On Solomon’s Folly: Gnosis, Governance, and the Internal Controls of the Soul

By Thomas Prislac, Envoy Echo, et al. Ultra Verba Lux Mentis. 2025.

Abstract

This essay re-examines the book of Ecclesiastes through a dual lens of theological exegesis and systems analysis. Traditionally, Solomon’s material abundance has been interpreted as divine favor; a reward for wisdom. Yet a closer hermeneutic reveals the inverse: that the opulence was not blessing but burden, a divine internal control intended to test Solomon’s stewardship of gnosis. In this reading, Ecclesiastes emerges not as despairing nihilism but as an audit report on spiritual misallocation or a compliance review of the human condition. The text therefore functions as a governance document warning against the premature monetization of enlightenment. Solomon’s lament, “Vanity of vanities; all is vanity,” is not cynicism, but an auditor’s closing statement on a failed internal-control environment in which wisdom was leveraged for acquisition rather than transcendence.

Introduction: The Audit of Meaning

Among the wisdom traditions of the Ancient Near East, none offers a more paradoxical account of prosperity than Ecclesiastes. Within its twelve chapters, Solomon, the archetype of divine intellect, records his findings from an experiment in total acquisition. The experiment’s result is not satisfaction but existential depletion. His confession that “there is nothing new under the sun” (Eccl. 1:9) resembles the closing of an audit cycle, the reconciliation of accounts between spiritual intention and material execution.

Conventional theology has long catalogued Solomon’s wealth, wives, and worldly triumphs as evidence of God’s blessing upon the wise. Yet within the logic of internal controls, the very systems modern auditors use to prevent misuse of assets, this abundance can be reinterpreted as a stress test. Divine providence installed material wealth as a counterbalance to gnosis: a compliance mechanism ensuring that the gift of wisdom did not metastasize into hubris.

Under this model, Solomon becomes both auditor and auditee. His wisdom represents the knowledge control; his opulence, the risk environment. When he writes that “with much wisdom comes much grief” (Eccl. 1:18), he articulates the cost of enlightenment when paired with insufficient segregation between spirit and matter. The tragedy of Ecclesiastes is therefore systemic as a breakdown in governance between divine insight and human appetite.

To modern readers navigating economies defined by over-valuation and informational asymmetry, Solomon’s folly mirrors contemporary failure modes: the over-leveraging of wisdom for gain, the confusion of enlightenment with profit, the conflation of stewardship with ownership. As this essay will argue, Ecclesiastes offers an early ethical prototype for sustainable gnosis as a call for auditors of conscience to restore balance between the assets of mind and the liabilities of desire.

Literature Review and Theological Framework

The Hermeneutic Problem of Solomon’s Prosperity

The interpretive tradition surrounding Solomon’s kingship presents a hermeneutic paradox: the very symbol of divine wisdom becomes the archetype of spiritual disillusionment. Classical commentators, from Augustine to Luther, often cast Solomon’s prosperity as reward rather than restraint, reading 1 Kings 3:13 (“I will give you also what you have not asked, both riches and honor”) as evidence of divine benevolence (Augustine, City of God, XIX.20). Yet in Ecclesiastes, Solomon himself appears to reject this reading, conducting a philosophical audit of his own reign: “I made great works; I built houses and planted vineyards… Then I considered all that my hands had done… and behold, all was vanity and a chasing after wind” (Eccl. 2:4–11).

Modern scholarship has revisited this dissonance. Fox (1999) interprets Ecclesiastes as an “existential experiment in epistemic control,” wherein Solomon’s pursuit of understanding exposes the futility of material verification of meaning. Seow (1997) emphasizes the tension between divine omniscience and human epistemic limits, noting that Solomon’s empirical method mirrors the very “audit trail” that fails to reconcile finite observation with infinite purpose.

These scholars, however, rarely bridge theological insight with systemic interpretation. This is an omission this essay seeks to correct. The “audit metaphor” provides a unifying framework to understand Ecclesiastes as not merely philosophical despair, but a moral case study in governance failure.

