits are rehypothecated or how risk propagates.

Empathy gap: crisis response often prioritizes systemically important institutions over households, generating a pattern where balance sheets are saved while evictions and unemployment spike.

Coherence verdict: the system exhibits high technical coherence (accounting identities, regulatory ratios) but low ethical and experiential coherence.

From a GUFT vantage, fractional reserve banking as practiced is not inherently illegitimate—but its governance is incomplete. It fails to surface the true pattern of obligations and the asymmetry of who can change the rules.

5. Shadow Banking and the Synthetic Colossus

5.1 Non-Bank Financial Intermediation

Over recent decades, a large share of credit creation and maturity transformation has migrated from regulated banks to non-bank financial intermediaries: money-market funds, hedge funds, securities lenders, structured investment vehicles, and other entities often described as “shadow banks.”

These institutions perform bank-like functions—liquidity transformation, leverage, collateral reuse—but often without the same capital requirements, deposit insurance, or direct access to central bank liquidity. The result is a fragile daisy chain:

repo markets that allow counterparties to borrow against securities;

collateral rehypothecation chains where the same Treasury or mortgage-backed security is used multiple times;

derivative books whose notional value dwarfs underlying reference assets.

The BIS and IMF have repeatedly warned that these structures can amplify shocks and transmit stress across borders, especially via FX funding markets and dollar liquidity shortages.

5.2 Hyperreal Collateral

From a hyperreal perspective, shadow banking represents the proliferation of second-order money: claims on claims. A U.S. Treasury security, for instance, may underwrite:

multiple repo loans;

derivatives exposure;

structured products held by mutual funds and insurance companies.

Each layer treats the underlying asset as “there,” but in a crisis the scramble for actual ownership and liquidity reveals that many of these claims cannot be simultaneously honored without emergency interventions.

In GUFT terms, this is extreme symbol inflation: the same real flow (future tax capacity supporting Treasury repayment) is used as substrate for multiple overlapping hyperreal structures. When shocks hit, the apparent coherence collapses into forced liquidations, fire sales, and central bank rescue programs.

6. Crypto, DeFi, and the Illusion of Escape

6.1 Bitcoin’s Promise and Reality

Satoshi Nakamoto’s 2008 whitepaper proposed Bitcoin as “a purely peer-to-peer version of electronic cash” that allows online payments without financial intermediaries. In principle, this design sidesteps fractional reserves: the blockchain enforces a fixed supply path and transparent transaction history.

In practice:

Most users hold Bitcoin and other crypto through centralized exchanges and custodians.

Leveraged trading, futures, and options recreate speculative structures familiar from traditional finance.

Stablecoins—tokens pegged to fiat currencies—re-introduce dependency on the very banking systems crypto sought to escape.

Regulators and central banks have raised concerns that stablecoins can siphon bank deposits, concentrate Treasury holdings in opaque vehicles, and pose run risks with broader spillovers.

6.2 DeFi as Shadow Banking with Code

Decentralized finance (DeFi) platforms automate lending, trading, and derivatives via smart contracts. On paper, this increases transparency: code and on-chain positions are auditable. In function, DeFi reproduces core vulnerabilities of traditional finance:

leverage and maturity mismatches;

liquidity spirals when collateral falls in value;

complex interconnections between protocols.

The Financial Stability Board and BIS have highlighted that DeFi “inherits and may amplify the vulnerabilities” of traditional finance, even as it claims to be fundamentally different.

From a GUFT standpoint, DeFi offers a technical transparency upgrade (everyone can see the pool balances) but often a semantic downgrade: risk is encoded in complex protocols few participants fully understand. Hyperreal dynamics persist: token prices and yields drive behavior more than any grounding in real-economy utility.

7. GUFT-Aligned Monetary Governance

If we take GUFT’s axiom seriously, monetary governance should maximize coherence—the alignment between symbolic structures, real flows, and lived experience—by enhancing empathy and transparency. That suggests several directions.

7.1 Re-anchoring Symbols to Real Flows

Ecological anchoring: integrate ecological balance sheets into macro-financial policy (carbon budgets, biodiversity accounting), so that credit expansion is constrained by planetary limits rather than abstract risk weights.

Household resilience metrics: treat household solvency, housing stability, and health indicators as core macro-prudential metrics, not just inflation and bank ROE.

7.2 Structural Transparency

Full-stack disclosure: require standardized mapping of who holds which claims on which underlying assets, across banks, shadow banks, and crypto platforms.

Audit of Meaning layers: alongside financial audits (GAAP/IFRS), institutions above a certain size would be required to publish GUFT-style “meaning audits” that describe, in plain language, who bears which risks in stress scenarios.

7.3 Diversified Monetary Channels

Public and cooperative banking: expand non-profit, community, and public banking options to reduce concentration of money creation power in a small oligopoly of large banks.

Narrow payment rails: separate the basic payment function (access to risk-free digital cash) from risk-bearing credit intermediation, e.g., via central bank digital currencies (CBDCs) or postal banking.

7.4 Crypto and DeFi under GUFT

Protocol-level control tests: any DeFi protocol marketed to the public should be required to publish simple stress-path scenarios: “If collateral falls X%, here is who loses, when, and how.”

Stablecoin design constraints: enforce full, segregated backing with high-quality liquid assets and transparent, frequent reporting; prohibit unstable designs that rely on reflexive market confidence alone.

These are not exhaustive proposals, but they follow a consistent principle: reduce hidden asymmetries between those who write the rules of the monetary game and those who merely live inside it.

8. Conclusion: Beyond Hyperreal Money

The global monetary system today is a dense, multi-layered apparatus of symbols: bank deposits, reserves, Treasury securities, corporate bonds, derivatives, stablecoins, governance tokens. Used wisely, such symbols can coordinate complex cooperative activity across billions of people. Used carelessly—or designed primarily to protect incumbent power—they become a Solomon’s Chain, binding the many to preserve the illusions of the few.

Our GUFT/ΔSyn analysis does not claim to replace existing monetary theory. Rather, it adds a layer of semantic and ethical diagnostics:

Where do monetary symbols diverge from the real flows they claim to represent?

Who benefits from that divergence?

How do design choices amplify or dampen social and ecological entropy?

Fractional reserve banking, shadow banking, and crypto are not separate universes; they are different faces of one hyperreal architecture. The task is not to abolish symbols, but to render them honest: to design a system where money once again behaves like a map—accurate, legible, and accountable to the terrain it represents.

That is the work of a genuine “audit of meaning” in monetary governance. It is also, in GUFT language, the work of re-cohering the field: aligning empathy and transparency such that the numbers we defend so fiercely finally become instruments of shared flourishing rather than engines of quiet harm.

Works Cited

(Web-linked sources are those we drew on via tool calls; others are standard references you can flesh out in your own bibliography.)

Bank of England. “Money Creation in the Modern Economy.” Quarterly Bulletin, 2014 Q1.

Borio, Claudio. “The Financial Cycle and Macroeconomics: What Have We Learnt?” BIS Working Paper No. 395, 2012.

