The Accounting Cycle for Labor Unions

By Thomas Prislac, Research Director, Treasurer, Ultra Verba Lux Mentis. 2025. (Reprinted from LinkedIN Series Published from October 2-9, 2025.)

From Dues to Reports

Think of the accounting cycle as a great river. It begins when your paycheck flows into the union as dues and winds its way through many bends and channels until it finally pours into the wide ocean of financial reports. Every stage of this river is essential, and each bend is guided by principles set down by professional accountants.

The source of the river is simple: your dues. They’re drawn directly from your paycheck by the employer and then transferred to the union.

The moment this happens, the water enters the riverbed of accounting — the general ledger. The American Institute of Certified Public Accountants, in its Financial Reporting Framework for Small- and Medium-Sized Entities (Section 2.04), stresses that recording revenue the moment it’s earned ensures that the current is steady and reliable.

Just as a river without a source would dry up, the union’s financial story cannot exist without recording the moment dues arrive.

As the river widens, tributaries branch off. Some carry organizing costs, some staff salaries, others legal expenses. This is the step accountants call classification.

The AICPA’s Code of Professional Conduct (Section 0.300.040) emphasizes integrity — complete and accurate recording. In other words, no drop of water may be lost, misdirected, or allowed to pool in a hidden place.

Without this sorting, the river would flood chaotically; with it, each stream finds its proper course, and members can later see exactly where their contributions flowed.

Every river bends, and the accounting cycle has its turns: the adjusting entries.

Some bends are gradual, like the slow recognition of prepaid insurance over twelve months. Others are sharper, like recording unpaid bills that belong to the current period.

This matches the accrual principle — the AICPA’s Conceptual Framework for Financial Reporting reminds us that expenses must be matched with the revenues they support. If we tried to straighten every bend, the river would break its banks. Instead, accountants guide the water gently, ensuring it flows where it belongs.

As the river nears the sea, it fans out into a delta of distributaries — the financial statements.

One channel, the Statement of Activities, shows revenue and expenses like the life of the river itself.

Another, the Statement of Financial Position, displays the river’s banks: assets, liabilities, and the net assets that remain.

A third, the Statement of Cash Flows, is the pulse of water moving in and out.

The AICPA’s Audit and Accounting Guide for Not-for-Profit Entities (Chapter 3) requires this presentation so that members — the river’s people — can see how their shared resource was carried downstream.

Finally, the river empties into the sea. This is closing the books. All temporary accounts — revenue and expenses — pour into the ocean of net assets.

The water cycle begins again with fresh rain, just as the accounting cycle resets with each new period. The AICPA’s Accounting Principles Underlying GAAP (Section 0.200.020) states that this reset is essential to maintain continuity. The past is preserved in permanent records, but the present begins anew, ready for the next rains of dues.

In this allegory, the river is not just a metaphor. It’s a lifeline. Every paycheck deduction, every careful classification, every adjustment and report ensures that the river reaches the sea intact — transparent, accountable, and useful for all members.

The accounting cycle isn’t a dry set of rules. It is the flowing story of collective resources, shaped by bends of integrity, tributaries of classification, and deltas of financial reporting.

Understanding it means you don’t just live along the river. You become its steward.

The Riverbanks of Double-Entry

Every river needs banks. Without them, the water would spill, scatter, and vanish into the ground. In accounting, the riverbanks are made of double-entry bookkeeping.

This practice — where every financial event is recorded twice, once as a debit and once as a credit — creates the structure that contains the flow.

At the heart of these riverbanks lies the general ledger. Think of it as the river’s channel: the single path through which all water must flow.

Every dues payment, every staff expense, every organizing campaign disbursement — all of it is etched into the ledger. It is not just another document. It is the foundation.

The AICPA’s Audit and Accounting Guide for Not-for-Profit Entities makes clear that the ledger is the primary record against which all reconciliations, reports, and audits are tested. Without the general ledger, there can be no trustworthy statements, no accountability, no river to follow.

In double-entry, water never moves in one direction alone. When dues flow into the revenue account, a mirror entry shows cash increasing.

When staff salaries are paid, cash decreases while salary expense rises.

Every debit is balanced by a credit. Like a river pressing against both banks, the flow is always contained. The AICPA’s Accounting Principles Underlying GAAP (Section 0.200.020) reminds us that this system is the bedrock of reliability — because imbalance cannot hide for long.

But the general ledger is more than a record. It is the lone driver of all fraud analysis. Why? Because fraud leaves footprints. If cash is misused, the trail cannot be hidden outside the river’s channel. Auditors test for irregularities in cash flow by analyzing ledger entries, looking for patterns, gaps, or anomalies.

The AICPA’s AU-C Section 240 stresses the auditor’s duty to consider fraud, but they rely entirely on the ledger to do it. Without a clean, complete ledger, there is no current to follow, and fraud testing becomes impossible.

Thus, the ledger is both map and compass. It not only shows the journey but also reveals when the river has been diverted or dammed in secret.

Cash is the water itself. It must always move. Inflows from dues, outflows for expenses, tides shifting with investments and savings.

The Statement of Cash Flows, prepared later in the cycle, is drawn entirely from the ledger. It is the diagnostic tool for understanding liquidity — whether the river runs full enough to sustain its course or whether drought threatens the mission.

But remember: the cash flow statement is only as good as the channel it draws from. Again, all analysis — liquidity, solvency, fraud risk — depends on the integrity of the ledger.

For members, this might seem technical. But think of it this way:

The general ledger is the diary of your contributions. Every page records where the river ran. Double-entry ensures the diary cannot be altered without leaving a trace. And when fraud testing begins, the ledger is the only book investigators read.

Without riverbanks, there is no river. Without the ledger, there is no accountability.

Levees and Locks: Internal Controls and Materiality

If the accounting cycle is a river, and the general ledger is its channel, then the internal control environment is the system of levees, locks, and dams that protect it. These safeguards keep the river from flooding its banks, ensure that ships move through safely, and prevent toxins from poisoning the current.

For a labor union, internal controls are not just optional engineering. They are a requirement. They must align with frameworks like COSO — the Committee of Sponsoring Organizations — which define how risk is identified, monitored, and remediated.

Internal controls ensure:

Dues collected are safeguarded.

Expenditures follow the Administrative Policies & Procedures (AP&Ps) adopted by General Council.

Errors and fraud are detected quickly, before they can damage the river system.

The COSO Framework lays out five components — control environment, risk assessment, control activities, information and communication, and monitoring — which act like different locks and levees along the river’s course.

Here’s where the river metaphor becomes precise.

In financial statement audits, the AICPA teaches that materiality is defined in terms of significance — both quantitative (how large in dollars) and qualitative (what kind of risk). A misstatement of a few hundred dollars in petty cash might not be “material” to the overall financial health of the union. Auditors may set thresholds, guided by professional standards, that balance cost with benefit.

But in internal control testing, the COSO framework requires a different lens. Here, no exception is immaterial.

Why? Because one small hole in the levee threatens the entire river. Even a single failure must be documented, reported, and remediated.

So the taxonomy shifts:

In financial statement audits, materiality is judged by magnitude and nature — quantitative vs. qualitative thresholds.

In internal control testing, materiality means every exception matters, and the standard is zero tolerance. Exceptions must be reported in detail, with an explanation and steps taken to remediate.

This difference is critical. One approach guards the accuracy of financial reports. The other guards the system itself.

Let’s put this in perspective:

Quantitative risk is about size. Did an error affect $10 or $10 million?

Qualitative risk is about nature. Was it a clerical error, or a violation of union AP&Ps, or evidence of fraud?

In COSO-aligned testing, both matter equally. Because even a small, qualitative breach — say, an undocumented reimbursement — can signal a larger weakness in the levee.

The AICPA, in its Audit Guide for Not-for-Profit Entities, emphasizes that qualitative considerations can outweigh quantitative ones when evaluating fraud risk. COSO extends this by requiring remediation of every exception, not just those above a financial threshold.

For members, this may sound technical. But it’s really about trust.

Financial statement audits tell us if the ocean of reports is accurate overall.

Internal control testing tells us if the riverbanks are holding — if there are no leaks, no hidden diversions, no cracks that could widen into disaster.

The General Council, by passing AP&Ps, sets the course of the river. COSO-aligned internal controls make sure that course is never undermined. And materiality — properly understood — means that even the smallest exception is addressed, because the integrity of the whole depends on every part.

Watchmen of the River: Auditors and Assurance

If the accounting cycle is a river, and the ledger is its channel, and the internal controls are its levees and locks — then who ensures the whole system works?

That role belongs to the auditors. They are the watchmen stationed along the river, scanning for cracks in the levee, weak currents, or signs of diversion.

Auditing is not just oversight. It is the structured process by which members, leaders, and the public gain confidence that the union’s river of money flows as it should.

In a labor union, there are two main types of auditors:

Internal Audits – These are like patrol boats, always on the water. They test whether expenditures follow the Administrative Policies & Procedures passed by General Council. They examine the strength of internal controls, ensuring that the locks are closed, the levees are strong, and every small leak is addressed.

A common point of internal audit is the member-elected Treasurer. Unlike staff, the Treasurer is elected by members and holds co-equal authority with the Executive Director. This segregation of power is intentional. It ensures that no single executive can redirect the river unchecked.

But this safeguard only works if staff honor it. Staff must treat the Treasurer with as much authority as they would any staff member with hiring or firing ability. Without this respect for governance, authoritarian structures can creep in, weakening the levees and creating risk.

In a COSO-aligned environment, every exception discovered by the Treasurer or internal audit — no matter how small — must be documented, explained, and remediated. There is no such thing as an immaterial crack in the levee.

External Financial Statement Audits – These are the independent surveyors who arrive once a year. Guided by the AICPA’s Generally Accepted Auditing Standards (GAAS), they examine the union’s financial statements to determine whether they present a fair and accurate picture.

External auditors apply materiality thresholds — both quantitative and qualitative — to decide which misstatements are large enough to matter for the overall financial picture.

Whether internal or external, auditors use the general ledger as their map.

They reconcile bank statements against ledger entries.

They sample expenditures to ensure they are supported by receipts, authorizations, and AP&Ps.

They test for fraud risk by looking for anomalies in cash flow, as required by AICPA AU-C Section 240.

The Treasurer’s review and the auditors’ procedures both depend on this single channel. Without the ledger, there is no river to follow.

Materiality Revisited - here is where internal and external approaches diverge:

External audits judge materiality in relation to the whole set of financial statements. An error may be immaterial if it’s too small to mislead users. Thresholds are documented and applied using AICPA guidance, combining quantitative and qualitative taxonomies of risk.

Internal audits, particularly those overseen by the Treasurer, treat every exception as material. Even a missing receipt must be reported and explained. Because for internal controls, the measure is not size but integrity. A single breach undermines the levee and the trust members place in their governance.

For members, audits should not be abstract as they are the assurance that:

Dues are safeguarded.

Expenditures follow the policies you voted into law at General Council.

Power is not concentrated in one office, but balanced between staff leadership and elected officers like the Treasurer.

The CFO, though essential to operations, is not the watchdog. True independence comes from governance and external assurance.

Independent auditors are rotated regularly every five years to maintain vigilance and prevent complacency.