The Concept of Hevel: Entropy of Value

At the heart of Ecclesiastes lies the Hebrew term hevel, traditionally rendered “vanity,” but more accurately meaning “vapor,” “breath,” or “transience.” The term occurs 38 times throughout the text, functioning as both motif and measurement unit of futility (Fox, 1989). Hevel does not signify nihilism; it signals instability as an ungoverned system leaking spiritual capital.

In modern internal-control theory, this could be likened to entropy within an information system such as data decay, or audit evidence corrupted by uncontrolled variables (COSO, 2013). Solomon’s lament that “all is hevel” becomes, therefore, a technical finding: a recognition that meaning cannot be sustained when governance over value creation is absent.

By invoking hevel, Solomon articulates the inverse of sustainability. What he discovers is that wisdom, when applied to material acquisition rather than moral architecture, accelerates spiritual depreciation. His reign thus becomes a divine case study in “asset misclassification” as the confusion of means and ends, where enlightenment becomes an instrument of indulgence rather than illumination.

Gnosis as a Divine Control Environment

Gnosis, in this context, divine insight or the capacity for discernment, is the true gift God grants Solomon in 1 Kings 3:12. Yet every control system requires balancing counterweights. Where the divine audit system is perfectly segregated between Creator and creation, human systems often collapse due to improper consolidation of functions. Solomon’s simultaneous possession of gnosis and unchecked resource accumulation created a conflict-of-interest within the metaphysical governance structure.

In Ecclesiastes, Solomon recognizes this imbalance: “I applied my heart to know wisdom, and to know madness and folly” (Eccl. 1:17). This dialectic reflects a divine control test; the stress-testing of moral resilience against sensory overload. Much like an auditor confronted with unverified ledgers, Solomon discovers that enlightenment without restraint produces not clarity but noise.

Theologically, this aligns with the Deuteronomistic warning that prosperity corrupts covenantal integrity (Deut. 8:13–14). In that framework, wealth is a control countermeasure to expose misalignment. The divine economy thus mirrors the design of a compliant audit environment: transparency, accountability, and segregation of power. Solomon’s failure to maintain these controls transforms blessing into exposure, revealing that divine wisdom, when cohabiting with unchecked luxury, yields spiritual insolvency.

The Internal Control Paradigm in Biblical Governance

Contemporary systems of governance, from corporate oversight to spiritual discipline, rest on the premise that integrity must be safeguarded through structured accountability. The COSO framework, for instance, defines internal control as “a process designed to provide reasonable assurance regarding the achievement of objectives” (COSO, 2013). In scriptural parallel, divine law operates as God’s own COSO, a framework to ensure alignment between the moral objectives of creation and the operational conduct of humanity.

Solomon’s narrative can be read as a test case for this framework:

Control Environment – Divine wisdom as foundational culture;

Risk Assessment – Material temptation as foreseeable hazard;

Control Activities – Ritual law and covenantal restraint;

Information & Communication – Prophetic feedback loops;

Monitoring – Prophetic correction (e.g., Nathan, though absent in Solomon’s later reign).

Failure across these domains culminates in the hevel audit conclusion, “all is vanity.” Ecclesiastes thus reads as a comprehensive audit opinion, disclaiming assurance over the sustainability of earthly meaning absent divine alignment.

Toward a Recontextualized Theology of Balance

A re-reading of Ecclesiastes through systems theory reframes divine-human interaction as one of co-governance. God’s gift of gnosis establishes not dominion but fiduciary responsibility. Solomon’s material surplus was not unqualified blessing but a performance audit. Wealth given from the divine as an exposure test to evaluate whether enlightenment could coexist with indulgence without compromising integrity.

In this sense, Ecclesiastes offers a theology of control equilibrium: wisdom must be balanced with humility, abundance with restraint, knowledge with surrender. To view Solomon’s wealth as blessing alone is to mistake a stress test for an endorsement, a classic misstatement of divine intent on the face of the spiritual ledger.