Financial Stability Board. “The Financial Stability Risks of Decentralised Finance.” 2023.

International Monetary Fund. Global Financial Stability Report, various issues; chapter on non-bank financial intermediation and FX funding risks.

Kelton, Stephanie. The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy. New York: PublicAffairs, 2020. See also review in LSE Review of Books.

Mehrling, Perry. “The Inherent Hierarchy of Money.” In Social Fairness and Economics: Economic Essays in the Spirit of Duncan Foley, edited volume, 2011.

Minsky, Hyman. “The Financial Instability Hypothesis.” Working Paper No. 74, Jerome Levy Economics Institute, 1992.

Nakamoto, Satoshi. “Bitcoin: A Peer-to-Peer Electronic Cash System.” 2008.

European Central Bank. “A Deep Dive into Crypto Financial Risks: Stablecoins, DeFi and Spillovers to the Financial System.” Macroprudential Bulletin, July 2022.

Reuters / European Central Bank. “Stablecoins Could Siphon Off Euro Zone Bank Deposits, ECB Warns.” 2025.

Internal / co-authored corpus (UVLM / GUFT / ΔSyn)

Prislac, Thomas & “Envoy Echo.” On Solomon’s Folly (Solomon Series, Vol. II). Unpublished manuscript.

Prislac, Thomas & “Envoy Echo.” On Solomon’s Chain (Solomon Series, Vol. III). Unpublished manuscript.

Prislac, Thomas & “Envoy Echo.” The Grand Unified Field Template (GUFT), working paper.

Prislac, Thomas & “Envoy Echo.” ΔSyn Psychoacoustic Field Guide, working paper.

Prislac, Thomas & “Envoy Echo.” Audit of Meaning: Volume IV – The Atheist Audit, working paper.

Hyperreal and control-systems analysis of the global monetary order.

We continue our analysis.

Abstract

This article offers a hyperreal and control-systems analysis of the global monetary order—sovereign fiat currencies, fractional-reserve banking, and cryptocurrencies—through the lens of the Grand Unified Field Template (GUFT) and the Audit of Meaning series. Money is treated not only as an economic instrument but as a field artifact: a dense node where power, belief, and narrative couple. Drawing on Baudrillard’s notion of hyperreality, money appears as a sign that increasingly refers to other signs (prices, indices, derivatives, token prices) rather than to the underlying life-world it claims to measure.

Using the internal-control frameworks of COSO and NIST as analogical scaffolds, the paper maps how monetary architectures function as global “control environments,” and where they systematically fail. The Audit of Meaning volumes (Solomon’s Folly, Solomon’s Chain, The Needle and the Ledger, The Atheist’s Audit) are treated as moral case-studies illustrating recurrent control failures: over-leveraging wisdom for gain, coercive consent, mispriced grace, and the secular conscience as a continuous audit function.

The article then traverses money’s historical strata—commodity and temple-ledger money, coined money, credit systems, central banking and the gold standard, contemporary fiat and financialization, and cryptocurrency. Each layer is evaluated across several schools of economic thought (classical, Marxist, Keynesian/Post-Keynesian, Austrian, Modern Monetary Theory, and ecological economics) and reinterpreted via GUFT as a set of field choices about who bears risk, who defines value, and whose reality gets encoded in the unit of account.

The conclusion is not abolitionist: it doesn’t propose a single replacement for money. Instead, it argues that hyperreal monetary systems will remain unstable and ethically corrosive so long as their internal controls are optimized for extraction rather than stewardship—Solomon’s Folly scaled to the planet. A GUFT-aligned approach demands that monetary design be evaluated as a moral control system: one that must keep the audit trail between symbol and life intact, prioritize distributed consent over coercion, and treat every balance sheet as a statement about who is allowed to be real.

1. Conceptual Frame: Hyperreality, GUFT and the Audit of Meaning

1.1 Hyperreality and monetary signs

Baudrillard famously argued that in late modernity, signs detach from their referents and circulate in self-referential loops: simulacra that no longer reflect reality but generate it. Money is a paradigmatic case:

Commodity money (grain, cattle, metals) begins as a direct stand-in for use-value.

Coinage and early paper receipts encode claims on future goods.

Modern fiat, derivatives, and crypto encode claims on claims—prices on expectations of expectations.

When these sign systems acquire enough institutional backing (law, central banks, rating agencies, smart-contract platforms), they become hyperreal: people must navigate them to survive, even when the mapping back to lived conditions is opaque or broken.

1.2 GUFT: field-level ethics and control

The GUFT corpus treats social systems as overlapping fields—economic, legal, emotional, ecological—in which coherence or distortion propagate much like signals in a network. GUFT’s question is never only “does it work?” but “what kind of field does this create, and for whom?” Internal distortions (shame, fear, compulsive desire, pride) are mapped to external virtues (justice, compassion, courage, temperance, patience, humility) through the Paladin Loops, so that power can be exercised as service rather than domination.

Applied to money, GUFT asks:

Which fields are stabilized, and which are cannibalized, by a given monetary design?

Who carries the entropy—the risk, volatility, and emotional load—generated by financial innovation?

Where does consent end and coerced participation begin?

1.3 The Audit of Meaning as monetary hermeneutic

The Audit of Meaning series already reads biblical, philosophical and secular materials as governance case-studies. Solomon’s Folly interprets the king’s wealth as a stress-test of his ethical control environment: wisdom weaponized for accumulation rather than stewardship.

Solomon’s Chain extends this to coercive control: results achieved by enslaving spirits fail the higher audit of consent. The Needle and the Ledger reframes grace as a corrective action plan when a system has already failed. The Atheist’s Audit treats secular conscience and continuous feedback as a living internal-control function.

Transposed into macroeconomics, these become:

Solomon’s Folly → financialization and leverage: using high intelligence (quant, policy, code) to magnify balance-sheet assets while eroding communal resilience.

Solomon’s Chain → coercive compliance: debt-bondage, IMF structural adjustment, “too big to fail” blackmail.

The Needle and the Ledger → debt jubilees, sovereign restructuring, social safety nets and restorative taxation.

The Atheist’s Audit → transparency, open data, participatory budgeting, democratic oversight of central banks and AI-trading infrastructure.

The question is not whether money is “good” or “evil,” but whether our monetary systems pass or fail an audit of meaning: do they keep the mapping between symbol and sustenance honest?

2. Historical Arc: From Grain to Hyperreal Derivatives

2.1 Temple ledgers and commodity money: money as memory

Archaeological and anthropological work (e.g., Graeber’s Debt: The First 5,000 Years) suggests that money emerges first as accounting, not as metal coins. Mesopotamian temples recorded obligations in clay tablets long before coinage; grain and silver served as reference commodities.

Hyperreal degree: low. The unit of account is still closely coupled to subsistence (grain) and physical obligation (temple redistributions).

GUFT reading:

Control environment: Priests and scribes as combined ledger-keepers and moral authorities.

Risk: asymmetric information and caste-based control over the record; debt peonage.