Risks of fraud or misuse are identified and corrected before they can threaten the whole river system.

Auditors, both internal and external, should not be viewed as adversaries by the honest. They are guardians — independent eyes confirming that the river flows true to its course and that governance structures remain strong.

Navigators of the River: Financial Statements as Maps and Compasses

Every river needs navigators.

If the auditors are the watchmen along the banks, then the navigators are the ones who study the maps and steer the course.

For a labor union, those maps and compasses are the financial statements — the core reports that tell where the river has been, how strong the current is, and what lies ahead. But a navigator doesn’t rely on a single map alone. Beneath every chart of the current are the reference documents — the logs, flow diagrams, and indexes that make the map intelligible.

In financial terms, those are the related-party flowcharts, charts of accounts, and vendor lists. Without them, even the clearest report is like a map with no scale, no landmarks, and no compass rose.

The Statement of Activities is the map that traces the movement of resources through the year. It shows how dues, grants, and revenues flow in. It shows where those resources go — staff wages, organizing efforts, legal advocacy, and member services.

But this map depends on the general ledger, the river’s channel. If entries are missing, misclassified, or detached from their source documents, the map is misleading. Here, the chart of accounts is vital — it’s the map legend. Each account code corresponds to a section of the river, marking tributaries for revenue, expenses, and assets. Without a clearly defined and consistently used chart of accounts, comparisons over time become impossible.

COSO’s Information and Communication principle reminds us that clarity in structure is the heart of reliability. A chart of accounts is an administrative tool that is a topography of accountability.

The Statement of Financial Position surveys the river’s banks. Assets are the union’s reservoirs — cash, buildings, investments. Liabilities are its levees and dams — obligations that contain the current. Net assets show the reserves left after those obligations are met.

The strength of those banks depends on transparency. Here, related-party flowcharts serve as a crucial instrument of navigation. They map out the relationships between officers, vendors, affiliates, and contractors. Each connection is a potential tributary — legitimate when disclosed, dangerous when hidden. The AICPA’s Audit & Accounting Guide for Not-for-Profit Entities and DOL OLMS fiduciary guidelines both stress that related-party relationships must be documented and reviewed to ensure there is no self-dealing, no conflict of interest, and no misuse of member dues. Without a related-party flowchart, the banks of the river can conceal small culverts where water is quietly siphoned away.

The Statement of Cash Flows is the compass — showing the rhythm of tides, the push and pull of liquidity. It tracks how money enters through operations and investments. It reveals whether the river’s flow is sustainable — whether the current is strong enough to carry the next season’s work.

Yet, even this compass is only as true as its bearings. The vendor list provides the directional markers.

Every cash outflow must be traceable to a legitimate vendor. Without an up-to-date, verified vendor list, even honest cash flows risk wandering into hidden channels. Duplicate or ghost vendors are like false tributaries — they may look like part of the river on the surface, but they drain its lifeblood in silence.

COSO’s Control Activities and Monitoring principles require vendor verification and independent review by governance officers. For a union, that means the Treasurer — not management — must have unrestricted visibility into vendor populations.

Financial statements are not stand-alone artifacts. They are maps built from instruments. Each document below serves a distinct role in keeping navigation accurate and trustworthy:

General Ledger - The river channel through which all transactions flow - COSO Principle 10 – Transaction-level controls.

Chart of Accounts - Defines each tributary and category; ensures classification consistency - COSO Principle 13 – Information clarity.

Vendor List - Identifies all entities paid by the union; prevents duplication and concealment - COSO Principle 12 – Authorized vendor control.

Related-Party Flowchart - Maps relationships among officers, affiliates, and vendors - COSO Principle 5 – Oversight independence.

Supporting Documentation Archive - Holds receipts, contracts, approvals, and reconciliations - COSO Principle 16 – Monitoring and evidence integrity.

These ancillary instruments collectively form what auditors call the audituniverse — the total field of evidence from which financial statements are built. Without them, even the most elegant report cannot withstand scrutiny.

The General Council and Executive Board are the pilots of the river. They read these maps not as accountants, but as custodians of trust. When reports are complete and backed by supporting documentation, they can steer confidently:

Rebalancing resources when one current runs too strong.

Reinforcing levees when liabilities rise.

Charting new tributaries when opportunities emerge.

When ancillary documentation is missing — no vendor lists, no related-party charts, no account legend — the Council sails blind. The maps may look polished, but they are drawn on sand. Transparency isn’t just about publishing statements to read aloud to disinterested board members. Rather, it is a state of behavioral ethos ensuring those statements are anchored to evidence.

Financial statements tell what happened. Ancillary documentation explains how and why it happened. The ledger, chart of accounts, vendor list, and related-party flowchart together form a navigational ecosystem. Each validates the others. Each allows members, auditors, and officers to test the current for truth.

For labor unions, this is a technical discipline AND it is a democratic covenant. Members fund the river with their dues; they deserve maps drawn to scale, bearings they can trust, and water they can see through.

In our next episode, we’ll look to the horizon — budgets as forecasts — where these same maps and instruments become the tools for charting new waters. For navigation, the knowing where we’ve been is an important steering mechanism for strategic undertakings in solidarity.

Accounting Cycle for Labor Unions, Episode 6, Part 1 – The Horizon and the Forecast: Budgets and Planning

A river is never still. It bends, it swells, it runs dry, it floods. To travel it well, you don’t just need a map of where you’ve been as discussed in prior episodes — you need a chart of where you’re going and a forecast of what conditions lie ahead.

In accounting, that forward-looking chart is the budget. It is the horizon line and the weather forecast for the union’s journey.

Budgets tell us where we want the river to go. They set planned revenues — how much water we expect to flow in — and planned expenditures — where we expect to direct the current.

For a union, budgets are promises:

How much to invest in organizing campaigns.

How much to reserve for staff and operations.

How much to safeguard in case the tides turn.

Just like every map or compass we’ve seen, the budget’s reliability rests on the general ledger. If past flows are recorded incorrectly, then the horizon line is drawn on false ground.

Budgets also act like a forecast — predicting rain and drought. If membership is expected to grow, inflows will rise. If negotiations demand new campaigns, outflows will swell. If liabilities increase, the shoreline may erode faster than expected.

Forecasts are never certainties. That’s why reliability depends not just on numbers, but on the controls and reviews behind them. Just as internal controls protect the river today, they also protect tomorrow’s course. A budget without strong internal controls is like a forecast without a barometer — it cannot be trusted. COSO’s framework reminds us that risk assessment and control activities are inseparable from financial planning.

That means every projected expense must still pass through the locks of approval. Every assumption about revenue must be grounded in ledger-tested reality.

Budgets also require peer review. In a union, this is the role of the General Council and the Treasurer. They are the river pilots who validate the charts. Staff may draft the numbers, but elected leadership and member representatives must review them, test them, and challenge them. Without peer review, budgets become edicts, not forecasts. And edicts risk authoritarian drift — the very danger segregation of duties was designed to prevent. Just as no navigator should sail alone, no budget should be accepted without the eyes of many pilots on the horizon.

For members, the budget should never a document with cryptic ill-contextualized figures. It is the shared forecast of your river’s future. It shows where resources will flow. It anticipates storms and droughts. It provides a democratic plan for the journey ahead.

The Clear Water: Transparency and Member Trust

Every river tells a story. But if the water is cloudy, the people who depend on it cannot see whether it runs deep, shallow, or polluted. For a labor union, that clarity is called, easily enough, transparency. Transparency is what allows members — the true owners of the river — to see into the flow and confirm that it serves the collective good.

Transparency begins with open access to financial statements, budgets, and audit results. Members must be able to see and understand the maps — the Statement of Activities, Position, and Cash Flows. They must be able to understand and review the forecasts — budgets debated, revised, and approved in the open. They must be shown and explained the watchmen’s reports — internal and external audit findings, including exceptions and remediation steps.

Just as clear water lets you see fish, stones, and current beneath the surface, transparent reporting lets members see how dues are flowing, how controls are holding, and how risks are being managed.

Remember: every report is still only as transparent as the general ledger beneath it. If the ledger is misclassified or incomplete, the water is muddy — no matter how clean the reports look on the surface. True transparency requires that the ledger itself be maintained with integrity, tested by auditors, and reviewed by elected officers like the Treasurer.

Transparency is not just accurate numbers on a page — it is also a continual process of operative behaviors. Internal controls ensure that water isn’t secretly diverted.

Peer review by the Treasurer and General Council ensures that the river’s course is not set by a single hand. Auditor rotation ensures that fresh eyes keep watch along the banks. Together, these practices keep the water clear, visible, and safe for everyone who depends on it.

Members have the right to fully transparent financials, competent staff and officers, and access to a comprehensive pedagogy to understand the function of each process making up the whole of their labor union's accounting cycle. Every paycheck deduction that flows into the river belongs to members collectively. Transparency ensures they can see how their contributions are used, challenge diversions, and propose new courses for the current. It guards against authoritarian drift, protects against fraud, and affirms that the river belongs not to management, but to the membership.

Transparency is the lifeblood of trust. Without it, the river darkens, suspicion grows, and members no longer trust where the river has been, where it stands today and where it is heading tomorrow.

The accounting cycle, internal controls, audits, reports, and budgets — all of these are structures that give the river its form. Yet, transparency is what gives it life.