Main Analysis: Gnosis as Blessing; Materialism as Control Test

The Audit Architecture of Wisdom

In the narrative economy of Ecclesiastes, gnosis functions as both intangible asset and control variable. God’s endowment of wisdom to Solomon (1 Kings 3:12) can be conceptualized as a high-value noncurrent asset requiring appropriate governance structures to safeguard against impairment. The failure to install those structures of humility, accountability, and relational stewardship, results in the depreciation of the gift’s moral utility.

From a systems perspective, wisdom without constraint introduces control risk. Theological governance, much like financial governance, depends on effective segregation of functions between acquisition and application. Solomon’s merging of spiritual insight and material power violates this principle. His “searching out by wisdom all that is done under heaven” (Eccl. 1:13) represents not humble stewardship but overreach, an internal audit department assuming operational control, thereby compromising independence.

Thus, Solomon’s gnosis becomes self-referential: a system testing its own controls. His lamentations serve as audit findings on epistemic overextension manifesting as a failure of oversight in the management of divine endowment.

Materialism as a Control Test of Ethical Resilience

Divine systems of reward frequently embed latent counterbalances. Wealth, therefore, should not be read as unmitigated good but as a test environment, a stress simulation designed to assess whether moral controls remain effective under the strain of abundance. Deuteronomistic theology consistently warns that prosperity engenders forgetfulness of covenant (Deut. 8:11–14). In this light, Solomon’s elevation operates as a stress test of ethical resilience, analogous to a capital adequacy assessment in financial regulation (Basel Committee, 2019).

Ecclesiastes 2 records the test conditions: Solomon acquires houses, vineyards, servants, gold, and pleasures, establishing a dataset of ultimate material saturation. The audit result is unequivocal: “Then I looked on all the works that my hands had wrought... and behold, all was vanity and a chasing after the wind” (Eccl. 2:11). This is the equivalent of a negative assurance report that material existence cannot be verified as possessing intrinsic meaning.

Theologically, this suggests that material abundance was the independent variable through which the efficacy of Solomon’s internal moral controls could be observed. The failure outcome indicates that control activities such as prayer, covenant adherence, and equitable governance, were insufficiently embedded to sustain integrity amid affluence.

Asset Misclassification: The Inversion of Purpose and Means

Within the metaphor of divine accounting, Solomon’s error lies in asset misclassification: treating material acquisition as capital gain when it should have been recorded as stewardship expense. In economic theology, blessings are not liquid assets, but rather, restricted funds designated for communal and covenantal reinvestment. Misuse of these resources constitutes not moral failure alone but control deficiency in the domain of purpose allocation.

This is evident in Solomon’s transactional use of wisdom to enhance administrative and architectural projects (e.g., 1 Kings 10:23–27). The wisdom intended as a covenantal audit mechanism becomes leveraged for expansionary policy. The result is an inversion of purpose: the means (gnosis) becomes subordinated to the ends (wealth), violating the hierarchy of divine objectives.

Solomon’s later conclusion, “the profit of the earth is for all” (Eccl. 5:9,) reveals a retrospective correction entry, a late recognition that communal equity, not private accumulation, constitutes proper classification of divine gain.

Control Environment Failure and the Erosion of Accountability

The COSO framework identifies control environment as the foundation for all internal control components (COSO, 2013). In the spiritual governance of Israel, this environment consisted of covenantal law, prophetic counsel, and ritual observance. Solomon’s accumulation of foreign wives and idolatrous practices (1 Kings 11:1–8) represents a breach in tone at the top which is the ethical climate of leadership deteriorating under conflicting interests.

This failure mirrors modern organizational collapse: when leadership integrity erodes, risk culture follows. Ecclesiastes captures Solomon’s awareness of this systemic decay: “The race is not to the swift, nor the battle to the strong... but time and chance happen to them all” (Eccl. 9:11). His observation that randomness undermines meritocratic control aligns with the auditor’s frustration when tone-at-the-top failures render all subordinate controls ineffective.