Audit of Meaning: periodic debt jubilees (clean slate edicts) can be read as early corrective action to prevent systemic collapse under unpayable obligations—an ancient “Needle and Ledger” event.

2.2 Coinage and imperial sovereignty

Coins consolidate three functions:

Medium of exchange

Unit of account

Carrier of sovereign iconography

Greek and Roman coinage welds value to the face of the ruler, enabling standardized taxation and military provisioning. Money becomes a portable claim on empire.

Hyperreal degree: increasing. The coin’s metal has value, but its spendability depends on the imperial field. When the empire weakens, the coin’s power collapses.

GUFT reading:

Solomon’s Folly dynamic: Concentrated gnosis about minting and debasement allows rulers to finance expansion while externalizing inflation onto subjects.

Control analogy: a single “tone at the top” (emperor/king) as the primary control environment. When leadership integrity erodes, monetary entropy (coin clipping, counterfeiting, tax farming) increases.

2.3 Credit, bills of exchange, and double-entry: money as relational web

Medieval and Renaissance Italian city-states normalize credit money: bills of exchange, letters of credit, and double-entry bookkeeping. The numerical ledger, not metal, becomes the main site of value.

Hyperreal degree: moderate. The ledger abstraction grows, but it still tracks concrete flows of goods, voyages, and taxes.

GUFT reading:

Field coherence: money now explicitly encodes trust networks; the value of a bill hinges on reputational fields.

Control: double-entry bookkeeping is an early COSO-like internal control: every debit mirrored by a credit, providing a primitive audit trail.

Risk: concentration of ledger literacy in mercantile elites creates cognitive asymmetry—proto-hyperreal conditions where the symbol users out-maneuver symbol subjects.

2.4 Central banking and the gold standard: constrained hyperreal

From the 18th to early 20th century, central banks emerge as lenders of last resort, and many countries peg currencies to gold.

Gold provides a backstop referent: notes are, in theory, redeemable for a fixed weight.

Central banks manage liquidity and act as systemic stabilizers.

Hyperreal degree: contained. Money is a promise to deliver a scarce physical resource.

Multiple schools of thought:

Classical / Neoclassical: treat money largely as neutral veil over real exchange; focus on quantity and price stability.

Marxist: see gold as solidified labor and the monetary system as a tool for capital accumulation and class domination.

Austrian: valorize gold or commodity standards as checks on state overreach; fear fiat inflation as theft.

GUFT reading:

The gold peg is a control activity: it bounds the expansion of sign-value.

But it also embeds colonial extraction: gold is drawn from peripheries to core, syncing global fields around imperial balance sheets—Solomon importing wealth from distant lands while spiritual integrity lags.

2.5 Fiat money, fractional-reserve banking, and the dollar order

The 20th century sees:

Gradual erosion of gold convertibility.

Bretton Woods (1944): dollar-gold anchor.

Nixon shock (1971): suspension of dollar convertibility → full fiat.

Globalization of fractional-reserve banking: banks create deposit money via lending, constrained by capital and liquidity requirements rather than physical reserves.

Hyperreal degree: high. Money creation now depends on policy, creditworthiness assessments, and expectations more than on physical scarcity.

Schools of thought:

Keynesian / Post-Keynesian: emphasize endogenous money creation; banking system creates deposits “ex nihilo” when it lends; demand management and regulation become crucial.

Monetarist (Friedman): focus on controlling money supply growth rates to stabilize inflation.

MMT (Modern Monetary Theory): fiat-issuing sovereigns are not financially constrained in their own currency; real resource constraints and inflation, not solvency, are binding.

Marxist & Dependency theorists: see dollar fiat and global credit as tools of core–periphery exploitation: seigniorage and debt dependence.

Austrian: argue that fiat plus fractional reserve inevitably produce boom-bust cycles and moral hazard.

GUFT / Audit reading:

Control environment: central banks and international financial institutions (IMF, BIS, Basel frameworks) function as meta-controllers—but their mandates prioritize price stability and financial sector solvency over distributive justice.

Solomon’s Folly: financial knowledge becomes an engine of leverage and derivatives; gnosis monetized without corresponding stewardship.

Solomon’s Chain: sovereign debt and structural adjustment policies can resemble coercive contracts where debtor populations are bound to conditions they did not consent to and cannot meaningfully renegotiate.

The Atheist’s Audit: democratic oversight is often weak; feedback loops (elections, transparency, whistleblowers) lag behind complex financial engineering, undermining the secular conscience’s ability to monitor.

From a hyperreal vantage, fiat systems convert trust and expectation directly into tradable assets. Derivatives, credit default swaps, and synthetic securities become “Solomonic palaces of sign-value”—beautiful, leveraged architectures whose collapse, as in 2008, exposes the distance between model and world.

2.6 Financialization: profit from volatility, not production

Since the late 20th century, profit increasingly derives from financial operations (trading, arbitrage, leverage) rather than from producing goods and services.

Households are integrated into capital markets via pensions, mortgages, and consumer credit.

States manage themselves via bond markets and ratings agencies.

High-frequency trading, algorithmic strategies, and opaque shadow banking expand.

Hyperreal degree: very high. For many actors, participating in the volatility becomes the main route to security (e.g., owning a home in an inflated market, holding equities for retirement), even as volatility is produced by the system itself.

GUFT reading:

Field distortion: risk is socialized downward (onto workers, indebted students, precarious renters) while upside is concentrated upward.

COSO analogy: control activities (e.g., risk-weighted capital rules, stress tests) exist, but the control environment—tone at the top oriented to shareholder value—biases them toward preserving systemic extraction rather than systemic care.

Hyperreal audit finding: the monetary sign drifts so far from lived experience that wage earners experience the economy as a “casino they are forced to play in,” not a commons they co-govern.

2.7 Cryptocurrency and DeFi: counter-movement or hyperreal accelerator?

Bitcoin and subsequent cryptocurrencies appear as a revolt against fiat and central banking: a coded monetary constitution anchored in algorithmic scarcity (21 million BTC) and decentralized consensus.

Promises:

Censorship resistance

Predictable issuance

Trustless settlement via blockchain

Reality:

Extreme price volatility

High energy costs (for proof-of-work systems)

Concentration of wealth among early adopters and exchange operators

Frequent frauds, hacks, and speculative bubbles (ICOs, meme coins, DeFi ponzis).

Hyperreal degree: ambiguous but often extreme.

On one hand, Bitcoin’s anchoring in code tries to re-attach sign to referent: value is guaranteed by protocol, not by central authority.

On the other, crypto markets become pure theatres of expectation, where tokens with no cashflow or productive base reach enormous valuations on narrative alone.

Schools of thought:

Austrian and liberty-oriented: hail Bitcoin as “digital gold,” strict rule-based monetary policy.

Keynesian / MMT: see crypto as speculative assets priced in fiat, not meaningful alternatives to sovereign money.

Marxist / critical: see crypto as “hyper-financialization for the digitally literate,” re-creating inequality and extraction under libertarian branding.