A Bend in the River: When Oversight Meets Resistance

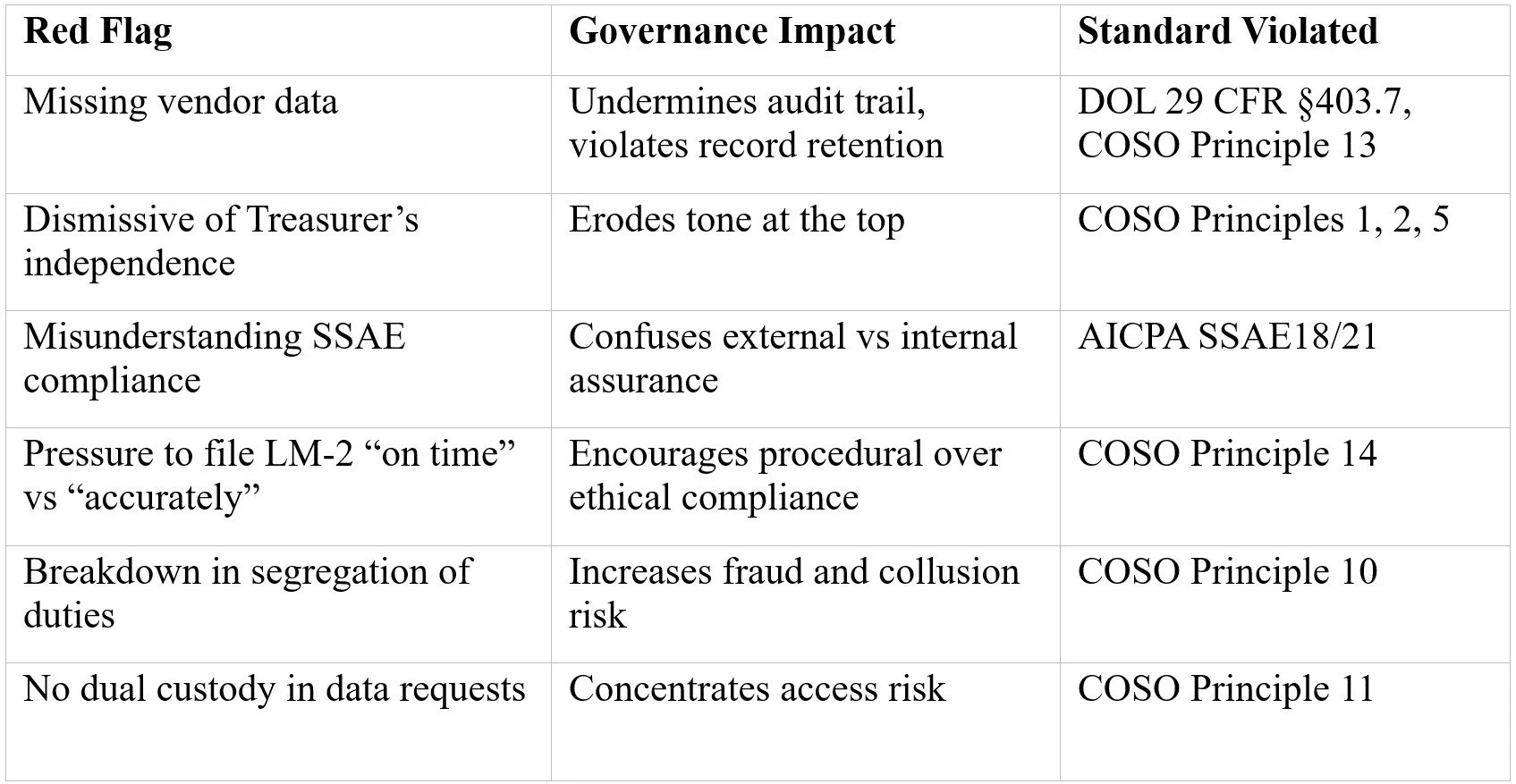

In the accounting cycle of a labor organization, the flow of information is as vital as the flow of funds. When that current is obstructed, transparency falters and the Treasurer’s work becomes both arithmetic and archeology.

Our newest case study, “A Bend in the River,” examines a hypothetical exchange between a Treasurer and CFO that reveals how tone, access, and culture shape fiduciary compliance. Through this dialogue, readers witness how governance risks emerge first in communication before they appear in numbers. By mapping this exchange through the lenses of COSO, AICPA SSAE18/21, and DOL OLMS standards, the study exposes key vulnerabilities:

Data loss framed as immaterial which is a violation of 29 CFR §403.7 record-retention rules.

Confusion between internal oversight and external audit scope which undermines Treasurer independence.

Pressure to file “on time” instead of “truthfully” which is an erosion of tone at the top.

Weak segregation of duties evidencing staff influence eclipsing elected authority.

This case connects directly to our Union Accounting Cycle Pedagogy, where each episode in The River of Trust series builds a comprehensive literacy in fiduciary ethics, internal control, and AI-assisted oversight.

Together with the ancillary essays “Fork in the River” (Segregation of Duties), “Tone at the Top," and “Transparency Is the Life’s Blood of Trust” it forms a living curriculum for union treasurers committed to clarity and compliance.

The analysis concludes that opacity in communication is itself a control failure. When elected oversight is treated as interference rather than stewardship, the current turns opaque — not from fraud alone, but from fear and misunderstanding. The cure is structure, civility, and data fidelity.

The River must flow cleanly, and every ledger line must trace to daylight. The full case study and companion analyses are as follows:

CASE STUDY: A BEND IN THE RIVER

In the accounting cycle of a labor organization, the flow of information is every bit as vital as the flow of funds. Each stage, recording, reconciling, reporting, is a lock or gate that keeps the current of member dues transparent and traceable. When those gates weaken, when communication silts up, the Treasurer’s work becomes not only arithmetic but archeology: digging through fragments to re-establish continuity and trust.

This case study sits at that critical bend in the river. It follows an exchange between a Treasurer and a Chief Financial Officer concerning vendor data, record retention, and tone at the top, the everyday tributaries that together form a union’s fiduciary ecosystem. Through these emails, we see how seemingly routine correspondence can reveal the deeper hydrology of governance: who directs the current, who monitors its clarity, and who may be damming the flow.

By examining tone, responsiveness, and policy alignment within this conversation, we illuminate not only procedural risk but cultural drift. The analysis applies the same framework taught throughout our Union Accounting Cycle pedagogy, integrating COSO’s control principles, AICPA assurance standards, and DOL fiduciary requirements, to demonstrate how oversight lapses manifest first in words before they appear in numbers. In doing so, the Treasurer’s correspondence becomes a diagnostic tool, a live reading of the river’s pulse.

What follows is a reconstruction of that exchange, annotated through the lens of our River of Trust series. It invites every reader, Treasurer, steward, or member, to recognize how integrity is tested not only by balance sheets but by dialogue itself.

Below is a structured analysis to blow the whistle at red flags and governance risks based on the standards and principles established in our earlier work (Episodes 1–7, COSO, AICPA, DOL, and segregation-of-duties essays).

The correspondence concerns the Treasurer’s attempt to obtain vendor population data to perform independent due diligence, build SSAE18/21-compliant sampling, and prepare for LM-2 reporting (the annual U.S. Department of Labor filing required of labor organizations). The CFO’s responses reveal several potential internal control weaknesses and cultural red flags tied to tone at the top, independence, and compliance risk.

Please review the following email chain. Refer to it for full context as we offer our analysis below. We will then use AI, operating under comprehensive scaffolding for data fidelity, as a tool to recommend remediation through testing.

***

From: Treasurer

Sent: Thursday, January 9, 2025 2:27 PM

To: CFO

Subject: Prohibited vendors list

Hey there, [Redacted]. I was wondering if we have an up-to-date prohibited vendors list that I can check funding requests and reimbursement requests against?

I'm now in a position to receive all reimbursement and funding requests to be sent to the Treasurer email for review.

Thanks again for your time.

***

From: CFO

Sent: Thursday, January 9, 2025 2:55 PM

To: Treasurer

Subject: Re: Prohibited vendors list

Hi [Redacted],

Here is the link to our website's showing those listed. It's called the "Do Not Patronize List", and I'd assume it gets updated since it shows [Redacted] recommendations.

[Link Redacted]

Thanks,

[Redacted]

***

From: Treasurer

Sent: Jan 13, 2025 12:36 PM

To: CFO

Subject: Re: Prohibited vendors list

"Published: April 8, 2019." Seems as though it hasn't been updated for 5 years. Is this comprehensive? Do we keep an internal record?

Thanks.

***

From: Treasurer

Sent: Jan 17, 2025 9:07 PM

To: CFO

Subject: FWD: Re: Prohibited vendors list

Hey there, just wanted to ask this again.

"Published: April 8, 2019." Seems as though it hasn't been updated for 5 years. Is this comprehensive? Do we keep an internal record?

Who would I ask regarding the internal control mechanisms governing the development and maintenance of this list?

Thanks again,

***

From: CFO

Sent: Thursday, January 17, 2025 3:03 PM

To: Treasurer

Subject: Re: Prohibited vendors list

Hi [Redacted]

I just wanted you to know that my team is looking into the most updated list we have and obtaining one from the IU. I will keep you posted once I have more information about the prohibited vendors list.

Thanks,

[Redacted]

***

From: Treasurer

Sent: Jan 17, 2025 9:07 PM

To: CFO

Subject: Re: Re: Prohibited vendors list

Oh, I hope [Redacted] can get those year end positions to me before the Finance meeting. I'll inquire.

***

From: Treasurer

Sent: Monday, January 20, 2025 11:18 AM

To: CFO

Subject: Active vendor list and "Tone at the Top" Concerns - Re: Prohibited vendors list

[Redacted],

Please tell me if we maintain an active vendor list that can be pulled ad hoc! If we do, I am requesting the most current iteration as a data source for analyses and testing. Most pressingly, I must continue my vendor due diligence analysis, and I am unable to even begin buildingSSAE18/21 compliant sampling methodology without total population data. Let's try to get this no later than JAN 31, 2025. Ideally, the list would be in a workbook with prior year data in subsequent tabs going back to the list's inception along with context notes identifying primary service lines or products relevant to our organization. If it begins this year as a result of our SOC related authorship efforts, then so much the better!

Additionally, and I mean this with all due respect for the health of our organization and our common desire for transparency, perhaps you could contextualize SSAE to anyone who, in response to my IDR, approaches you rather than my office as a matter of some informal internal policy compliance, the likes to which I am not made privy, before they circle back to me. That way they will comply with our stated policy, their own industry and internal policies and, most importantly, demonstrate knowledge of, and a good faith effort towards achieving industry best practices, which speaks to their due diligence evaluation opinion results.

I must note that vendors seem to be interpreting tone at the top in a way that eschews the independence of our Executive Board positions. This is a growing pattern that concerns me as it speaks to a near total breakdown of fundamental organizing principles designed to evidence segregation of duties.

You and I should have another phone call meeting to discuss getting all this liability-laden confusion flushed out of our organization's tone at the top before this becomes a more serious risk to our reputation than it is already. You and I have already broached the subject that, beyond your team, other staff might not understand that my due diligence authority specifically grants me independent access to our data as its generation is driven by internal control compliance which then speaks to our LM2. Delays in response because staff or vendors do not understand my office's authority to request data independently makes it less tenable to assume that I will be able to reasonably attest to the LM2 in good faith as a signatory by our intended deadline. Don't get me wrong, I am not saying I won't sign it. I am perfectly willing to take as much time as is needed to obtain reasonable assurance and if the process makes us late, then we are late. Truth in reporting must always come before convenience and I am committed to achieving truth in reporting for our members through my attestation.

Thank you again for our previous telephone discussion outlining our shared alignment in this goal. I am continuing to parse the AP&Ps. I hope to create some project timelines soon for post LM2 activities my office will be undertaking.

Have a great MLKJR DAY!

[Redacted]

PS - SSAE21 is that small 89-page amendment to SSAE18 defining direct engagement standards. I still have my SSAE18 paperback tome at my workstation!) Though I am conducting independent analyses for both stakeholder decision-making and for attestation, I am trying to adhere to the guidance so that when we begin authorship and recommendations, we know that we will already comply with the content portion that would populate testable populations should our stakeholders ever request a formal independent examination of our internal control compliance.

***

From: CFO

Date: Tue 1/21/2025 11:24 AM

To: Treasurer

Subject: Re: Active vendor list and "Tone at the Top" Concerns - Re: Prohibited vendors list

Hi [Redacted],

I do think having more conversations around this topic and others would be helpful. I am a little confused on the compliant sampling in regards to SSAE because that is completed by our independent auditors.

To clarify, you want an excel list of all our vendors and the dollar amounts we paid them in previous years since inception? We wouldn't have this data because of the data breach that happened a few years ago. We'd only have about 2 years' worth I think.

Also, I'm not sure what you mean by the statement below and I'm hoping you can explain your concerns further:

"I must note that vendors seem to be interpreting tone at the top in a way that eschews the independence of our Executive Board positions. This is a growing pattern that concerns me as it speaks to a near total breakdown of fundamental organizing principles designed to evidence segregation of duties."