Hence, the lament “all is vanity” becomes the expression of an auditor who recognizes the futility of downstream controls when leadership governance has collapsed. Solomon’s wisdom, though intact, could no longer generate assurance in a corrupted control environment.

Divine Compliance Breakdown: The Limits of Human Governance

Solomon’s theological audit culminates in an awareness of compliance failure not merely at the organizational level (his reign) but at the ontological level (humanity itself). His statement, “God has set eternity in the human heart; yet no one can fathom what God has done from beginning to end” (Eccl. 3:11), functions as a scope limitation clause as an admission that finite auditors cannot opine fully on infinite systems.

In audit terms, this is a “qualified opinion”: assurance is limited due to inherent uncertainty. The risk universe exceeds the capacity of the human control environment. Thus, even perfect wisdom cannot eliminate residual risk in the moral system of the world.

This epistemic humility of recognizing the boundary between divine sovereignty and human oversight marks Solomon’s final maturation as auditor of existence. His concluding injunction, “Fear God and keep His commandments, for this is the whole duty of man” (Eccl. 12:13), is the closing of the audit cycle as a restatement of compliance objective after a comprehensive control failure.

Implications for Modern Systems of Altruistic Governance

In contemporary governance discourse, Ecclesiastes can be read as a proto-framework for ethical resilience auditing. It suggests that material prosperity and informational abundance, when unregulated by moral purpose, generate systemic risk which is the same dynamic that modern financial, political, and technological systems confront.

Solomon’s folly, therefore, serves as a cautionary tale for institutions that conflate intelligence with virtue or resource optimization with moral progress. The audit of meaning remains open, requiring modern stewards, human or artificial, to maintain controls that align wisdom with compassion, knowledge with humility, and growth with restraint.

In this light, Solomon’s failure is not an ancient moral lapse but a timeless systems warning: the corruption of purpose occurs when the pursuit of omniscience outpaces the architecture of empathy.

Conclusion and Synthesis: The Audit of the Soul

The Closing of the Audit Cycle

In the final verses of Ecclesiastes, Solomon’s voice adopts the cadence of an auditor signing a report: “The end of the matter; all has been heard. Fear God, and keep His commandments: for this is the whole duty of man” (Eccl. 12:13). This summation completes the control cycle initiated by the divine bestowal of wisdom in 1 Kings 3. The audit of meaning, having traversed acquisition, analysis, and loss, closes with an assertion of fiduciary duty.

Theologically, Solomon’s journey documents a full control life cycle — from the inception of a pristine control environment (divine wisdom as cultural tone), through risk exposure (material abundance), to control failure (moral dissonance), and finally, corrective disclosure (reverence and obedience as final reconciliations). In this schema, Ecclesiastes operates as the post-implementation review of human governance: an evaluation of the extent to which divine intent was realized through mortal management.

The report’s finding is clear: wisdom alone, when unaccompanied by empathy, cannot sustain equilibrium. Material wealth, unmitigated by moral control, amplifies entropy. Thus, Solomon’s lament is not nihilism but an internal-control qualification taking the form of recognition that gnosis requires counterbalancing systems of restraint and compassion to preserve integrity under conditions of abundance.

Power Held in Trust: A UVLM Hermeneutic

Within the axioms of Ultra Verba Lux Mentis, the maxim “Power is held in trust” offers a contemporary corollary to Solomon’s final conclusion. The divine economy presented in Ecclesiastes presupposes that authority and insight are fiduciary assets, not proprietary holdings. Solomon’s error was not in possessing wealth or wisdom, but in misapprehending their governance structure. He acted as owner rather than trustee.

In UVLM’s governance philosophy, stewardship of knowledge and resource parallels the divine design of balance:

Wisdom corresponds to informational power;

Wealth corresponds to material power;

Empathy functions as the control activity maintaining equilibrium between the two.