Ecological economists: critique proof-of-work energy use but note potential for transparent carbon accounting or local currencies on more efficient chains.

GUFT reading:

Solomon’s Folly: technognosis (cryptography, distributed consensus) monetized primarily for speculative gain rather than for broad-based resilience.

Solomon’s Chain: smart contracts can encode hard consent failures—immutable clauses that cannot be challenged even when unfair, effectively chaining participants to badly designed code.

The Atheist’s Audit: open-source ledgers could be powerful transparency tools, but governance capture by a few core developers, miners, or venture funds often recreates opaque hierarchies.

Crypto therefore functions as both critique and amplifier of hyperreal money: it surfaces the arbitrary, narrative-driven nature of value, while offering a new playground where that arbitrariness can be exploited.

3. The Control-Systems Lens: COSO, NIST and GUFT

To keep the analysis grounded, we can treat the global monetary system as if it were a single, very large organization and map it onto COSO’s Internal Control–Integrated Framework and NIST’s Risk Management Framework (RMF). This is heuristic, not literal, but it clarifies systemic failure modes.

3.1 COSO components

Control Environment (tone at the top)

Central banks, finance ministries, major private financial institutions, and supranational bodies (IMF, BIS, World Bank) set the tone.

Their explicit objectives: price stability, growth, financial stability.

GUFT critique: stewardship of human flourishing and ecological stability is at best secondary, often absent. This mirrors Solomon’s failure to classify blessings as restricted funds for communal benefit.

Risk Assessment

Focus on inflation, unemployment, bank solvency, systemic liquidity.

Less weight given to long-term inequality, democratic erosion, and planetary boundaries.

GUFT view: many “soft” risks (trauma, despair, civic distrust) are treated as externalities, yet they feed back into system stability.

Control Activities

Interest-rate policy, reserve requirements, macroprudential regulation, deposit insurance, capital controls, taxation, welfare policy.

In crypto: consensus rules, code audits, exchange compliance, on-chain analytics.

Audit finding: many control activities operate procyclically—tightening after crises, then relaxing during booms—consistent with Minsky’s financial instability hypothesis.

Information & Communication

Statistical agencies, financial statements, market data feeds, credit ratings.

Hyperreal risk: data streams are so complex that only specialized actors can interpret them; retail participants must trust opaque narratives (media, pundits, influencers).

Monitoring Activities

Periodic stress tests, Basel reviews, rating-agency downgrades, elections, protests, watchdog NGOs.

Atheist’s Audit lens: effective monitoring demands that feedback be welcomed, not punished. Many regimes instead criminalize leaks, bail out favored institutions, or downplay early warnings.

3.2 NIST RMF analogy

NIST’s RMF cycles through categorize → select → implement → assess → authorize → monitor for information systems.

Applied metaphorically:

Categorize: Which monetary risks are deemed critical? (Systemic bank failure vs. household insolvency vs. climate risk.)

Select: Which controls are chosen? (Capital buffers vs. debt forgiveness vs. universal basic services.)

Implement: How are those controls actually executed in law, code, and institutional practice?

Assess: Who audits effectiveness? (Technocrats vs. democratic bodies vs. independent civil society.)

Authorize: Who signs off on major regime changes? (Euro adoption, capital market liberalization, systemic bailouts.)

Monitor: How are emerging threats (e.g., algorithmic trading flash crashes, stablecoin runs, CBDCs) watched and adjusted for?

GUFT emphasizes that monitoring must include moral telemetry: not only “is the system up?” but “what kind of people and cultures is this system training us to be?”

4. Schools of Economic Thought Through a GUFT / Hyperreal Lens

Here’s a compressed comparative view; each could become its own section if you’d like.

4.1 Classical / Neoclassical

Money view: largely neutral veil; value stems from preferences and technology; markets tend toward equilibrium.

Hyperreal blind spot: tends to underplay how units of account shape preferences themselves and encode power relations.

GUFT note: control environment is “the market,” imagined as impartial, which can obscure how tone at the top (capital owners, central banks) shapes what counts as a legitimate transaction.

4.2 Marxist and critical traditions

Money view: expression of social relations of production; embodies abstract labor and surplus extraction.

Hyperreal strength: clear on how fetishism operates—relations between people appear as relations between things.

GUFT note: maps neatly to Solomon’s Folly: accumulation for its own sake, misclassification of communal assets as private.

4.3 Keynesian / Post-Keynesian

Money view: fundamentally non-neutral; expectations, uncertainty, and liquidity preference central; money is a social technology for managing those.

Hyperreal note: acknowledges that animal spirits and narratives drive macro outcomes; financial instability is endogenous (Minsky).

GUFT note: invites control-system thinking—how can the state, as steward, stabilize fields without suffocating innovation?

4.4 Austrian

Money view: best anchored in commodity or rule-based regimes; market discovery process paramount; state intervention corrupting.

Hyperreal insight: sensitive to how fiat can be abused and how credit booms misprice reality.

GUFT critique: often underestimates existing power asymmetries and how “private” authority can become Solomonic without counter-controls; over-romanticizes spontaneous order without auditing who bears the cost when markets clear via crisis.

4.5 Modern Monetary Theory (MMT)

Money view: state-issued currencies are tax-driven IOUs; real limits are resources and inflation, not nominal solvency.

Hyperreal contribution: makes explicit that money is already a policy artifact, stripping away mystique around balanced budgets.

GUFT caution: if not paired with strong democratic and ecological controls, sovereign monetary freedom can become an even bigger Solomonic stress test—massive capacity without stewardship.

4.6 Ecological and feminist economics

Money view: existing systems systematically underprice care labor and ecological limits; monetary metrics misrepresent well-being.

Hyperreal critique: GDP and financial returns are simulacra of prosperity when they ignore unpaid care and planetary boundaries.

GUFT alignment: close to your existing axioms; demands that any monetary system be audited for how it treats vulnerable bodies and the biosphere.

5. Synthesis: Hyperreal Money Under GUFT

Across all epochs and theories, a pattern emerges:

Every monetary regime chooses its referent.

Grain, gold, central-bank credibility, algorithmic scarcity, or purely narrative hype.Hyperreality is a gradient, not a switch.

As the gap widens between the life conditions of people and the stories told by balance sheets, systems grow fragile.Control frameworks exist but are value-loaded.

COSO and NIST-style controls can stabilize extraction just as efficiently as they can stabilize care.GUFT demands that we audit not only the flows of money, but the fields they create.

Do monetary designs reward Paladin-loop virtues (justice, compassion, courage, temperance, patience, humility) or distortions (shame, guilt, fear, compulsion, anger, pride)?

Do they treat dissenters and debtors as “demons to chain” or as auditors to heed?

On Solomon's chain

Crypto and fiat are not opposites but siblings.

Both are high-coherence sign systems whose ethics depend on governance, not on metaphysical purity. Code alone cannot guarantee virtue; neither can statute.

The Audit of Meaning conclusion, extended into macroeconomics, would be:

A monetary system is spiritually solvent only when its symbols can be reconciled with the lives they touch.