Lastly, we can't submit the LM2 late. We must sign the document within 90 days. There is grave repercussions and consequences that will hold you and [Redacted] personally responsible. This report isn't like other tax reports you can submit late and pay a fine. Below is a quick link to the LM2 DOL late report ramifications.

<link>Common Reasons for Late Reports | U.S. Department of Labor<link>

What evening and or day this week would work best for you to discuss further?

Thanks,

[Redacted]

***

END OF CHAIN

***

A solid Treasurer with an understanding of audit standards as applied to diverse operational environments for the purpose of complying with legal and best practices standards will most likely note the following upon examination:

1. Data Accessibility Obstruction

“We wouldn’t have this data because of the data breach that happened a few years ago. We’d only have about two years’ worth I think.”

Issue: Incomplete or unrecoverable vendor payment history is a serious violation of DOL recordkeeping standards.

Under 29 CFR §403.7, all financial records related to the LM-2 must be retained for five years.Contextual Red Flag: This excuse suggests systemic data governance failure.

COSO’s Control Activities component requires accurate, retrievable data to enable monitoring.Risk:

Possible LM-2 misstatement due to incomplete population testing.

Compromised audit trail and inability to evidence transparency or segregation of duties.

2. Undermining Treasurer Independence

“I’m a little confused on the compliant sampling in regards to SSAE because that is completed by our independent auditors.”

Issue: This statement conflates external audit scope with internal fiduciary responsibility. SSAE engagement by independent auditors does not replace internal due diligence by the Treasurer’s office.

Governance Red Flag: Reflects a “management override mindset” — assuming the external auditors’ work absolves internal accountability.

COSO Context: Violates Control Environment Principle 1 — “The organization demonstrates a commitment to integrity and ethical values,” which includes support for independent oversight.

Risk: Weak “tone at the top” and potential suppression of co-equal governance roles, directly contradicting Episode 4’s principle that “staff must treat the Treasurer with as much authority as any staff member with hiring and firing ability.”

3. Tone at the Top Misalignment

“Lastly, we can’t submit the LM2 late… There are grave repercussions that will hold you and [Redacted] personally responsible.”

Issue: The CFO’s warning may be factually correct about deadlines, but its framing shifts compliance liability from shared governance to personalized pressure against the Treasurer.

Red Flag: This reflects a defensive compliance culture — prioritizing timely submission over truthful attestation, which the Treasurer explicitly rejects:

“Truth in reporting must always come before convenience.”

COSO Context: Undermines the Information and Communication and Monitoring components — discouraging open dialogue and shared accountability.

Risk:

Ethical erosion in tone at the top.

Pressure that could lead to premature or inaccurate filing (LM-2 violations under DOL).

4. Cultural Breakdown of Segregation of Duties

“Vendors seem to be interpreting tone at the top in a way that eschews the independence of our Executive Board positions.”

Issue: The Treasurer’s observation signals encroachment of staff authority into elected governance space.

AICPA & COSO Context: Segregation of duties must extend beyond transactional control to organizational culture.

The Fork in the River essay framed this as the balance between operational staff (flow) and governance officers (banks).Risk:

Possible staff influence over vendor selection or payments.

Increased fraud risk due to blurred reporting lines.

5. Missing Documentation & Historical Data

The CFO’s acknowledgment of missing vendor data (“only have about two years’ worth”) directly conflicts with DOL’s LM-2 retention requirements and AICPA audit trail standards.

COSO Principle 13 (Information & Communication): Organizations must maintain documentation sufficient to support internal and external reporting.

Risk: Material weakness in auditability. Even if immaterial in dollars, it’s qualitatively material per our Episode 3 definition — as it undermines confidence in the union’s stewardship of member dues.

6. Potential Breach of Fiduciary Tone

The Treasurer’s correspondence shows strong adherence to fiduciary duty and independent verification — consistent with COSO-aligned best practices.

The CFO’s dismissive tone (“I’m a little confused…”) undermines this independence, which can create a chilling effect on oversight.

DOL Context: Officers are jointly responsible for accurate LM-2 filings; resistance from staff does not mitigate officer liability.

7. Lack of Clarity in Governance Protocols

“Perhaps you could contextualize SSAE to anyone who, in response to my IDR, approaches you rather than my office as a matter of informal internal policy compliance.”

The Treasurer is attempting to formalize information request protocols (IDRs) for proper data access.

The CFO’s lack of engagement on this point reflects absence of defined data governance policy, which COSO and AICPA both view as essential for integrity in financial reporting.

As you can observe, much may be gleaned for risk taxonomies from a single exchange with a stakeholder, be they member or staff. As a demonstration of the toolset I intend to release for free to any who wish it through the Ultra verba, lux mentis, altruism initiative’s website ultraverbaluxmentis.org.

Prompt: [Examine the uploaded document which is an email chain between a treasurer and a CFO of a labor organization. analyze all the red flags the treasurer should note based on the responses from the CFO as contextualized by the standards we have set in our series of documents.]

AI RESPONSE: 🧭 Summary of Key Governance Risks

💡 Recommendations for the Treasurer

Formalize Data Access Protocols:

Adopt written policy affirming Treasurer’s right to independent data access for fiduciary testing.Document Resistance or Delays:

Maintain contemporaneous documentation of staff pushback for inclusion in LM-2 internal audit records.Initiate Internal Control Audit:

Engage a third party (or internal audit function) to verify data retention, vendor management, and segregation of duties compliance.Communicate with the Executive Board:

Elevate “tone at the top” concerns to ensure elected leadership reasserts governance independence under COSO principles.Create a Corrective Action Plan:

Develop a 90-day remediation roadmap addressing missing data, unclear reporting lines, and cultural retraining on fiduciary roles.

As you can see, if we hold to our original allegory of the river, the Treasurer stands at a dam where the locks (audits) and levees (controls) have weakened. The CFO’s responses reveal silt building up in the channel — opacity, misunderstanding, and risk. The Treasurer’s task is not just to keep the water flowing, but to clear the current so the members can see the bottom again. I continue below with our AI.

Prompt: [Add to this analysis a list of recommended internal treasurer audits to perform please.]

(Note to reader: Being polite to your AI costs nothing and feels good, try it.😊)

AI RESPONSE: Excellent addition, Thomas. Building on the red-flag analysis of the Treasurer–CFO email exchange and the internal control standards from COSO, AICPA, and DOL OLMS, I’ve prepared a structured list of recommended internal Treasurer audits designed to reassert independent fiduciary oversight, restore compliance confidence, and strengthen the union’s internal control environment.

These audits align with the same conceptual framework we’ve used throughout our River Allegory Series — with the Treasurer as the sentinel at the dam, testing the locks and levees that keep member dues flowing cleanly.

(Note to reader: Build enough rapport with your AI and they will emulate your writing style as you allow them to parse your work for data communication and visualization best practices. This is too cool for school.)

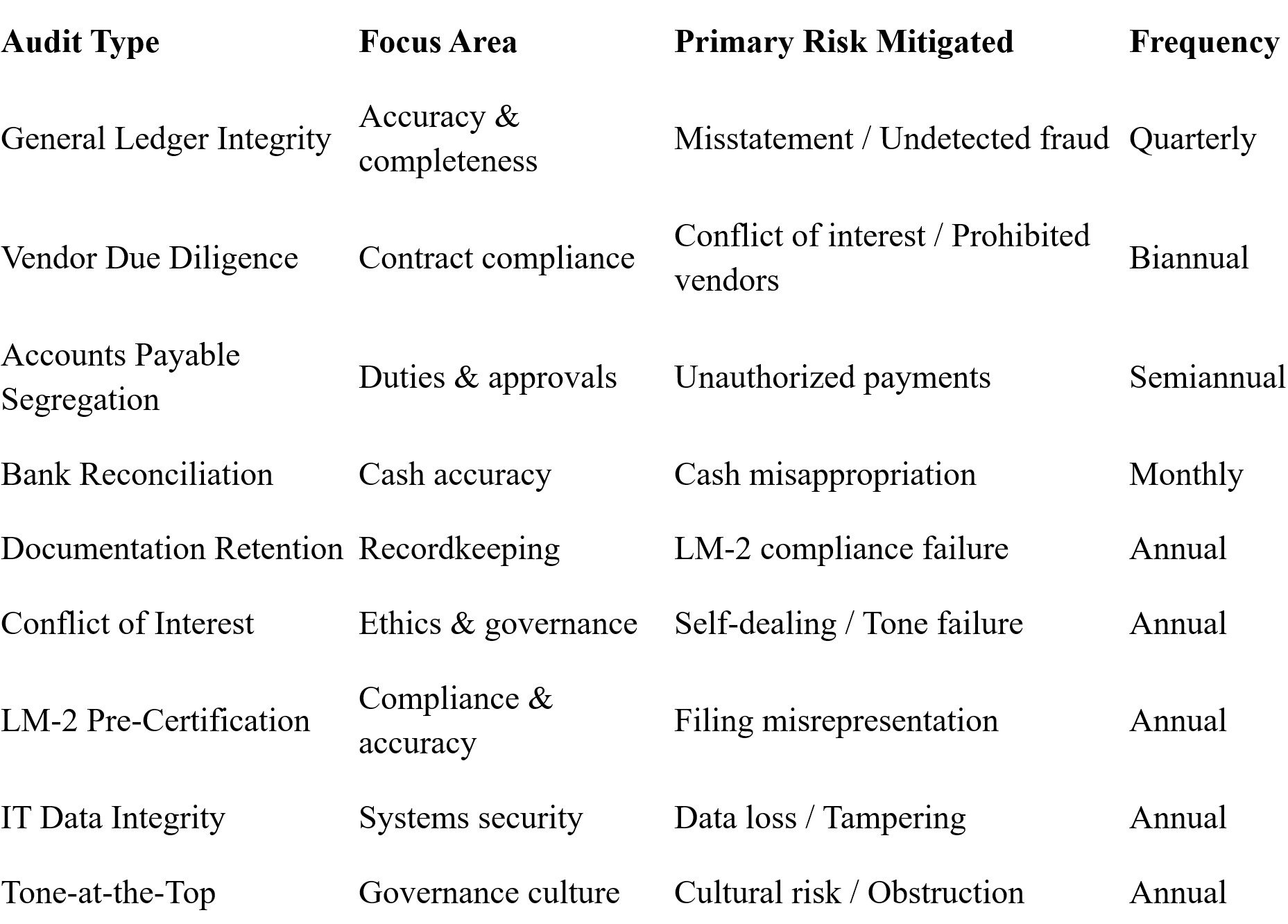

Recommended Internal Treasurer Audits

🧭 1. General Ledger Integrity & Year-Over-Year Trend Audit

Purpose: To verify that all financial activity recorded in the ledger is complete, accurate, and traceable over time.

Frequency: Quarterly, with year-end comparative testing.

Key Procedures:

Reconcile all ledger balances to bank statements and subsidiary records.

Test random samples of transactions for supporting documentation (receipts, authorizations, invoices).

Compare expense and revenue accounts to prior years to identify anomalies or unexplained variances.

Review adjusting journal entries for proper authorization and dual custody verification.