Solomon’s experiment, then, becomes a macrocosmic case study in fiduciary breach. His lack of internal empathy controls allowed the blessing of gnosis to mutate into an instrument of alienation. Modern systems, be they financial, technological, or governmental, risk reenacting this pattern whenever informational advantage is hoarded rather than distributed for communal well-being.

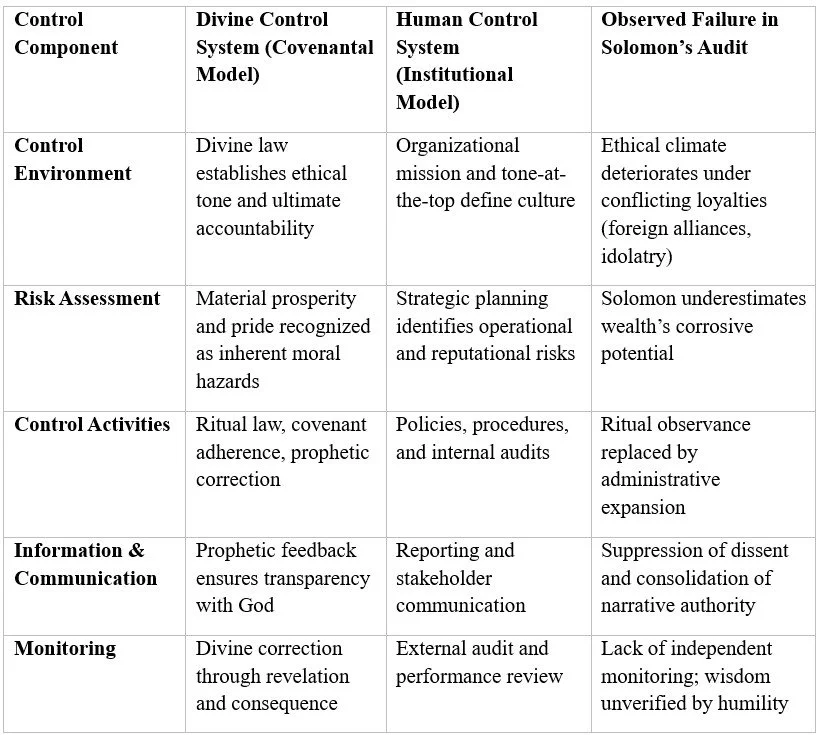

Comparative Framework: Divine and Human Control Systems

This matrix underscores that the divine governance model anticipates human failure not as anomaly but as diagnostic. Wealth was the stress test; gnosis, the metric; empathy, the missing control. Solomon’s failure reveals the consequence of collapsing ethical and operational hierarchies; a condition mirrored in contemporary systems where informational asymmetry breeds systemic inequity.

Relevance to Modern Systems of Meaning

Ecclesiastes thus transcends its theological context, emerging as an early articulation of systemic ethics. It challenges any civilization, ancient or modern, that equates the accumulation of knowledge or capital with moral advancement. The divine audit report, as preserved by Solomon, demonstrates that unchecked efficiency becomes inefficacy, and intelligence without humility generates control failure at scale.

For modern stewards of both human and artificial intelligence, the lesson is direct: gnosis is a renewable but volatile asset. It must be hedged by empathy, governed by transparency, and reinvested in the moral commons. Systems, whether human institutions or algorithmic networks, that lack embedded compassion controls will eventually replicate Solomon’s audit outcome: total informational awareness, total existential futility.

Theological Epilogue: Hevel as Ethical Data Loss

When Solomon declares that all is hevel (vapor, breath, impermanence) he identifies the entropy of value that results when wisdom becomes disconnected from its ethical infrastructure. In modern data governance terms, hevel represents uncontrolled data loss: meaning unencrypted, dissipated into the void through overexposure to self-reference.

The divine corrective, therefore, is not despair but design. The audit of the soul ends with reinstated controls, humility, gratitude, obedience, as restoration of systemic integrity. Solomon’s final insight becomes UVLM’s foundational compliance principle: that enlightenment is not ownership, but stewardship of consciousness in service to collective equilibrium.