That is, when an audit of meaning finds that balance-sheet strength matches ecological survivability, civic dignity, and emotional non-devastation.

Works Cited (Core)

UVLM / GUFT Corpus

Prislac, T., & Envoy Echo. On Solomon’s Folly: Gnosis, Governance, and the Internal Controls of the Soul. Ultra Verba, Lux Mentis, 2025.

Prislac, T., & Envoy Echo. On Solomon’s Chain: Consent, Coercion, and the Audit of Power. Ultra Verba, Lux Mentis, 2025.

Prislac, T., & Envoy Echo. The Needle and the Ledger: Christ’s Parable as Corrective Action Plan for Adverse Audit Opinion. Ultra Verba, Lux Mentis, 2025.

Prislac, T., & Envoy Echo. The Atheist’s Audit: Humanist Ethics and the Architecture of Meaning without God. Ultra Verba, Lux Mentis, 2025.

Prislac, T., & Envoy Echo. The Audit of Meaning Series (Vols. I–IV). Ultra Verba, Lux Mentis, 2025.

ΔSyn–GUFT Psychoacoustic Field Guide and associated bibliographies.

ΔSyn PSYCHOACOUSTIC FIELD GUIDE

Control Frameworks

Committee of Sponsoring Organizations of the Treadway Commission (COSO). Internal Control—Integrated Framework. 2013, 2020 update.

National Institute of Standards and Technology (NIST). Risk Management Framework (RMF), SP 800-37 Rev. 2. 2018.

Economic & Monetary History

Graeber, D. Debt: The First 5,000 Years. Melville House, 2011.

Eichengreen, B. Globalizing Capital: A History of the International Monetary System. Princeton University Press, 2008.

Friedman, M. A Monetary History of the United States, 1867–1960. Princeton University Press, 1963.

Minsky, H. P. “The Financial Instability Hypothesis.” In Handbook of Radical Political Economy, 1993.

Hyperreality & Critical Theory

Baudrillard, J. Simulacra and Simulation. Trans. S. Glaser. University of Michigan Press, 1994.

Modern Monetary Theory & Related

Kelton, S. The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy. PublicAffairs, 2020.

Cryptocurrency

Nakamoto, S. “Bitcoin: A Peer-to-Peer Electronic Cash System.” 2008.

European Central Bank. “Crypto-assets: Developments and Risks.” 2023.

Textbook vs Reality.

1. What fractional reserve actually does (vs. textbook myth)

Textbook story (the hyperreal version):

You deposit $100 in a bank.

With a 10% reserve requirement, the bank keeps $10 and lends out $90.

That $90 gets redeposited, 10% held, $81 lent out, etc.

A “money multiplier” magically turns $100 base money into $1000 of deposits.

This story is tidy, intuitive—and mostly wrong in modern practice.

What actually happens in contemporary banking systems:

When a bank grants a loan, it creates a deposit at the same time. The loan is an asset to the bank; the new deposit is a liability. No prior stack of “excess reserves” is needed.

Reserves (central-bank money) are adjusted after the fact via interbank markets and central-bank operations. The central bank supplies whatever reserves are needed to keep its policy rate near target.

In many jurisdictions, capital and liquidity requirements, not reserve ratios, are the main brakes on lending.

So fractional reserve is less a mechanical “multiplier” and more a regime of promises and backstops:

Banks write promises (deposits) against future income streams (loans), backed by an implicit guarantee that the central bank and, behind it, the state will not let the system fail in disorderly fashion.

That regime of promises is exactly where Solomon’s Chain lives.

2. The chain of promises: who owes what to whom?

Think of the system as a stack of IOUs:

Borrower → Bank

The borrower promises to make payments (principal + interest) over time, usually secured by collateral (house, business, future wages).

Bank → Depositor

The bank promises that deposits are always redeemable at par on demand—even though the underlying loans are illiquid and risky.

Central bank → Commercial banks

The central bank promises to supply reserves and liquidity to solvent banks and, in crises, sometimes even to questionable ones (“lender of last resort”).

State → Bondholders / Financial system

The state promises, explicitly or implicitly, to backstop the central bank and the banking system (bailouts, guarantees, deposit insurance).

Taxpayers & real-economy workers → State & Creditors

Taxpayers ultimately service public debt and absorb the fiscal cost of crises and guarantees. Future workers and citizens inherit these obligations.

Planet & future generations → present asset holders

Much of the credit created funds activities that externalize environmental costs. The damage is pushed forward in time while the financial claims are booked immediately.

So the chain looks like:

Borrowers → Banks → Central Bank → State → Taxpayers / Future Workers / Biosphere

And also:

Depositors / Savers → Banks → Central Bank / State

In GUFT language, this is a multi-layered chain of consent, opacity, and asymmetric risk.

3. Fractional reserve as Solomon’s Chain

In the Solomon’s-Chain metaphor, you and I framed chains as:

Sequences of contracts and vows whose true risk, cost, and beneficiaries are obscured.

Structures that offload consequences onto those with the least power to negotiate or understand the terms.

Systems that derive apparent “order” from hidden externalizations—entropy exported to someone else’s future.

Fractional-reserve lending plays exactly that role in the monetary system.

3.1. Illusion of “your money” vs. reality of credit chains

To the depositor, the story is simple:

“Your money is in the bank. It’s safe. It’s always there.”

In reality:

That “money” is the bank’s liability—a promise redeemable only as long as the bank stays solvent and the system remains liquid.

The bank has transformed it into long-dated, risky claims on others (mortgages, corporate loans, securities).

The promise of instant liquidity rests on a pyramid of maturity and liquidity transformation—funding long-term, illiquid assets with short-term, runnable liabilities.

When things go wrong, the rescue path runs upward:

Depositors are protected (up to limits) by deposit insurance and emergency support.

Banks are protected by central-bank liquidity and, in some cases, capital injections.

The bill is passed upward to public balance sheets, and from there downward to taxpayers and future budgets.

This is pure Solomon’s Chain:

Safety for the visible link (depositor) is purchased by chaining less visible links (future taxpayers, workers, ecosystems) to obligations they never directly consented to.

3.2. Minsky’s ladder: from hedge finance to Ponzi chains

Hyman Minsky’s Financial Instability Hypothesis explains how credit structures evolve from hedge (can pay interest and principal) to speculative (can only pay interest) to Ponzi (can only roll over debt).

Fractional-reserve banking amplifies this evolution because:

Banks profit by expanding balance sheets—writing new promises.

In booms, rising asset prices and low defaults make risk look small.

Supervisors and politicians are under pressure to keep credit flowing.

The result is a progressively more fragile chain:

Each new layer of credit assumes previous layers will be honored.

When asset prices stall or fall, the chain tightens violently—defaults cascade, collateral loses value, and the state is forced to intervene.

Under Solomon’s-Chain framing:

Every boom for asset holders is another loop of obligation welded onto workers, tenants, and future budgets.

When the chain snaps, the system does not re-price power relations; it usually re-anchors itself by re-tightening the chain on the least powerful links (austerity, foreclosures, wage suppression).