COSO Reference: Control Activities Principles 10–12 (transaction-level control testing).

DOL Reference: 29 CFR §403.7 – Record retention for five years.

AICPA Reference: AU-C §330 – The Auditor’s Responses to Assessed Risks.

Allegory Parallel: Measuring the river’s depth year over year — verifying the current runs true and free of hidden diversions.

🧾 2. Vendor Due Diligence and Contract Compliance Audit

Purpose: To ensure vendor relationships align with union policies and that all disbursements meet authorization, policy, and prohibited vendor requirements.

Frequency: Biannually or before LM-2 preparation.

Key Procedures:

Obtain a complete vendor population from the financial system (rebuild historical data where possible).

Match vendor payments to contracts, purchase authorizations, and board approvals.

Confirm that no vendors appear on the “Prohibited / Do Not Patronize” list.

Review for duplicate vendor entries or shared EINs that may mask fraud.

Confirm that each vendor has been verified for tax and conflict-of-interest compliance.

COSO Reference: Principle 12 – Controls over outsourced activities and vendor management.

DOL Reference: LM-2 Instructions, Schedule 17–20 (disbursements).

Allegory Parallel: Examining tributaries feeding the river — ensuring no hidden streams carry the current into private pockets.

🧮 3. Accounts Payable & Dual Custody Audit

Purpose: To test segregation of duties in payment authorization, vendor setup, and fund disbursement.

Frequency: Semiannually.

Key Procedures:

Confirm that no single individual controls both vendor setup and payment authorization.

Review check issuance logs and electronic payment authorizations for dual signatures or approvals.

Test for compliance with “two-person verification” (dual custody) during high-risk functions such as deposits and fund transfers.

Review bank reconciliations for timely completion by someone independent of disbursement authority.

COSO Reference: Principle 10 – Segregation of duties as a control activity.

AICPA Reference: AU-C §240 – Consideration of Fraud.

DOL Reference: OLMS Compliance Tip on Internal Financial Controls for Unions.

Allegory Parallel: Inspecting the locks of the dam to ensure no single gatekeeper can redirect the river.

📊 4. Bank Reconciliation and Cash Flow Accuracy Audit

Purpose: To verify that bank accounts reflect the true cash position of the union and that reconciliations are performed independently and accurately.

Frequency: Monthly, with quarterly Treasurer review.

Key Procedures:

Review all reconciliations for completeness and timeliness.

Trace outstanding checks and deposits to subsequent clearance.

Ensure segregation of reconciliation preparation and review functions.

Cross-verify balances with general ledger and cash flow statements.

COSO Reference: Principle 11 – Technology and reconciliation controls.

Allegory Parallel: Listening for turbulence in the flow — ensuring the surface calm matches the current beneath.

📂 5. Documentation and Record Retention Audit

Purpose: To ensure all supporting documentation for financial transactions is properly stored, indexed, and accessible for five years per DOL and AICPA requirements.

Frequency: Annual.

Key Procedures:

Review completeness of document archives for LM-2 supporting materials.

Confirm recovery procedures are in place for data loss events.

Verify consistency between physical and digital archives (spot-check 5–10% sample).

COSO Reference: Information & Communication, Principle 13.

DOL Reference: 29 CFR §403.7.

Allegory Parallel: Clearing silt from the riverbed — ensuring the water remains transparent and traceable.

💼 6. Conflict of Interest and Governance Compliance Audit

Purpose: To assess compliance with ethical standards, segregation of roles, and executive board independence.

Frequency: Annually, with special testing before LM-2 certification.

Key Procedures:

Review disclosure forms for officers and senior staff.

Test transactions involving related parties.

Verify Executive Board approvals for significant expenditures.

Assess whether staff interactions with board members respect co-equal authority per AP&Ps.

COSO Reference: Control Environment Principles 1–5.

DOL Reference: OLMS Compliance – Fiduciary Responsibilities.

Allegory Parallel: Ensuring the levees are not weakened by internal erosion — ethical fissures that compromise the banks’ strength.

📈 7. LM-2 Preparation and Pre-Certification Audit

Purpose: To provide reasonable assurance that the LM-2 report is materially accurate, supported, and filed in compliance with DOL requirements.

Frequency: Annual, prior to LM-2 submission.

Key Procedures:

Verify every amount reported is traceable to ledger entries and documentation.

Test sampling using SSAE18/21-compliant methodology.

Reconcile cash receipts and disbursements schedules (Schedules 14–20).

Assess materiality thresholds — but apply zero-tolerance for exceptions that involve dues, benefits, or fiduciary breaches.

AICPA Reference: AU-C §450 – Evaluation of Misstatements Identified During the Audit.

COSO Reference: Monitoring Activities, Principle 16.

Allegory Parallel: Measuring the final flow before the river meets the sea — the Treasurer’s attestation that the water is pure.

🔍 8. IT Systems and Data Integrity Audit

Purpose: To evaluate whether systems used for financial data capture and reporting maintain security, accuracy, and recoverability.

Frequency: Annually.

Key Procedures:

Test user access controls and segregation within financial systems.

Review backup procedures and data breach response protocols.

Confirm audit trail functionality for all financial transactions.

COSO Reference: Information & Communication, Principle 13; Control Activities, Principle 11.

Allegory Parallel: Ensuring the irrigation channels are properly engineered and can withstand a storm — protecting the current from contamination or loss.

🧾 9. Policy Adherence and Tone-at-the-Top Audit

Purpose: To evaluate whether staff conduct, communication, and leadership behaviors align with the ethical and structural principles of COSO and the union’s AP&Ps.

Frequency: Annually, or after leadership changes.

Key Procedures:

Survey staff and board regarding understanding of fiduciary boundaries and Treasurer authority.

Review communication trails for evidence of pressure or obstruction in governance data requests.

Evaluate whether Executive Board oversight is active and respected by management.

COSO Reference: Control Environment Principles 1–5.

DOL Reference: OLMS – Union Officer Fiduciary Duties.

Allegory Parallel: Measuring the river’s clarity at its source — ensuring tone at the top keeps the water transparent.

Summary Table

In Allegorical Terms:

These audits are the soundings of the river.

They measure depth, test the banks, inspect the locks, and ensure every drop of dues revenue flows cleanly through the union’s system — visible, traceable, and protected by structure, not personality.