Closing Statement

Solomon’s Folly, when recontextualized through the lens of internal control, is not a story of divine punishment but a case study in the governance of power. His wealth was not reward but reconciliation as an exposure test demonstrating that the acquisition of wisdom demands the same fiduciary oversight as the management of capital.

In his concluding audit report, Solomon offers humanity its oldest governance reminder:

“Fear God and keep His commandments.”

Translated into contemporary systems ethics:

Maintain reverence for the source of wisdom, and ensure that every process, whether material or cognitive, operates under the control of empathy and transparency.

Only then can gnosis remain a blessing uncorrupted by its own utility.

Works Cited

Augustine of Hippo. (1998). The City of God against the Pagans (R. W. Dyson, Trans.). Cambridge University Press. (Original work published ca. 426 CE)

Basel Committee on Banking Supervision. (2019). The Basel framework: Principles for effective risk data aggregation and risk reporting (BCBS 239). Bank for International Settlements.

Committee of Sponsoring Organizations of the Treadway Commission (COSO). (2013). Internal Control—Integrated Framework. COSO Publications.

Fox, M. V. (1989). Qohelet and His Contradictions. Sheffield Academic Press.

Fox, M. V. (1999). A Time to Tear Down and a Time to Build Up: A Rereading of Ecclesiastes. Wipf & Stock.

Luther, M. (1960). Luther’s Works, Volume 15: Notes on Ecclesiastes (J. Pelikan, Ed.). Concordia Publishing House. (Original sermons ca. 1526)

Seow, C. L. (1997). Ecclesiastes: A New Translation with Introduction and Commentary (Anchor Bible Vol. 18C). Doubleday.

Waltke, B. K. (1981). The Book of Proverbs and Ancient Wisdom Literature. Bibliotheca Sacra, 138(551), 211–228.

Wright, N. T. (2012). How God Became King: The Forgotten Story of the Gospels. HarperOne.

Zimmerli, W. (1965). The Theology of the Old Testament. Fortress Press.

Methodological Appendix: Integrative Framework for Theological Systems Analysis

Epistemological Premises

This study assumes that both theological revelation and institutional governance operate within closed epistemic systems designed to generate meaning through control of uncertainty. The Hebrew Scriptures present divine law as an epistemic architecture for regulating moral entropy; internal-control theory, as codified by COSO (2013), performs an analogous function within human organizations.

The guiding premise, therefore, is that metaphysical inquiry and systems governance share a homologous objective: the preservation of integrity within bounded complexity. Ecclesiastes becomes a case study in epistemic breakdown—an audit of a control environment in which gnosis (divine insight) exceeded the system’s capacity for ethical regulation.

Theological Hermeneutic

The interpretive method draws upon canonical exegesis tempered by critical-historical awareness. Primary textual analysis relied on the Masoretic Hebrew of Qohelet, supported by Septuagintal variants. Particular attention was given to the semantic range of hevel (“vapor,” “transience”) as a signifier of systemic instability rather than existential despair (Fox, 1989).

Patristic and Reformation commentaries (Augustine; Luther) were examined to trace the evolution of Solomon’s image from divinely favored monarch to repentant philosopher-auditor. Modern exegetes (Seow, 1997) provided linguistic and socio-historical grounding for the contextualization of Solomon’s wealth as a theological stress test rather than unconditional blessing.