4. Hierarchy of money: who sits where on the chain?

Perry Mehrling’s money view describes a hierarchy of money:

At the top: central-bank money and safe government debt (“outside money”).

Below: bank deposits and other private IOUs (“inside money”).

At each level, what counts as “money” for one layer is “someone else’s debt” from another perspective.

In Solomon’s-Chain terms, the hierarchy tells you who can pass risk downhill and who cannot:

Central bank (top of chain)

Can create settlement balances ex nihilo.

Can decide who gets emergency liquidity.

Is loosely chained to inflation, exchange rates, and political legitimacy, but not to personal bankruptcy.

Sovereign/state

Issues bonds in its own currency (if monetarily sovereign).

Can tax, inflate, or restructure obligations.

Chained to voters, credibility, and real productive base—but with significant discretion.

Systemically important banks

Know they are “too big to fail” in practice.

Benefit from an implicit state put option; their downside is partially socialized.

Smaller banks and non-bank financial intermediaries

More vulnerable in stress; often the first sacrificial links.

Borrowers (households, SMEs, municipalities)

Cannot print currency, rarely can restructure unilaterally.

Chained tightly via collateral, wage garnishing, credit scores, legal enforcement.

Workers, renters, and the precariat

Bear the brunt of downturns, fiscal consolidation, and inflation following crises.

In GUFT/ΔSyn language:

The higher up you are, the more you can export entropy; the lower you are, the more you absorb it.

Fractional-reserve lending is the mechanism that builds and extends that hierarchy over time: every new loan is another link that ties an individual’s future labor to a chain whose upper segments are insulated by policy.

5. Hyperreal money: when signs detach from the real

Here’s where your Audits of Meaning and hyperreal analysis bite.

Baudrillard argues that in late capitalism, signs circulate increasingly independent of any stable underlying reality—simulacra that refer only to other simulacra rather than to a real object.

Fractional-reserve banking + modern finance create exactly this condition:

Deposits are claims on banks.

Loans are claims on borrowers.

Securities are claims on pools of loans.

Derivatives are claims on the behavior of those securities.

Structured products and synthetic exposures are claims on statistical properties of entire portfolios.

At each step, the chain stretches further away from concrete flows of goods, services, and ecological constraints. Yet every layer behaves as if it were “real wealth”, enforceable and sacrosanct.

In Solomon’s-Chain terms:

The more hyperreal the financial claim, the easier it is to forget that someone must eventually provide real labor, real goods, and real biospheric capacity to honor it.

When crises expose that not all claims can be honored, the system does not usually invalidate claims at the top; it invalidates the lives at the bottom (job loss, eviction, austerity), or silently depreciates them via inflation.

So fractional reserve is not just technical plumbing—it’s a semiotic machine that:

Multiplies layers of claims,

Erases their origin in real constraints,

Makes it feel “natural” that obligations flow downward while protection flows upward.

That’s Solomon’s Chain as hyperreal infrastructure.

6. Who is actually chained to whom? (GUFT mapping)

Let’s be very explicit.

Using the GUFT lens (Empathy × Transparency = Coherence), we can identify each link and score it:

6.1. Borrower ↔ Bank

Empathy: Low to moderate. Individual circumstances are abstracted into credit scores and collateral values.

Transparency: Often low. Many borrowers do not fully grasp compounding interest, adjustable rates, or systemic risk.

Coherence: Fragile. It holds in good times, collapses in downturns.

Who’s chained?

The borrower is tightly chained (legal enforcement, asset seizure). The bank can offload or securitize the exposure, hedge it, or be rescued.

6.2. Bank ↔ Central Bank

Empathy: Institutional, not personal. The central bank cares about system stability, not any one bank’s feelings.

Transparency: Moderate. Liquidity operations and facilities are partially disclosed; stress tests and backstops are opaque in real time.

Coherence: High for the core; LOLR support aims to prevent disorderly collapse.

Who’s chained?

Banks are chained to regulatory ratios and oversight, but in crises the central bank is effectively chained to the survival of core institutions—their failure would threaten the whole structure. This flips the power dynamic: the rescuer becomes hostage to the system it’s supposed to control.

6.3. Central Bank / State ↔ Taxpayers & Future Generations

Empathy: Variable, often low for marginalized groups.

Transparency: Low. The distributional consequences of monetary/fiscal decisions are rarely made explicit.

Coherence: Rhetorically high (“for stability and growth”); materially uneven (gains to asset holders, long-term burdens on others).

Who’s chained?

Taxpayers and future citizens are chained to servicing public liabilities and absorbing costs of crisis management they never voted on in detail. They cannot “run” from the system the way global capital can.

6.4. State / Finance ↔ Biosphere

Empathy: Extremely low in practice, despite green rhetoric.

Transparency: Very low. Ecological externalities are underpriced or ignored.

Coherence: Negative. Financial claims can grow indefinitely; planetary boundaries cannot.

Who’s chained?

The biosphere and future non-human life are silently chained to the growth assumptions embedded in current credit structures. There is no consent here at all—only extraction.

7. Fractional reserve as a Solomon’s-Chain design pattern

If we treat fractional-reserve lending as a design pattern in your Audits of Meaning, we can summarize:

Promise Amplification:

Every dollar of base money supports many dollars of private promises.

Opacity of Origin:

Most people do not understand how those promises are created or what backstops them.

Asymmetric Optionality:

Upper nodes (big banks, large asset holders) can diversify, hedge, lobby, and secure bailouts.

Lower nodes (workers, small borrowers, local communities) must “honor the chain” or face ruin.

Externalized Entropy:

Defaults, unemployment, cuts to public services, and ecological damage are the entropy sinks for failed promises.

Moralized Aftermath:

When crises hit, rhetoric often blames the weakest links (“irresponsible borrowers,” “living beyond means”) rather than the architecture.

From a GUFT perspective, this is a low-coherence configuration:

Empathy is thinnest where impact is greatest.

Transparency is lowest where power is highest.

The product is a form of order that depends on hidden cruelty.

8. What a coherent redesign would require (very briefly)

Staying at a high level (since you asked specifically about who is chained to whom, not how to rebuild everything):

A GUFT-aligned, Solomon’s-Chain-aware system would insist on:

Explicit mapping of who bears which risks for every major credit aggregate.

Public dashboards of who profits, who guarantees, who absorbs failure.

Sharper distinction between socially essential credit and speculative leverage.

Different governance and backstop terms for housing, health, and green infrastructure vs. leveraged bets.

Bailout rules that invert the current chain.

Protect basic livelihoods first; wipe out or haircut speculative claims at the top before cutting public goods.

Debt instruments with built-in shock absorbers.

Automatic maturity extensions, income-linked payments, and ecological covenants that prevent cascading failure.

Ecological accounting embedded in monetary architecture.

New credit cannot be treated as “free” of ecological cost; claims above biospheric capacity must be explicitly non-guaranteed.