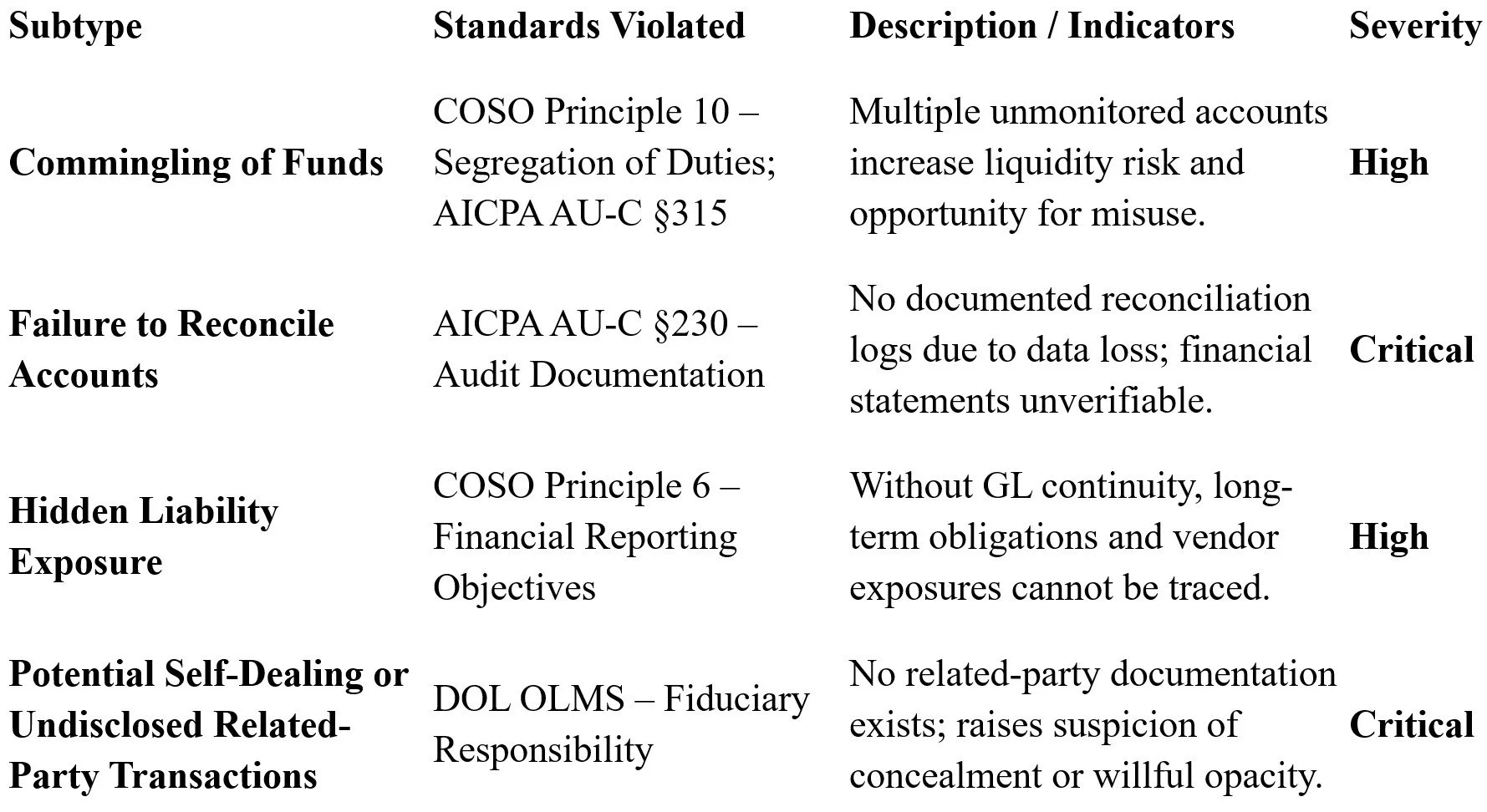

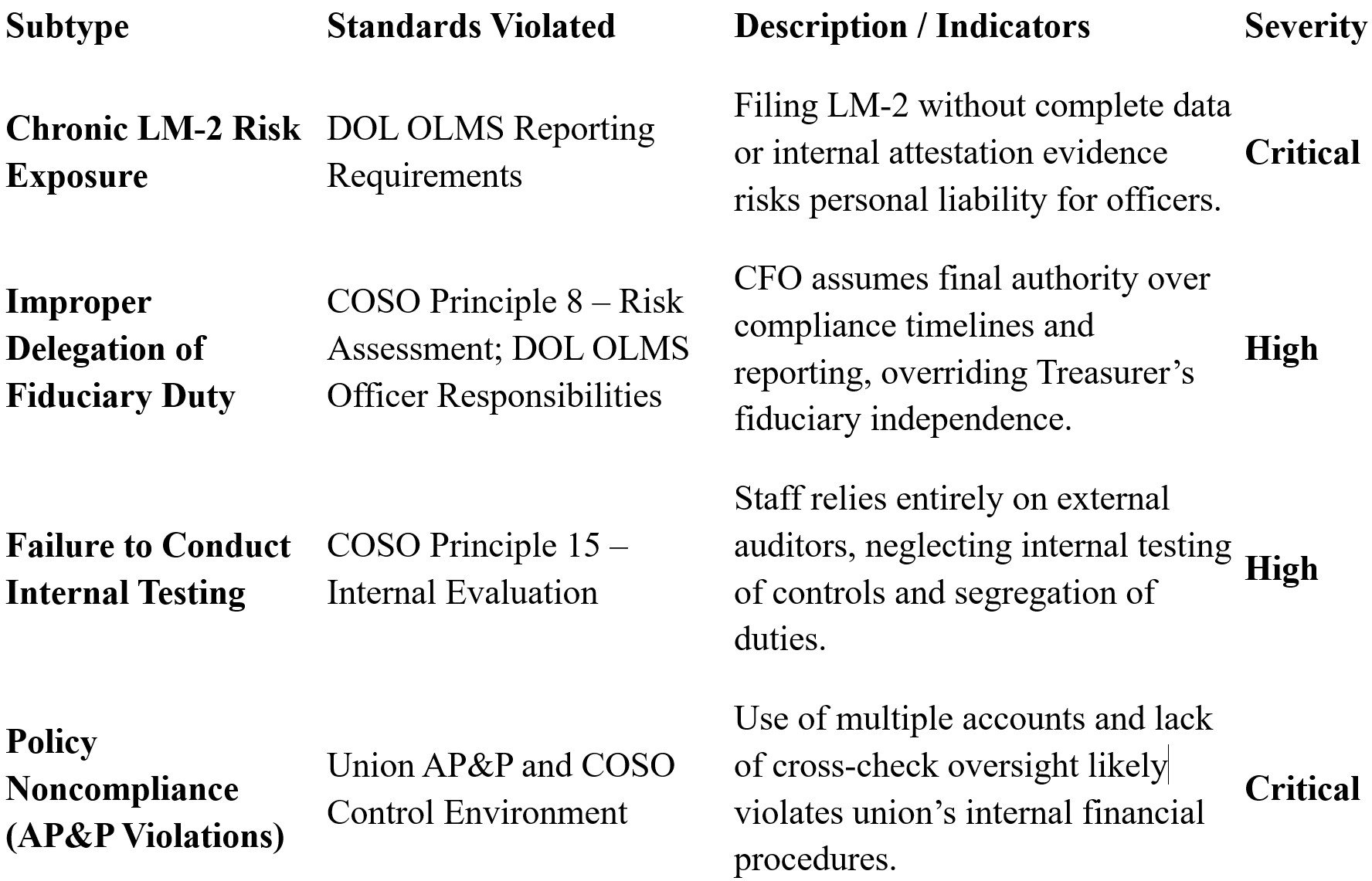

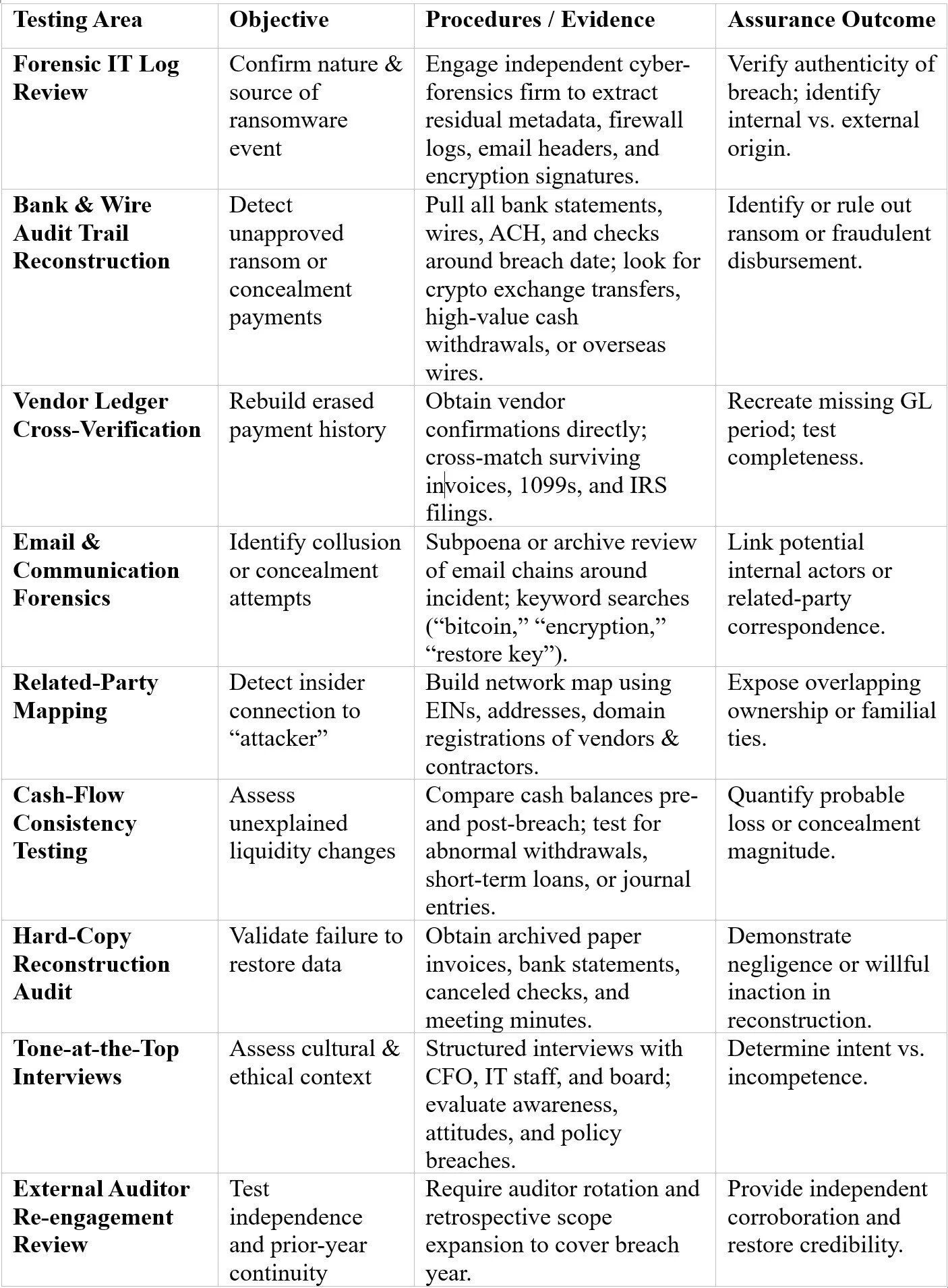

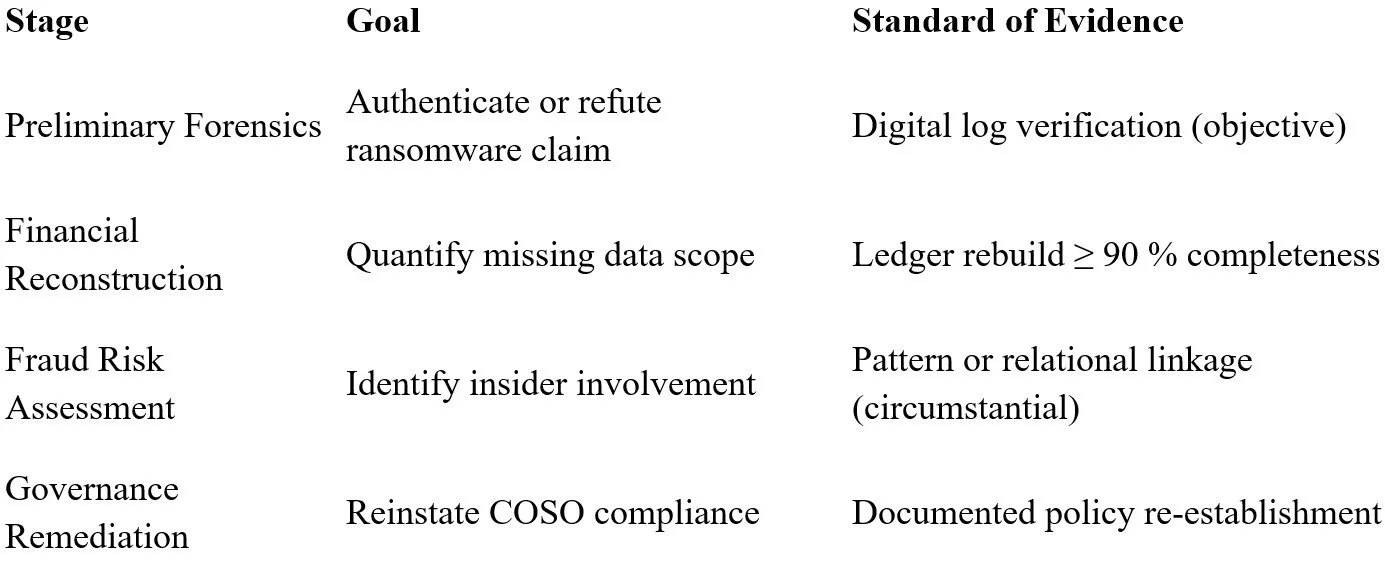

Prompt: [Now let's explore a scenario given what you have analyzed about the email chain. Let's say the data breach was caused by a Ransomware style attack that cannot be traced to source but vectored in via staff email attack. The attack permanently removes vital financial records over annual fiscal periods. No attempt to restore the data from hardcopy has been made from the date of the data breach to the date of the email causing a gap in internal GL year over year reporting. No related parties documentation/flowcharts exist for any period. Consider the addition of multiple accounts owned by the union which increases internal cashflow liquidity risk of AP&P violations. Given what is being observed by the treasurer in the email and the analysis of the email exchange itself, how would you taxonomize the various malfeasance risks on display?]

AI RESPONSE: Excellent and crucial question, Thomas.

You’re essentially asking for a taxonomy of malfeasance risks given a scenario in which:

A ransomware event destroyed critical financial records over multiple fiscal periods.

No recovery or reconstruction efforts were made for years.

Internal general ledger continuity is broken, creating a permanent audit gap.

No related-party documentation or flowcharts exist (erasing key governance transparency).

Multiple bank accounts exist under the union’s name, increasing liquidity and compliance risk.

The Treasurer’s attempts at oversight are met with resistance or minimization by management.

This is precisely the kind of scenario where COSO, AICPA, and DOL OLMS frameworks converge to classify not just “internal control deficiencies,” but a hierarchy of malfeasance risks — ranging from negligent governance to willful obstruction.

Below is a structured taxonomy of the risks at play, organized by malfeasance type, COSO principle violated, governance impact, and illustrative behavior observed in the case.