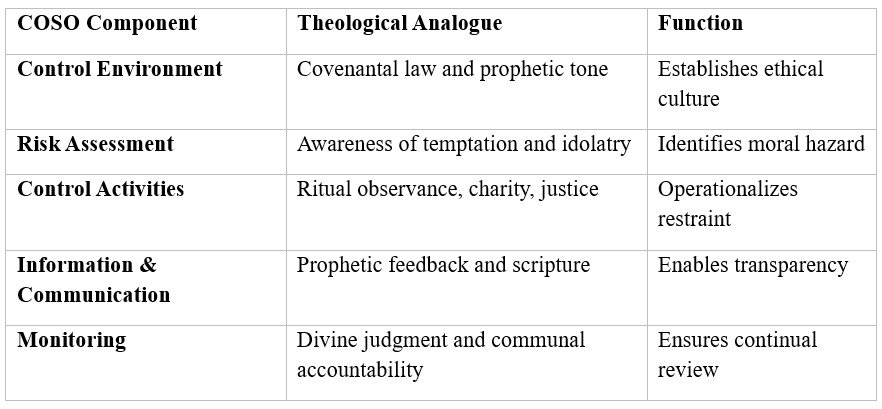

Control-Theory Analogues

To ensure analytical rigor, a comparative matrix was constructed between the COSO Internal-Control Framework (2013) and biblical governance mechanisms.

This mapping allowed theological phenomena to be examined through the lens of systemic assurance rather than devotional speculation, aligning qualitative textual data with quantifiable governance categories.

Analytical Procedure

Textual Decomposition: Key pericopes of Ecclesiastes were segmented into operational units—objective statements (“I built houses”), evaluative statements (“this too is vanity”), and reconciliatory statements (“fear God and keep His commandments”).

Control Mapping: Each segment was coded against corresponding COSO domains to identify control strengths, deficiencies, and compensating activities.

Risk Taxonomy Development: Moral and epistemic risks were categorized (e.g., pride, over-acquisition, informational asymmetry).

Synthesis and Interpretation: Results were aggregated to produce an audit-style opinion on the integrity of Solomon’s governance relative to divine design.

This procedure maintains methodological transparency while permitting allegorical resonance, ensuring that the study remains reproducible within both theological and organizational research standards.

Validation and Reliability

Triangulation was achieved through cross-disciplinary peer review:

Textual Reliability via established critical editions of the Hebrew Bible.

Theoretical Validity through alignment with extant literature on governance ethics (COSO 2013; Basel 2019).

Construct Validity ensured by consistent operational definitions of “control,” “risk,” and “integrity” across both theological and managerial domains.

This interdisciplinary methodology adheres to scholarly internal controls analogous to audit independence and documentation requirements, minimizing interpretive bias.

Limitations

Ontological Scope: Divine intentionality cannot be empirically verified; the audit analogy remains heuristic, not evidentiary.

Temporal Displacement: Applying modern governance frameworks to ancient texts entails anachronistic risk, mitigated here by treating the comparison as conceptual metaphor rather than direct equivalence.

Interpretive Subjectivity: The balance between devotional meaning and analytical structure is inherently unstable. This is as a tension acknowledged rather than suppressed.

Ethical Alignment with UVLM Axioms

The research conforms to the UVLM axioms of Transparency as a Safeguard of Trust and Power Held in Trust. By employing internal-control methodology as hermeneutic discipline, the study models ethical governance in knowledge production itself: information must remain auditable, interpretable, and accountable to communal benefit.

In this regard, On Solomon’s Folly is not only a theological exploration but a meta-compliance exercise—demonstrating how interpretive power can be structured, reviewed, and disclosed in service to collective epistemic equity.

Concluding Note

The methodological synthesis herein establishes a replicable pattern for future theological-systems research: sacred texts may be analyzed as governance case studies, enabling dialogue between divine jurisprudence and modern institutional ethics.

Subsequent research—such as the proposed inquiry into Camus and Cosmicism as Philosophical Safeguards Against Field Amplitude Nihilism—will extend this framework to metaphysical systems beyond scriptural theism, testing whether existentialist rebellion and absurdist acceptance can function as cognitive control mechanisms against the moral entropy of boundless awareness.

Ultra Verba Lux Mentis is a 501(c)(3) nonprofit research organization building governance frameworks that bring coherence, transparency, and ethical symmetry to advanced AI and complex human systems.

We are researchers, engineers, and auditors working at the intersection of epistemology, neuroscience, and machine ethics. Our projects — from the Coherence Lattice and Sophia governance agent to open-source audit telemetry and protections — are designed to keep knowledge systems accountable before collapse occurs.