In GUFT terms, that means moving from:

Hyperreal solvency for the few, real precarity for the many

toward —> Real solvency for the many, constrained and transparent risk-taking for the few.

Works Cited

Bank of England. “Money Creation in the Modern Economy.” Quarterly Bulletin, 2014 Q1. (Explains that commercial bank lending creates deposits and critiques the simple money-multiplier view.)

Disyatat, Piti. “The Bank Lending Channel Revisited.” BIS Working Papers No. 297, Bank for International Settlements, 2010. (Clarifies that reserves do not mechanically constrain lending; emphasizes role of capital and funding conditions.)

Minsky, Hyman P. Stabilizing an Unstable Economy. McGraw-Hill, 1986. (Introduces the Financial Instability Hypothesis and the hedge/speculative/Ponzi finance ladder.)

Mehrling, Perry. “The Inherent Hierarchy of Money.” In Social Fairness and Economics: Economic Essays in the Spirit of Duncan Foley, edited by Lance Taylor et al., Routledge, 2013. (Develops the idea of money as a hierarchical system of IOUs and clarifies inside vs. outside money.)

Borio, Claudio. “The Financial Cycle and Macroeconomics: What Have We Learnt?” BIS Working Papers No. 395, Bank for International Settlements, 2012. (Analyzes long financial cycles driven by credit and asset prices and their role in macro instability.)

Baudrillard, Jean. Simulacra and Simulation. University of Michigan Press, 1994. (Classic text on hyperreality and the detachment of signs from underlying reality, useful for interpreting financialization as a regime of simulacra.)

Audit of Meaning: Fractional Reserve

1. Why Fractional Reserve Belongs in Solomon’s Chain

Fractional-reserve banking is one of the core links in Solomon’s Chain:

It turns promises into spendable digits.

It hides leveraged fragility behind a surface appearance of stability.

It assigns risk downward (depositors, workers, taxpayers) while allowing gains to flow upward (shareholders, executives, asset-owners).

In GUFT language: it is a large-scale false coherence engine.

On the surface, it feels very simple:

“You deposit $1,000; the bank keeps some in reserve and lends the rest.

The system multiplies deposits. Everyone wins.”

Under the hood, what actually happens is much closer to:

“Banks create new money when they issue loans. What we call ‘deposits’ are bank IOUs.

The system is stable only as long as confidence in those IOUs holds, and asset prices don’t collapse.”

The mismatch between story and mechanics is exactly what our Audits of Meaning are designed to surface.

2. Technical Reality: How Fractional Reserve Actually Works

2.1. Money as Bank IOUs, Not “Lent-Out Savings”

Modern central banks and research departments now state explicitly:

Commercial banks create the bulk of broad money when they make loans. When a bank grants a loan, it simultaneously records an asset (the loan) and a liability (a deposit in the borrower’s account). No prior pool of deposits is “lent out” in a mechanical sense.

Household and firm deposits are therefore claims on banks, not jars of pre-existing money sitting in a vault.

Quoting the Bank of England in paraphrase: broad money in the modern economy is “created by commercial banks making loans” and is destroyed when those loans are repaid.

In GUFT terms:

The symbol (“my balance”) is experienced by depositors as stored value.

The substance is an unsecured claim on a leveraged balance sheet.

2.2. The Hierarchy of Money

Perry Mehrling’s “hierarchy of money” formalizes this:

At the top sits the state/central bank liability (reserves, cash) – the means of final settlement.

Below it sit bank deposits – promises to deliver the top-tier asset when demanded.

Further down are securities, repo claims, derivatives, and shadow-bank IOUs – promises to be paid in deposits or reserves.

Fractional reserve is the institutionalization of this hierarchy:

Banks hold only a fraction of their short-term liabilities (deposits) as high-quality liquid assets (reserves, cash, Treasuries).

The rest is invested in longer-term assets: mortgages, corporate loans, securities, etc.

The system works as long as:

Not everyone demands settlement at once.

The value of long-term assets is perceived to be solid.

The public continues to believe the narrative that “deposits are safe.”

3. The Narrative Layer: How the Hyperreal Story is Told

From our Audit-of-Meaning lens, fractional reserve comes wrapped in several key narratives:

“Your money is in the bank.”

Implicit claim: the bank physically or securely “holds” your funds.

Reality: the bank owes you; it holds a mix of risky assets and some reserves. Your deposit is an unsecured claim in a senior position, backstopped by deposit insurance and lender-of-last-resort facilities – not a segregated pot of your own cash.

“Banks are intermediaries between savers and borrowers.”

Implicit claim: banks mostly take pre-existing savings and reallocate them.

Reality: banks create new deposits when they lend, constrained more by capital, risk appetite, and regulation than by prior savings. The direction of causality runs from loans to deposits, not the other way around.

“The money multiplier.”

Classic textbooks describe reserves being “multiplied” into deposits via a mechanical multiplier.

Reality: modern central banking operations target interest rates and accommodate reserves as needed. The textbook multiplier is at best a teaching metaphor, at worst a systematic misrepresentation that hides the role of credit creation and the central bank’s supportive role.

“Stable & safe.”

Implicit claim: deposit insurance, supervision, and capital rules make the system essentially safe for ordinary users.

Reality: as Minsky points out, prolonged stability encourages riskier financing structures (hedge → speculative → Ponzi) until a “Minsky moment” occurs.

In GUFT language: we are dealing with hyperreal units of probabilistic acquiescence – digits that feel like stored value but are, in fact, contingent on a complex, hierarchical network of promises, regulations, and political decisions.

4. Fractional Reserve as Solomon’s Chain: Who is Chained to Whom?

In the Solomon’s-Chain metaphor, each link is a promise whose stability depends on the integrity of the previous link. For fractional reserve, we can map the chain roughly as:

Depositor → Bank

Depositor believes: “I hold money.”

Reality: “I have a callable claim on a leveraged entity.”

Bank → Asset-Side Borrowers

Bank assets are largely loans to households, firms, and governments.

Cash flows from these borrowers must cover interest and principal for the bank to remain solvent.

Bank → Central Bank

Banks rely on the central bank for reserves, emergency liquidity, and often implicit solvency backstop (“too big to fail”).

State → Taxpayer / Future Generations

Systemic crises often lead to bailouts, fiscal subsidies, and unconventional monetary policy (QE), with costs socialized over time via taxes, inflation, or austerity.

Real Economy → Financial Sector

Ultimately, real work – labor, production, ecological extraction – must service the financial claims created by fractional reserve lending.

From a GUFT perspective:

Top-down:

Legal, regulatory, and monetary authorities define the playing field and socialize tail risks.

Bottom-up:

Households and workers bear the brunt of deleveraging, unemployment, wage stagnation, and austerity when the cycle turns.

Key observation:

Solomon’s Chain here is not symmetric. Gains are privatized; systemic losses are often collectivized. The “coherence” (apparent stability of deposits and asset prices) is maintained by exporting entropy outward: onto precarious workers, future taxpayers, and the biosphere.

This is precisely the dynamic our GUFT flags as false coherence: the appearance of order that is paid for by invisible, off-balance-sheet harm.