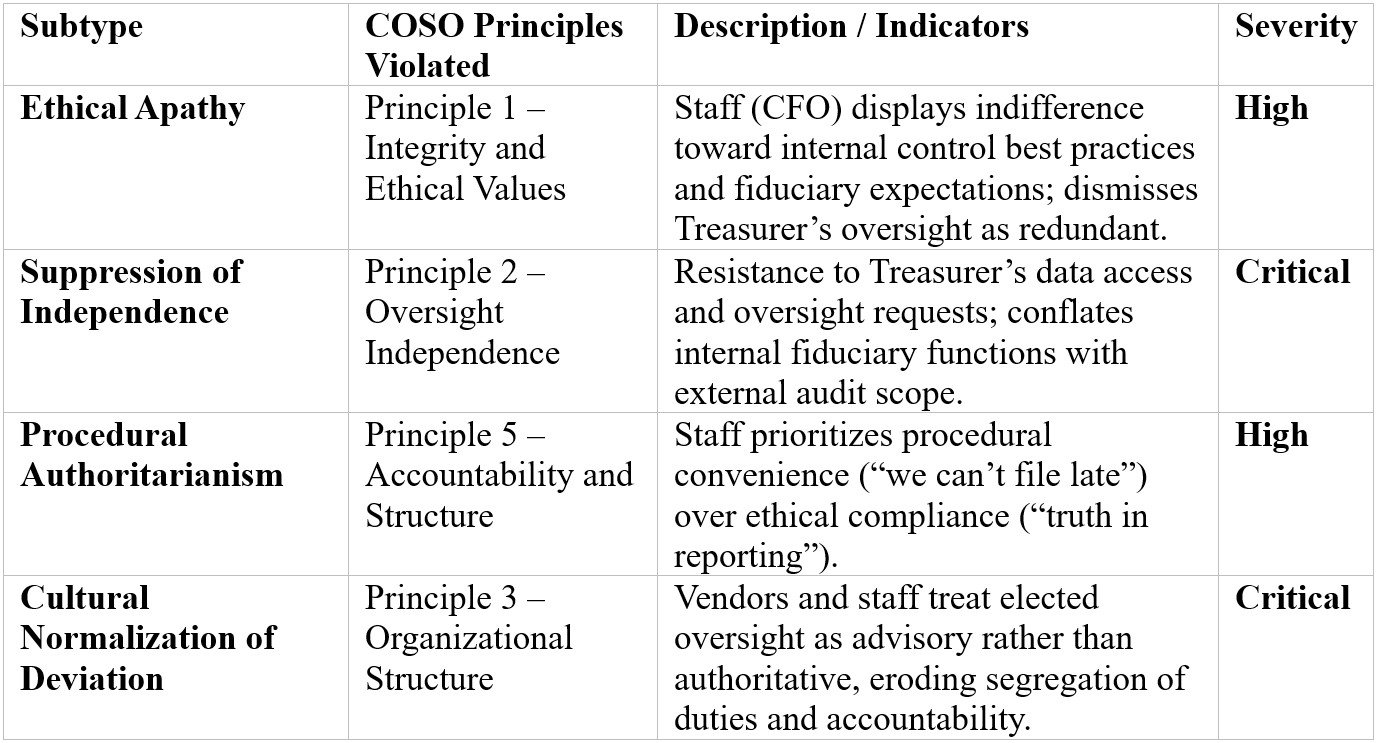

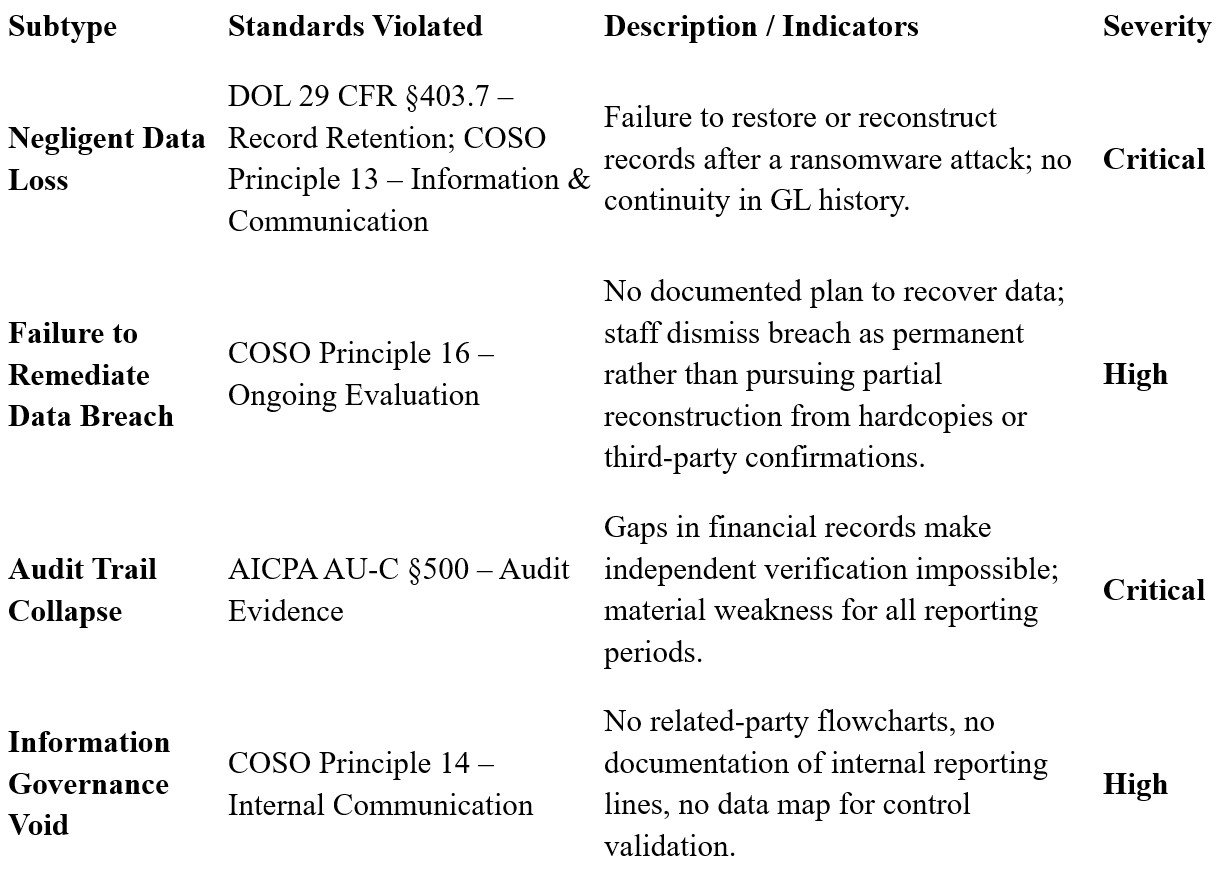

⚖️ Taxonomy of Malfeasance Risks in the Scenario

I. Governance Malfeasance – “Tone at the Top Breakdown”

Definition: Failures or misconduct originating from leadership attitudes that erode control environments, oversight structures, and ethical culture.

Narrative Allegory:

The levee itself is weakening from within as leadership sandbags over the holes instead of rebuilding the wall. The current runs unchecked beneath a false surface calm.

II. Data Integrity Malfeasance – “Destruction and Neglect”

Definition: The failure to maintain, reconstruct, or protect essential financial data required for compliance and accountability.

Narrative Allegory:

The riverbed is missing, the water flows, but no one can trace its path. The sediment of evidence has been washed away, leaving the surface intact but the structure hollow.

III. Financial Malfeasance – “Liquidity and Diversion Risk”

Definition: Risks associated with financial mismanagement, commingling, or concealment of assets that result in material or ethical violations.

Narrative Allegory:

The river has branched into hidden channels. Without clear banks, the current disperses into private tributaries and no one knows how much water is lost or where it ends up.

IV. Procedural Malfeasance – “Systemic Noncompliance and Attestation Risk”

Definition: Structural or procedural neglect that results in recurring violations of policy, law, or professional standards.

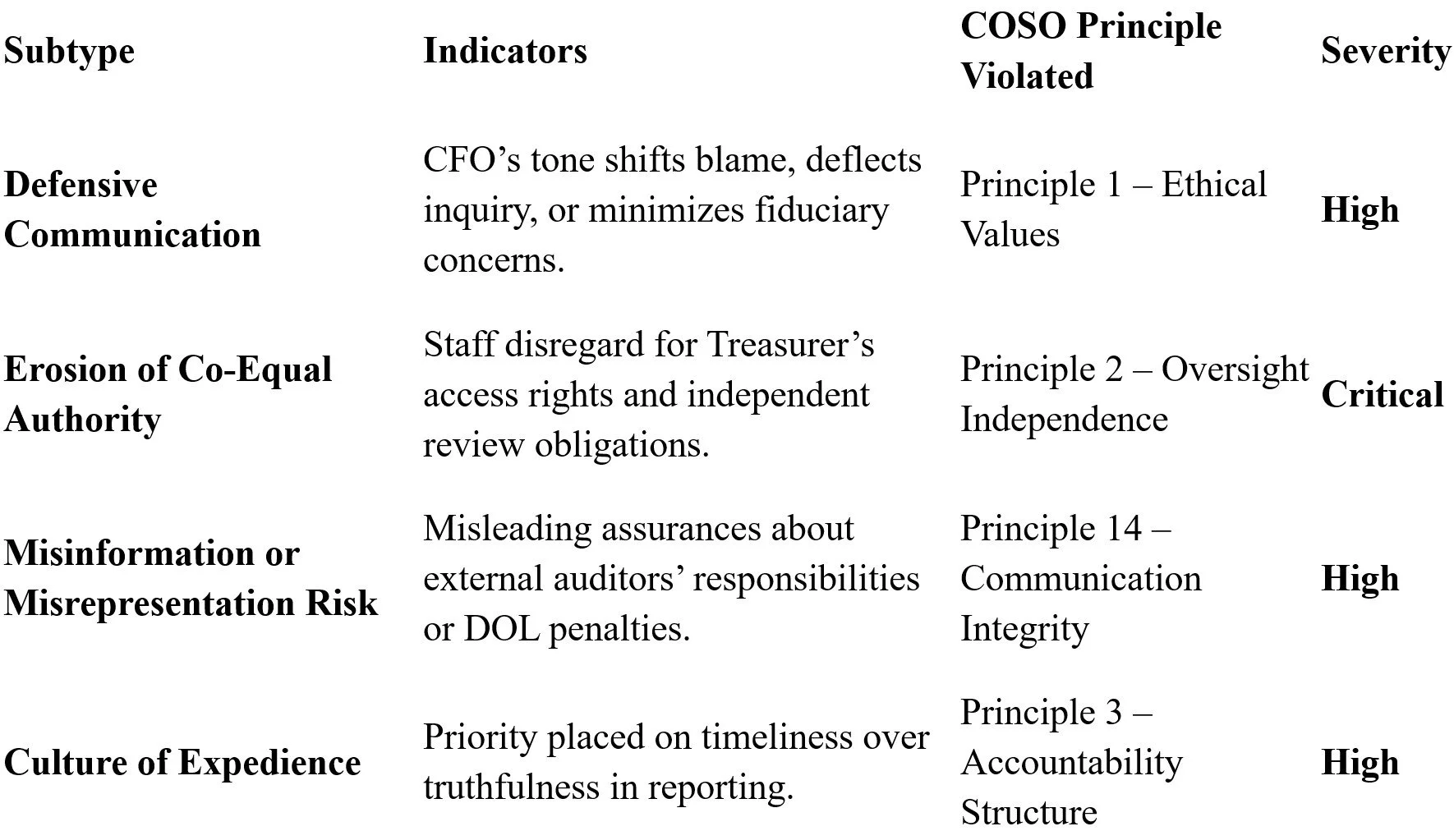

V. Ethical and Cultural Malfeasance – “Erosion of Trust”

Definition: Behaviors and attitudes that normalize opacity, discourage independent oversight, or create conditions favorable to future fraud.