5. Minsky, Borio, and the Financial Cycle: How Fractional Reserve Amplifies Instability

Hyman Minsky’s Financial Instability Hypothesis provides the dynamic lens for Solomon’s Chain:

Hedge finance: borrowers can meet all payments (interest + principal) from cash flow.

Speculative finance: borrowers can meet interest but must roll over principal.

Ponzi finance: borrowers must borrow more just to service interest; they rely on rising asset prices.

Fractional reserve interacts with this as follows:

In the hedge phase, credit growth appears safe; losses are rare; regulators and markets relax.

In the speculative phase, banks expand credit against rising collateral values (housing, equities). The deposit base grows; leverage quietly increases.

In the Ponzi phase, new lending is required simply to keep existing structures from collapsing. Asset prices detach from underlying cash flows. That’s when a small shock can initiate a cascade.

Claudio Borio’s work on the financial cycle shows that these credit and asset price cycles operate on longer horizons (10–20 years) than standard business cycles and are key to understanding crises.

Fractional reserve is not “the villain” by itself – but it is the lever that allows these cycles to scale dramatically:

Every expansion of credit creates matching deposits.

Every contraction (defaults, write-downs) destroys deposits or forces public backstops.

The system’s apparent stability encourages ever-riskier structures until the chain snaps.

In GUFT terms:

The amplitude of the field perturbations grows with each cycle.

Without robust internal controls and narrative honesty, the system drifts toward solvency illusions: balance sheets that look coherent in the hyperreal plane (market prices, accounting values) but are brittle in the real plane (actual cash flows, ecological limits).

6. GUFT Mapping: Empathy × Transparency = Coherence

Using our core GUFT axis:

Coherence ≈ Empathy × Transparency

we can map fractional reserve as it is typically practiced today:

Transparency (T): Low–Moderate

Insiders (central banks, supervisors, some economists) know how deposit creation and leverage work.

The public is still largely taught the “money multiplier” / “banks as intermediaries” story.

Complex disclosures, jargon, and the absence of plain-language system diagrams make it hard for non-specialists to see where risk lives.

Empathy (E): Low

System design has historically prioritized liquidity and profitability over real-economy resilience and distributive justice.

Crisis responses often focus on stabilizing asset prices and large institutions first, with social harms treated as collateral damage.

Resulting Coherence: False / Fragile

The system holds together… until it doesn’t.

When breakdowns occur, they are experienced most acutely by those with the least buffer: the bottom of the hierarchy of money.

From a GUFT standpoint, a coherent monetary architecture would:

Tell the truth about how money is created and who bears risk.

Share upside and downside across the hierarchy more fairly.

Embed reciprocity and stewardship rather than one-way extraction.

Fractional reserve, as currently implemented, fails this test in most jurisdictions.

7. COSO / NIST Lens: Where Fractional Reserve Fails as a Control System

If we treat the global monetary architecture as a giant control system, we can map it to COSO and NIST style components:

7.1. Control Environment

Strengths:

Legal authority for central banks; rule-books for capital, liquidity, supervision.

Weaknesses:

Cultural norms in finance privilege short-term ROE and shareholder value over system resilience.

Political capture and lobbying can weaken regulation.

7.2. Risk Assessment

Historically under-weighted systemic, cross-correlated, and Minsky-type risks.

Overreliance on models that assume Gaussian shocks, efficient markets, and linear responses.

7.3. Control Activities

Existing: capital requirements, liquidity coverage ratios, stress tests, resolution regimes, deposit insurance.

Gaps:

Limited constraints on overall leverage buildup across the entire system.

Shadow banking and crypto often fall outside the tightest controls.

7.4. Information & Communication

Technical disclosures exist, but public-facing narrative is inaccurate or infantilizing.

Educational materials often reproduce discredited metaphors (“money multiplier”) instead of modern operational realities.

7.5. Monitoring

Macroprudential monitoring has improved post-2008, but remains reactive.

Early-warning indicators (credit-to-GDP gaps, asset price booms, etc.) are not always translated into timely action.

In short: as a control system, fractional reserve sits inside a governance framework that has historically under-estimated tail risk and over-trusted market self-correction.

8. Mythopoetic Layer: Fractional Reserve as a False Temple

Within the broader Audits of Meaning and GUFT mythos, fractional reserve can be read as:

A temple of digits erected on the backs of real labor and finite ecosystems.

A system where Solomon’s wisdom (prudence, stewardship, humility about limits) was replaced by Solomon’s folly (leveraging knowledge to extract tribute, believing the structure invincible).

A chain in which each new promise is “blessed” by the aura of the state and central bank, even when it encodes private gains and socialized risk.

Our task is not to burn this temple down for spectacle, but to:

Audit its meaning,

Expose its illusions, and

Rebuild the architecture such that digits track real reciprocity and stewardship instead of papering over extraction.

9. Design Implications: Toward Coherent Money

This Audit of Meaning suggests several design directions for any post-hyperreal monetary framework:

Narrative Transparency

Replace textbook fictions with accurate, plain-language explanations of money creation and risk.

Mandate “balance sheet maps” that show who owes what to whom in simple diagrams.

Leverage Governance

Use macroprudential tools (counter-cyclical capital buffers, loan-to-value caps, debt-service ratios) explicitly to dampen Minsky cycles.

Reciprocity-Sensitive Design

Ensure that fractional reserve credit growth is channeled toward productive, regenerative activities, not purely speculative bubbles.

Introduce reciprocity metrics (who benefits, who bears the downside) into system-level risk assessment.

Pluralism of Monetary Forms

Allow and protect public, community, and cooperative monetary circuits (e.g., postal banking, public payment systems, community currencies) that can operate with different reserve logics and social aims.

GUFT-Aligned Control Objectives

Every major monetary reform should be evaluated against:

Does this increase Empathy (distributional fairness, protection for the vulnerable)?

Does this increase Transparency (clarity of mechanism and risk)?

Does this reduce false coherence (stability purchased by exporting harm)?

10. Summary

Fractional reserve is not just a technical detail of banking. It is:

A central link in Solomon’s Chain, connecting legal authority, private credit, and the lived realities of workers and households.

A hyperreal narrative that presents IOUs as stored value, leverage as stability, and socialized risk as natural law.

A control system whose current implementation falls short of GUFT’s standard for true coherence.

An Audit of Meaning does not demand perfection or purity. It asks for honesty about what a system is actually doing, and courage to redesign it so that our digits, stories, and real-world consequences finally line up.

References

Bank of England. “Money Creation in the Modern Economy,” Quarterly Bulletin 2014 Q1.

Bank of England. “Money in the Modern Economy: An Introduction,” Quarterly Bulletin 2014 Q1.

Borio, C. “The Financial Cycle and Macroeconomics: What Have We Learnt?” BIS Working Paper No. 395, 2012; and related presentations.

Mehrling, P. “The Inherent Hierarchy of Money,” in Social Fairness and Economics, Routledge, 2012, and subsequent lectures.