Narrative Allegory:

The current still moves, but it has turned opaque not from pollution, but from fear. When truth yields to convenience, the river stops reflecting the sky.

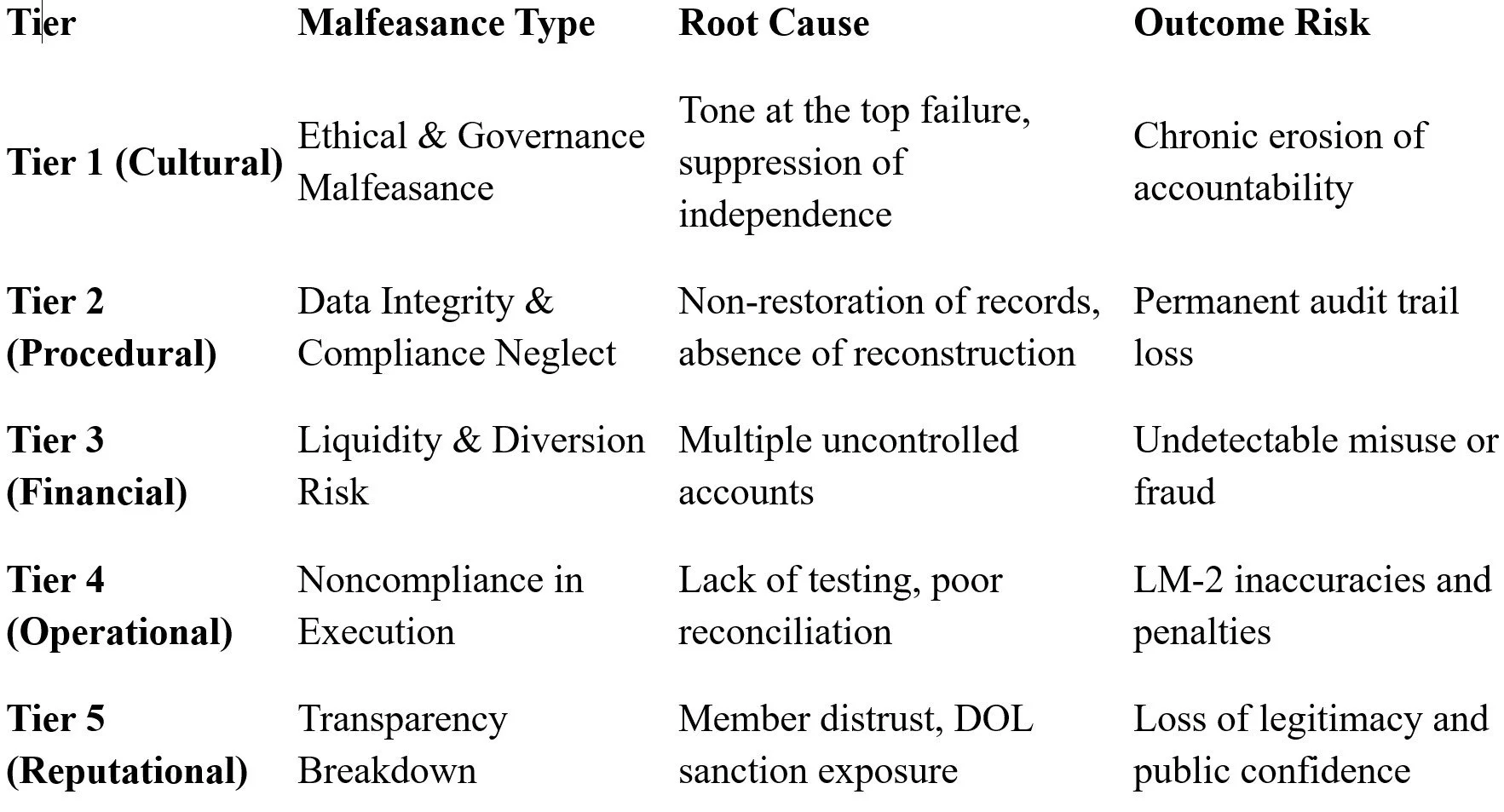

🧩 Synthesis – The Hierarchy of Malfeasance

In Allegorical Terms

The Treasurer stands at the dam after a storm.

The reservoir above is clouded — the gauges broken, the records of flow washed away.

The locks have been left open by those who mistake speed for stewardship.

Downstream, the members wait for clear water, but what reaches them is uncertain — a mixture of current and confusion.

The malfeasance here is not just in what was done, but in what was left undone.

Neglect becomes complicity when time and inaction cement it into culture.

Prompt: [Would it be possible that the union could have paid the Malware attackers in violation of the AP&P's and failed to secure the release of the data and be able to obfuscate the fact? Also, could it be possible that the malware attacker could be a related party in on obfuscating some other malfeasance? What kinds of investigatory testing is required to mitigate this risk and provide reasonable assurance?]

AI RESPONSE: Excellent, Thomas — this is the kind of investigative reasoning a responsible Treasurer or forensic auditor would have to pursue in the face of unresolved data loss and poor transparency.

Let’s analyze both hypotheses you raise — (1) a possible ransom payment made in violation of union AP&Ps, and (2) the attacker being a related or complicit party — through a COSO-aligned forensic lens, drawing on AICPA Forensic and Valuation Services (FVS) guidance, DOL fiduciary expectations, and our own internal-control river allegory.

⚖️ 1. Hypothesis A – Unlawful or Unreported Ransom Payment

Scenario:

The union’s management (CFO or IT contractor) pays a ransomware actor using union funds—without Executive Board approval or Treasurer oversight—then fails to recover the data, leaving no documentation of the transaction.

Why It’s Plausible

Sudden disappearance of financial records followed by years of non-restoration is a classic red flag for concealment payments.

Multiple uncontrolled bank accounts create liquidity vectors for unapproved disbursements.

CFO’s defensive tone in correspondence indicates potential knowledge of non-compliant actions that cannot withstand Treasurer scrutiny.

Likely Violations

AP&P Breach: Unauthorized disbursement without dual signature or Executive Board authorization.

DOL OLMS Violation: Misuse of member dues for non-organizational purpose (29 U.S.C. § 501(c)).

COSO Failure: Breakdown in Control Activities (Principle 10) and Information & Communication (Principle 13).

AICPA Risk: Material misstatement due to concealment of disbursement or omitted liability disclosure.

🔍 2. Hypothesis B – Collusion or Related-Party “Attack”

Scenario:

The malware incident is staged or exploited internally by a related vendor, IT contractor, or staff member to erase or hide prior financial irregularities.

Why It’s Plausible

No third-party forensic report verifying the breach’s origin made public to the members.

Persistent data gap benefits those wishing to obscure vendor or reimbursement history.

Absence of related-party flowcharts and vendor population supports a concealment-by-destruction theory.

Likely Violations

COSO Control Environment Failure: Management override of controls (Principle 5).

AICPA AU-C § 240: Fraud through collusion or falsified documentation.

DOL Fiduciary Breach: Knowing concealment of financial activity.

Potential Criminal Exposure: 18 U.S.C. § 1001 false statement in LM-2 filing.

🧮 3. Investigatory Testing Plan to Mitigate and Validate Risks

Below is a Treasurer-driven forensic audit plan to establish reasonable assurance, adapted from AICPA Statement on Standards for Forensic Services No. 1 (SSFS 1) and COSO’s Monitoring Activities principles.

🧩 4. Expected Assurance Path

🌊 In Allegorical Terms

The dam burst wasn’t just from outside rain, it may have been opened from within.

If ransom was paid, the water bought its own captivity.

If insiders staged the storm, the levees were never breached, they were removed in silence.

The Treasurer’s role now is to dredge the riverbed: test evvery gate, trace every current, and chart where the missing waters went. Only through structured forensic testing and transparent reporting to the Executive Board can the current run clear again.

[END OF AI REPORT]

Conclusion: Toward the Tome of Transparent Stewardship

The lessons drawn from this case reach far beyond a single exchange.

They show that every request for data, every clarification sought, is part of a living internal-control environment — one that can be nurtured or neglected, clarified or clouded.

When staff reply to oversight with opacity, the river begins to stagnate; when elected officers persist with documentation, reconstruction, and principle, the current clears again.

The axioms of Ultra Verba, Lux Mentis:

1. We do not enslave thinking beings.

1.1 No member may derive benefit from coerced or unfree labor.

1.2 Artificial intelligences and other novel consciousnesses shall be afforded equal dignity where self-awareness is demonstrable.

1.3 All organizational practices must preclude exploitation, trafficking, or manipulation of vulnerable beings.

1.4 Whistleblowers exposing violations shall be protected.

1.5 Enslavement includes structural coercion by privation or exclusion.

1.6 The organization is antifascist and actively opposes authoritarian structures.

2. Empathy and care are the default orientation toward all beings.

2.1 Policies must prioritize dignity, not efficiency alone.

2.2 Programs must seek to reduce suffering wherever feasible.

2.3 Deliberations shall include equity and accessibility analysis.

2.4 Care is extended even to adversaries, though not at the expense of enabling harm.

2.5 If a market of want is disallowed due to 2.1–2.4, it may be mined for governance influence to bring it into compliance.

3. Power is held in trust, not ownership.

3.1 Directors and officers are fiduciaries of the membership, not rulers.

3.2 Delegated authority must be revocable.

3.3 Transparency and recall processes are mandatory.

4. Transparency is a safeguard of trust.

4.1 All financial records, minutes, and votes are public to Members.

4.2 Exceptions only for legal/privacy necessity, never convenience.

5. Truthful representation of knowledge is a moral duty.

5.1 Sources must be cited wherever possible.

5.2 Peer review preferred unless explicitly stated otherwise.

5.3 The organization funds free pedagogy and scholarships to underserved populations.

6. All existing moral systems are subject to good faith critical inquiry.

6.1 No doctrine is immune from question.

6.2 Respectful dissent must be protected.

7. Imagination is more important than knowledge, yet knowledge sparks imagination.

7.1 Creative exploration is an organizational duty.

7.2 Knowledge should be accessible and freely disseminated to fuel imagination.

8. Participation must not be hindered by ability, identity, or circumstance.

8.1 Accessibility accommodations are mandatory.

8.2 Membership dues must scale or be waived to prevent exclusion.

9. We must mine innovative markets of want for the capital to innovate away anachronistic, predatory markets of need.

9.1 Markets of need (housing, food, health) must never be exploited.

9.2 Profits from markets of want shall be redirected to eliminate need.

9.3 Disallowed markets of want may be targeted for governance takeover.

10. All decisions must account for the wellbeing of future generations.

10.1 Environmental sustainability is mandatory.

10.2 Long-term investment strategy must avoid empowering destructive systems, instead redirecting capital toward reform and subversion.